Answered step by step

Verified Expert Solution

Question

1 Approved Answer

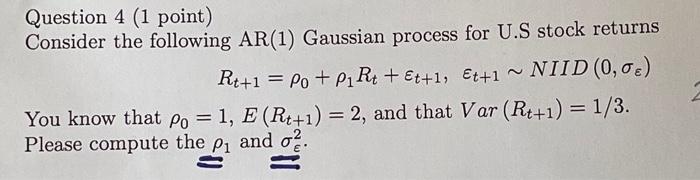

Question 4 (1 point) Consider the following AR(1) Gaussian process for U.S stock returns Rt+1 = Po + P Rt + Et+1, Et+1 ~ NIID

Question 4 (1 point) Consider the following AR(1) Gaussian process for U.S stock returns Rt+1 = Po + P Rt + Et+1, Et+1 ~ NIID (0,0%) You know that po = 1, E (Rt+1) = 2, and that Var (Rt+1) = 1/3. Please compute the p and .

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptocurrency 2 Manuscripts How To Make Money With Bitcoin How To Make Money With Ethereum

Authors: David Blake

1st Edition

1981675159, 978-1981675159