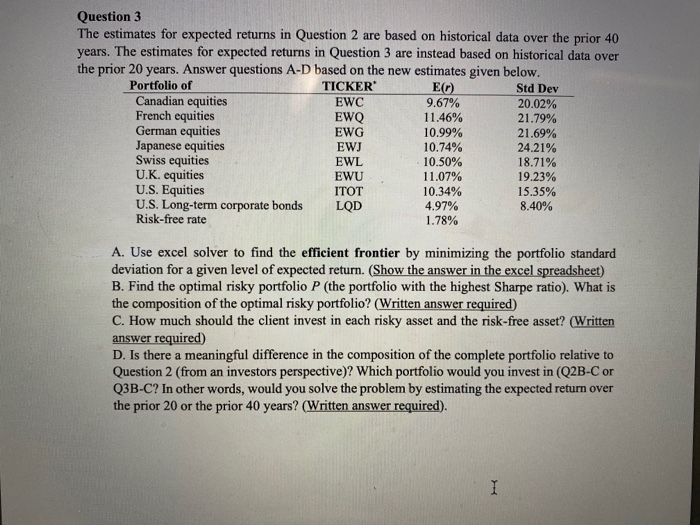

Question 3 The estimates for expected returns in Question 2 are based on historical data over the prior 40 years. The estimates for expected returns in Question 3 are instead based on historical data over the prior 20 years. Answer questions A-D based on the new estimates given below. Portfolio of TICKER Er) Std Dev Canadian equities EWC 9.67% 20.02% French equities EWQ 11.46% 21.79% German equities EWG 10.99% 21.69% Japanese equities EWJ 10.74% 24.21% Swiss equities EWL 10.50% 18.71% U.K. equities EWU 11.07% 19.23% U.S. Equities ITOT 10.34% 15.35% U.S. Long-term corporate bonds 4.97% 8.40% Risk-free rate 1.78% LOD A. Use excel solver to find the efficient frontier by minimizing the portfolio standard deviation for a given level of expected return. (Show the answer in the excel spreadsheet) B. Find the optimal risky portfolio P (the portfolio with the highest Sharpe ratio). What is the composition of the optimal risky portfolio? (Written answer required) C. How much should the client invest in each risky asset and the risk-free asset? (Written answer required) D. Is there a meaningful difference in the composition of the complete portfolio relative to Question 2 (from an investors perspective)? Which portfolio would you invest in (Q2B-C or Q3B-C? In other words, would you solve the problem by estimating the expected return over the prior 20 or the prior 40 years? (Written answer required). Question 3 The estimates for expected returns in Question 2 are based on historical data over the prior 40 years. The estimates for expected returns in Question 3 are instead based on historical data over the prior 20 years. Answer questions A-D based on the new estimates given below. Portfolio of TICKER Er) Std Dev Canadian equities EWC 9.67% 20.02% French equities EWQ 11.46% 21.79% German equities EWG 10.99% 21.69% Japanese equities EWJ 10.74% 24.21% Swiss equities EWL 10.50% 18.71% U.K. equities EWU 11.07% 19.23% U.S. Equities ITOT 10.34% 15.35% U.S. Long-term corporate bonds 4.97% 8.40% Risk-free rate 1.78% LOD A. Use excel solver to find the efficient frontier by minimizing the portfolio standard deviation for a given level of expected return. (Show the answer in the excel spreadsheet) B. Find the optimal risky portfolio P (the portfolio with the highest Sharpe ratio). What is the composition of the optimal risky portfolio? (Written answer required) C. How much should the client invest in each risky asset and the risk-free asset? (Written answer required) D. Is there a meaningful difference in the composition of the complete portfolio relative to Question 2 (from an investors perspective)? Which portfolio would you invest in (Q2B-C or Q3B-C? In other words, would you solve the problem by estimating the expected return over the prior 20 or the prior 40 years? (Written answer required)