Answered step by step

Verified Expert Solution

Question

1 Approved Answer

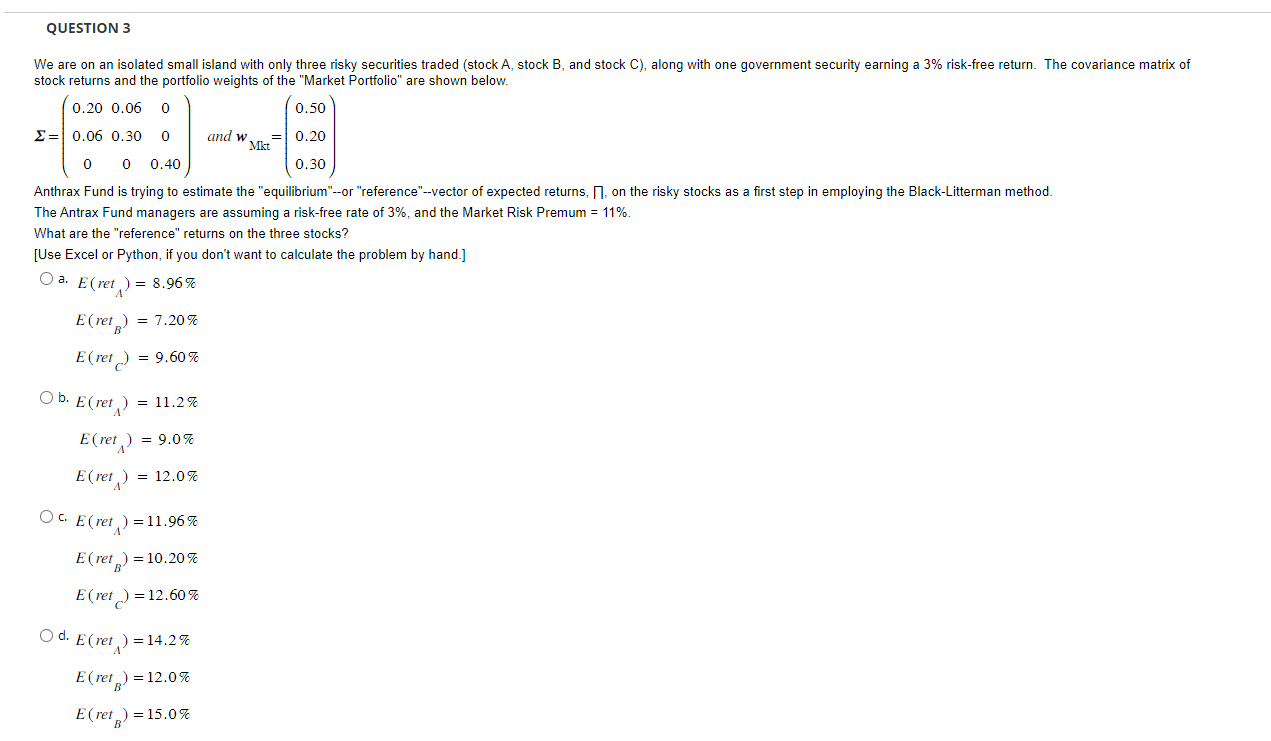

QUESTION 3 We are on an isolated small island with only three risky securities traded (stock A, stock B, and stock C), along with one

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Research On Behavioral Finance And Investment Strategies Decision Making In The Financial Industry

Authors: Zeynep Copur

1st Edition

1466674849,1466674857