Answered step by step

Verified Expert Solution

Question

1 Approved Answer

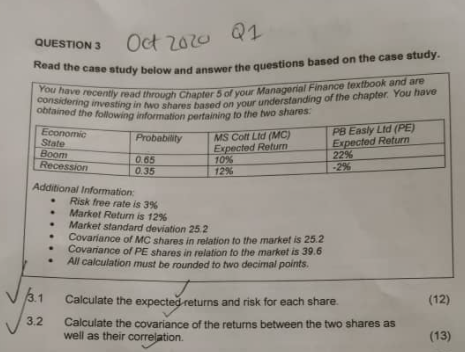

QUESTION 3 Oct 2020 Q1 Read the case study below and answer the questions based on the case study. You have recently read through Chapter

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sound Investing Uncover Fraud And Protect Your Portfolio

Authors: Kate Mooney

1st Edition

0071481826, 9780071481823