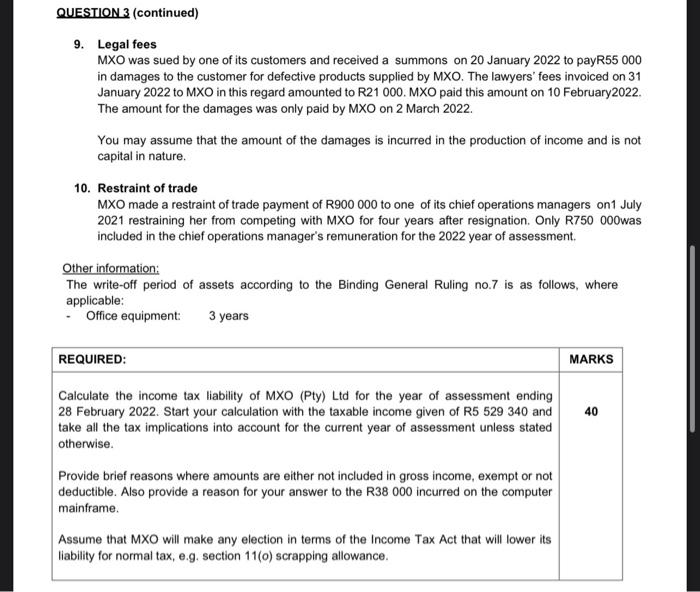

QUESTION 3b (40 marks) MXO (Pty) Ltd (MXO) is a manufacturing company that manufactures biodegradable products, such as cups, plates, cutlery, storage containers and straws. The current year of assessment ends on 28 February 2022. MXO is a small business corporation as defined in the Income Tax Act. You are the junior tax accountant at MXO and must finalise the tax calculation before the auditors arrive for the 28 February 2022 audit. Currently you have calculated a taxable income figure of R5 529340 before taking into account all the current year tax implications of the items below: 1. Fixed assets Purchased andexisting MXO have the following assets at the end of the 2022 year of assessment: - New manufacturing asset N8 purchased for R1 000000 and brought into use on 1 June 2021; - New non-manufacturing asset N9 purchased for R750 000 and brought into use on 1 December 2021; - Second-hand manufacturing asset N10 purchased for R400000 and brought into use on 1 February 2022. Moving and installation costs of R21 000 were incurred by MXO on27 January 2022 to move the machinery from the seller's premises. - Second-hand non-manufacturing asset E1 for R300 000, brought into use on 2 January 2020; Sold/Scrapped - New manufacturing asset E2 purchased for R120 000 and brought into use on 1 June 2020, was sold for R70 000 at an auction on 21 January 2022. Asset E2 had a tax value of Rnil on 1 March 2021. - A delivery vehicle was scrapped on 12 February 2022 after it was involved in an accident. MXO was not indemnified by its insurer for this loss. The vehicle was purchased and brought into use by MXO on 3 April 2020 for R480 000. On 20 February 2022 MXO accepted an offer from a scrap dealer for the scrapped delivery vehicle and received R5 000 on the same day. 2. Office space - On 1 March 2021 MXO purchased newly developed office space for all the administrative staff to operate from. MXO purchased the asset from a developer for R500 000 and brought it into use on 1 April 2021 - Office equipment (purchased and brought into use on 31 August 2020 for R85 000) was moved from a factory building to this new office on 2 March 2021. The moving costs of R11 000 were incurred. (Only account for the moving costs.) - On 30 November 2021, a fire started in the kitchenette which set off the fire alarm and triggered the sprinkler system. Unfortunately, there was water damage to a component of the computer mainframe. A replacement for the defective component was purchased for R38 000 on 3 December 2021 and installed to replace the damaged one. QUESTION 3 (continued) 3. Patents and trademarks - MXO purchased and brought into use a patent on 1 March 2018 for R250 000 for a three-year term. The patent term was extended for another three years from 1 March 2021 for R10 000. (Account for both transactions.) - A trademark was purchased and brought into use for R95 000 on 2 May 2021. 4. Research and development During the 2022 year of assessment, MXO started developing an invention: a biodegradable edible drinking cup. Approval by the Minister of Science and Technology was received on 1 April 2021 as well as a grant of R450 000 . The following costs were incurred for the research project during the 2022 year of assessment: - Salaries of R2 000000 were paid to staff involved exclusively in the research of the product from 1 April 2021. The grant was used to cover a portion of this salary expense. - A new machine costing R1 000000 was purchased and brought into use on 8 June 2021 for the purposes of the research. - Marketing costs of R56 000 in respect of the invention was paid on 15 March 2021. 5. Insurance contract An insurance contract was entered into with a new insurance company on 1 February 2022. The insurance premiums were payable in advance from the inception of the contract. MXO made a payment of R286 000 for the period 1 February 2022 to 31 January 2023. The insurance contract covers MXO for loss of fire and theft of its assets. 6. Donation MXO donated R25 000 cash on 31 August 2021 to a registered public benefit organisation. A valid section 18A receipt was received on the same date. 7. Bad debts Due to the Covid19 pandemic, MXO's customers had trouble paying their accounts. As a result, MXO wrote off R50 000 as irrecoverable during the 2022 year of assessment. A further amount of R9 300 was also written off in respect of staff loans. 8. Doubtful debtors The debtors clerk presents you with an extract from the debtors age analysis: Note: Assume that IFRS 9 is not applicable. MXO claimed a doubtful debts allowance of R29 640 in the 2021 year of assessment. QUESTION 3 (continued) 9. Legal fees MXO was sued by one of its customers and received a summons on 20 January 2022 to payR55 000 in damages to the customer for defective products supplied by MXO. The lawyers' fees invoiced on 31 January 2022 to MXO in this regard amounted to R21 000. MXO paid this amount on 10 February2022. The amount for the damages was only paid by MXO on 2 March 2022. You may assume that the amount of the damages is incurred in the production of income and is not capital in nature. 