Question

Question 3 In this question you will argue that the set of competitive equilibrium prices of a com- petitive economy has essentially no structure other

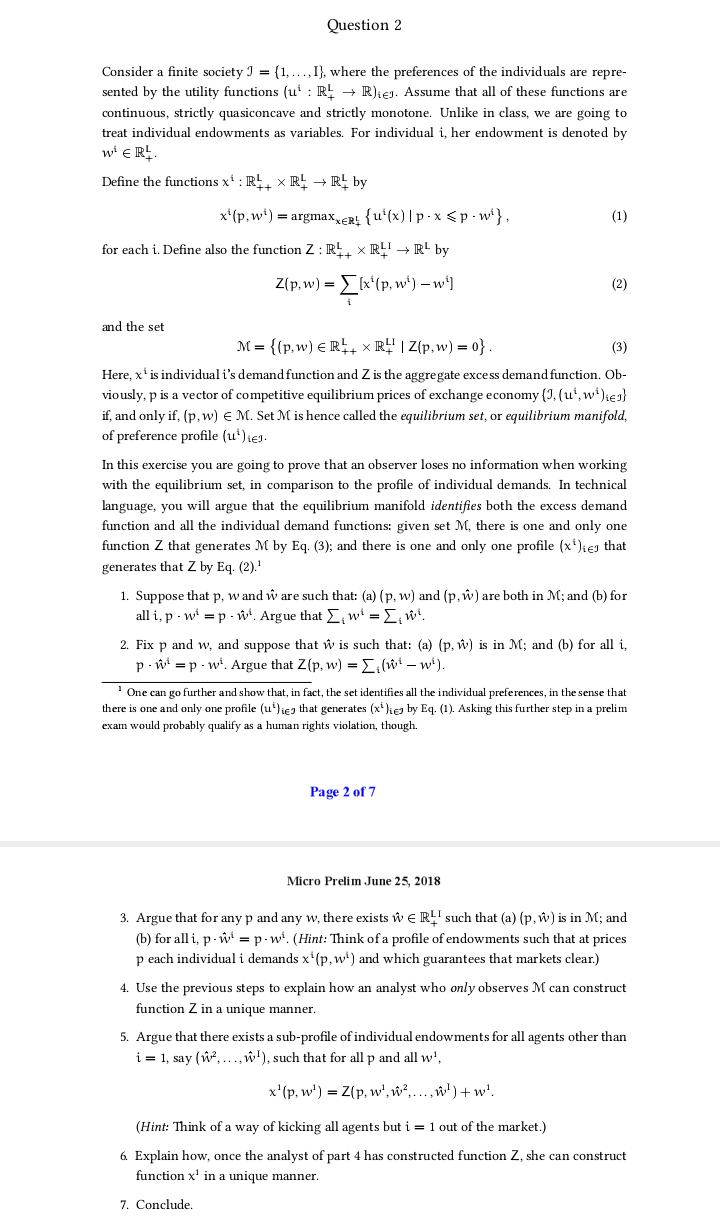

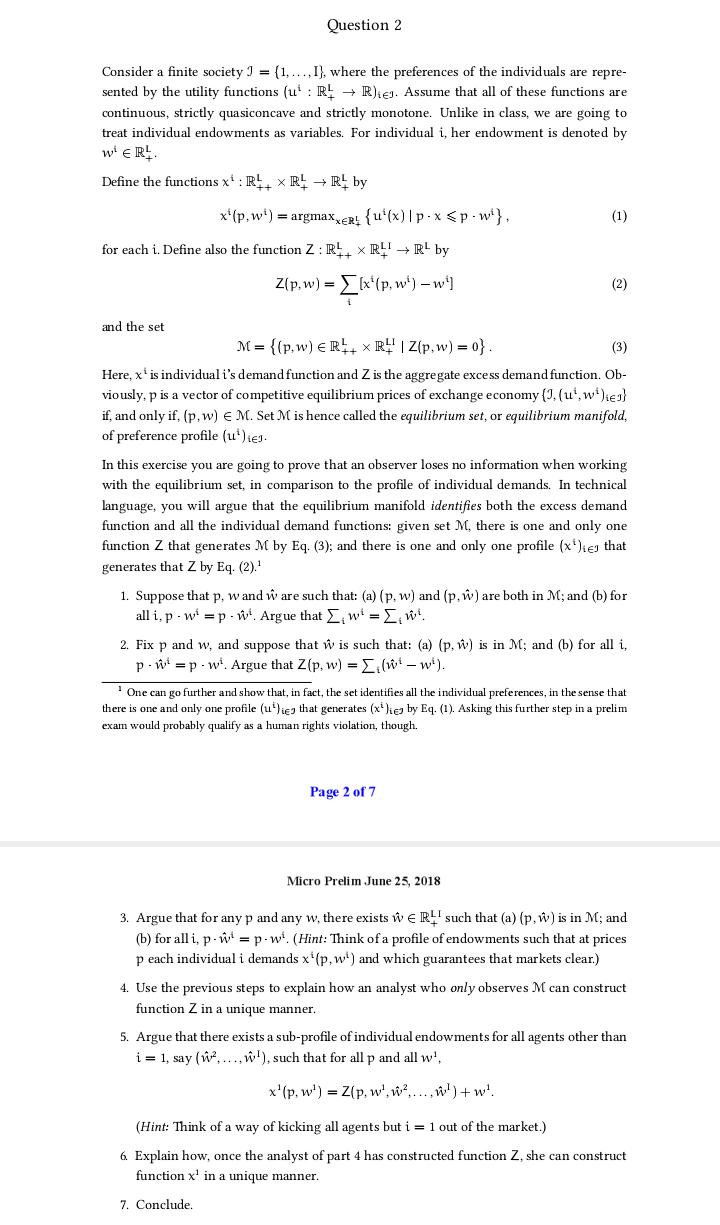

2 0, a solution to the UMAX[p, w] problem exists and is unique. Without attempting at this point to explicitly solve the UMAX[p, w], show that for w above a certain level, that you should made explicit, demand is insensitive to increases in wealth, whereas for values of w below this level Walrasian demand is affine in wealth. (Hint: For the second part, use the Implicit Function Theorem.) 1.7. We now consider a society with / consumers, each endowed with the preference relation represented by u in (1.1). We denote by P= R#'the domain of prices and individual wealth vectors (p:w'....w). Is there a subset of P for which a positive representative consumer exists? Explain. 1.8. We return to the one-consumer case. Solve the UMAX[p, w] problem for good I in the case where I - 2, a, =a, =a and B= b * , for c>0. Can one of the goods be inferior at a point of the domain of the Walrasian demand function? (Hint. Consider the wealth expansion paths in (x1, *2) space.) 