Answered step by step

Verified Expert Solution

Question

1 Approved Answer

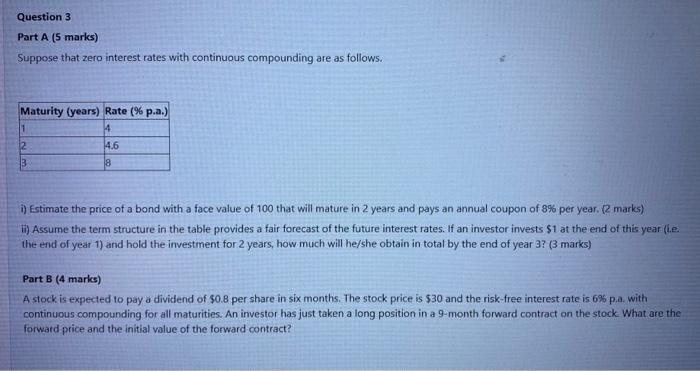

Question 3 Part A (5 marks) Suppose that zero interest rates with continuous compounding are as follows. Maturity (years) Rate (% p.a.) 1 2

Question 3 Part A (5 marks) Suppose that zero interest rates with continuous compounding are as follows. Maturity (years) Rate (% p.a.) 1 2 3 4 4.6 8 i) Estimate the price of a bond with a face value of 100 that will mature in 2 years and pays an annual coupon of 8% per year. (2 marks) ii) Assume the term structure in the table provides a fair forecast of the future interest rates. If an investor invests $1 at the end of this year (i.e. the end of year 1) and hold the investment for 2 years, how much will he/she obtain in total by the end of year 3? (3 marks) Part B (4 marks) A stock is expected to pay a dividend of $0.8 per share in six months. The stock price is $30 and the risk-free interest rate is 6% p.a. with continuous compounding for all maturities. An investor has just taken a long position in a 9-month forward contract on the stock. What are the forward price and the initial value of the forward contract?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Theory and Analysis Text and Cases

Authors: Richard G. Schroeder, Myrtle W. Clark, Jack Cathey

11th edition

9781118806500, 1118582799, 1118806506, 978-1118582794