10. Restraint of trade MXO made a restraint of trade payment of R900 000 to one of its chief operations managers on1 July 2021 restraining her from competing with MXO for four years after resignation. Only R750 000was included in the chief operations manager's remuneration for the 2022 year of assessment. Other information: The write-off period of assets according to the Binding General Ruling no.7 is as follows, where applicable: - Office equipment: 3 years QUESTION 3b (40 marks) MXO (Pty) Ltd (MXO) is a manufacturing company that manufactures biodegradable products, such as cups, plates, cutlery, storage containers and straws. The current year of assessment ends on 28 February 2022. MXO is a small business corporation as defined in the Income Tax Act. You are the junior tax accountant at MXO and must finalise the tax calculation before the auditors arrive for the 28 February 2022 audit. Currently you have calculated a taxable income figure of R5 529340 before taking into account all the current year tax implications of the items below: 1. Fixed assets Purchased andexisting MXO have the following assets at the end of the 2022 year of assessment: - New manufacturing asset N8 purchased for R1 000000 and brought into use on 1 June 2021; - New non-manufacturing asset N9 purchased for R750 000 and brought into use on 1 December 2021; - Second-hand manufacturing asset N10 purchased for R400000 and brought into use on 1 February 2022. Moving and installation costs of R21 000 were incurred by MXO on27 January 2022 to move the machinery from the seller's premises. - Second-hand non-manufacturing asset E1 for R300 000, brought into use on 2 January 2020; Sold/Scrapped - New manufacturing asset E2 purchased for R120 000 and brought into use on 1 June 2020, was sold for R70 000 at an auction on 21 January 2022. Asset E2 had a tax value of Rnil on 1 March 2021. - A delivery vehicle was scrapped on 12 February 2022 after it was involved in an accident. MXO was not indemnified by its insurer for this loss. The vehicle was purchased and brought into use by MXO on 3 April 2020 for R480 000. On 20 February 2022 MXO accepted an offer from a scrap dealer for the scrapped delivery vehicle and received R5 000 on the same day. 2. Office space - On 1 March 2021 MXO purchased newly developed office space for all the administrative staff to operate from. MXO purchased the asset from a developer for R500 000 and brought it into use on 1 April 2021 - Office equipment (purchased and brought into use on 31 August 2020 for R85 000) was moved from a factory building to this new office on 2 March 2021. The moving costs of R11 000 were incurred. (Only account for the moving costs.) - On 30 November 2021, a fire started in the kitchenette which set off the fire alarm and triggered the sprinkler system. Unfortunately, there was water damage to a component of the computer mainframe. A replacement for the defective component was purchased for R38 000 on 3 December 2021 and installed to replace the damaged one. QUESTION 3 (continued) 3. Patents and trademarks - MXO purchased and brought into use a patent on 1 March 2018 for R250 000 for a three-year term. The patent term was extended for another three years from 1 March 2021 for R10 000. (Account for both transactions.) - A trademark was purchased and brought into use for R95 000 on 2 May 2021. 4. Research and development During the 2022 year of assessment, MXO started developing an invention: a biodegradable edible drinking cup. Approval by the Minister of Science and Technology was received on 1 April 2021 as well as a grant of R450 000 . The following costs were incurred for the research project during the 2022 year of assessment: - Salaries of R2 000000 were paid to staff involved exclusively in the research of the product from 1 April 2021. The grant was used to cover a portion of this salary expense. - A new machine costing R1 000000 was purchased and brought into use on 8 June 2021 for the purposes of the research. - Marketing costs of R56 000 in respect of the invention was paid on 15 March 2021. 5. Insurance contract An insurance contract was entered into with a new insurance company on 1 February 2022. The insurance premiums were payable in advance from the inception of the contract. MXO made a payment of R286 000 for the period 1 February 2022 to 31 January 2023. The insurance contract covers MXO for loss of fire and theft of its assets. 6. Donation MXO donated R25 000 cash on 31 August 2021 to a registered public benefit organisation. A valid section 18A receipt was received on the same date. 7. Bad debts Due to the Covid19 pandemic, MXO's customers had trouble paying their accounts. As a result, MXO wrote off R50 000 as irrecoverable during the 2022 year of assessment. A further amount of R9 300 was also written off in respect of staff loans. 8. Doubtful debtors The debtors clerk presents you with an extract from the debtors age analysis: Note: Assume that IFRS 9 is not applicable. MXO claimed a doubtful debts allowance of R29 640 in the 2021 year of assessment. QUESTION 3 (continued) 9. Legal fees MXO was sued by one of its customers and received a summons on 20 January 2022 to payR55 000 in damages to the customer for defective products supplied by MXO. The lawyers' fees invoiced on 31 January 2022 to MXO in this regard amounted to R21 000. MXO paid this amount on 10 February2022. The amount for the damages was only paid by MXO on 2 March 2022. You may assume that the amount of the damages is incurred in the production of income and is not capital in nature. 10. Restraint of trade MXO made a restraint of trade payment of R900 000 to one of its chief operations managers on1 July 2021 restraining her from competing with MXO for four years after resignation. Only R750 000was included in the chief operations manager's remuneration for the 2022 year of assessment. Other information: The write-off period of assets according to the Binding General Ruling no.7 is as follows, where applicable: - Office equipment: 3 years