1.9. We now consider a consumer who faces uncertainty. Her ex ante preference relation satisfies the expected utility hypothesis with von Neumann-Morgenstern-Bernoulli utility function ":[0.a/b]- R. where a and b are positive parameters, and with coefficient of absolute risk aversion equal to- a - bx -. She is facing the contingent-consumption optimization problem of maximizing her expected utility subject to a budget constraint. Let there be two states of the world, s, and $2, with probabilities a and 1- n, respectively 1.9.1. Comment on her ex ante preferences. 1.9.2. To what extent is her problem formally a special case of the UMAX problem of 1.6 above? Explain. 1.9.3. Draw a plausible wealth expansion path in contingent commodity space. As her wealth increases, does the consumer bear absolutely more or less risk? Relatively more or less risk?Question 2 Consider a finite society ] = (1, ..., I), where the preferences of the individuals are repre- sented by the utility functions (ul : R4 - Rhey. Assume that all of these functions are continuous, strictly quasiconcave and strictly monotone. Unlike in class, we are going to treat individual endowments as variables. For individual i, her endowment is denoted by WERE Define the functions x' : R x R! - R! by x'(p. wi ) = argmaxxent {u'(x) |p - x

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations of Macroeconomics

Authors: Robin Bade, Michael Parkin

8th edition

134492005, 978-0134492001