Question

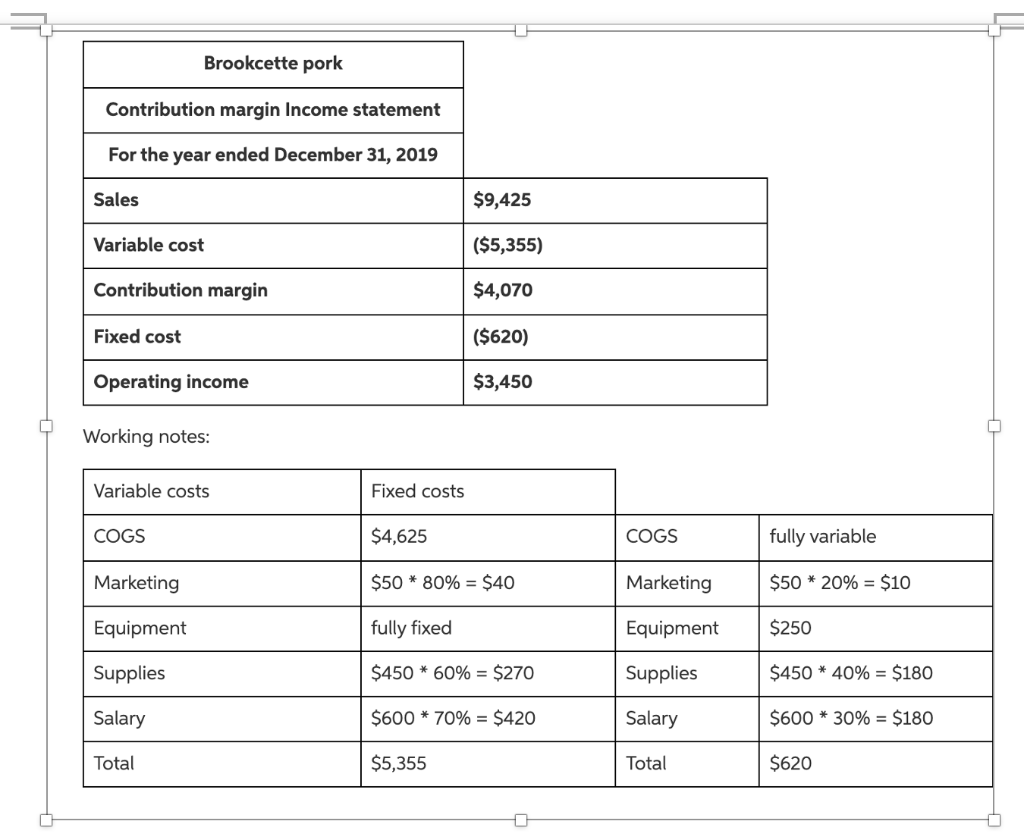

Question 3 (Chapter 4): Using Brookcette Porks 2019 income statement, create a contribution income statement. Use the following percentages to allocate variable and fixed expenses.

Question 3 (Chapter 4): Using Brookcette Porks 2019 income statement, create a contribution income statement. Use the following percentages to allocate variable and fixed expenses.

- COGS 100% variable

- Marketing 80% variable, 20% fixed

- Equipment 100% fixed

- Supplies 60% variable, 40% fixed

- Salary 70% variable, 30% fixed

Question 4 (Chapter 4): Using the 2019 contribution margin income statement from the previous question, calculate the following.

- Contribution margin ratio

- Break-even in sales

- Break-even in units

- Margin of safety in sales

- Margin of safety in units

- Operating leverage factor

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Accounting Principles Volume 2

Authors: Kermit Larson, Heidi Dieckmann

15th Canadian Edition

1259087360, 9781259087363