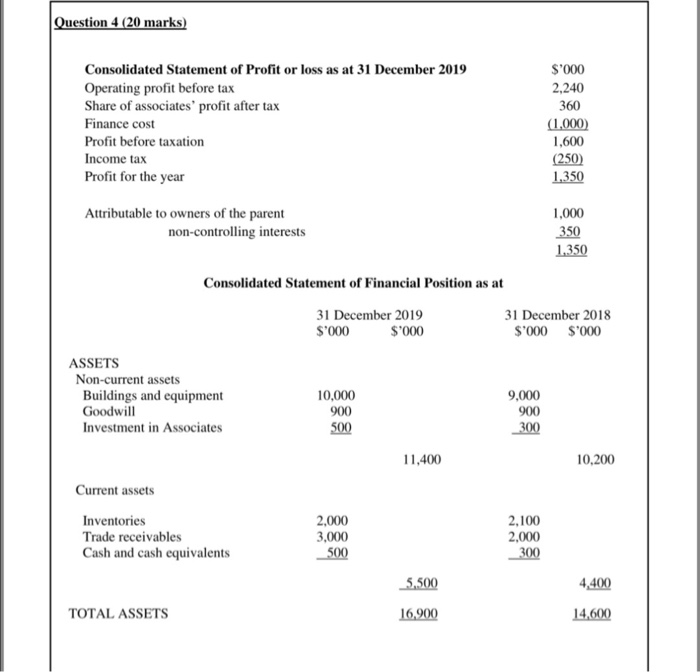

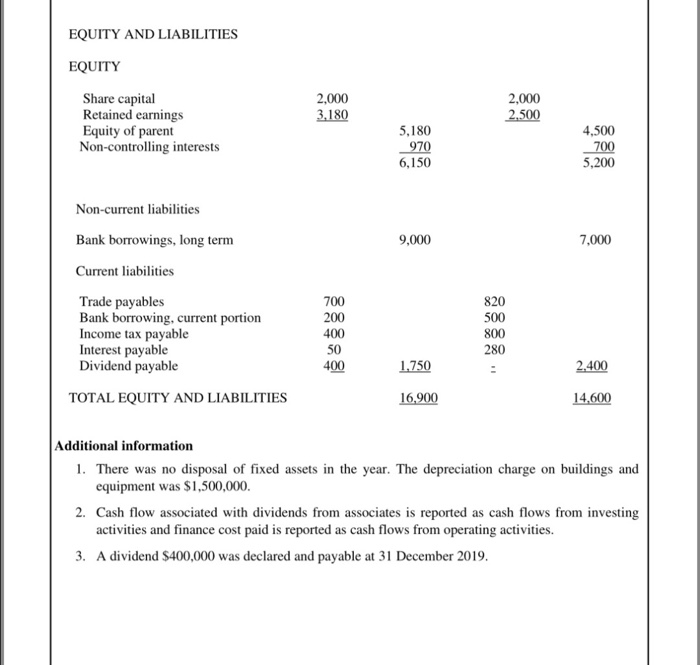

Question 4 (20 marks) Consolidated Statement of Profit or loss as at 31 December 2019 Operating profit before tax Share of associates' profit after tax Finance cost Profit before taxation Income tax Profit for the year $'000 2,240 360 (1,000) 1,600 (250) 1,350 Attributable to owners of the parent 1,000 non-controlling interests 350 1.350 Consolidated Statement of Financial Position as at 31 December 2019 31 December 2018 $'000 $'000 $'000 $'000 ASSETS Non-current assets Buildings and equipment Goodwill Investment in Associates 10,000 900 500 9,000 900 300 11,400 10,200 Current assets Inventories Trade receivables Cash and cash equivalents 2,000 3,000 500 2,100 2,000 300 5,500 4.400 TOTAL ASSETS 16,900 14,600 EQUITY AND LIABILITIES EQUITY 2,000 3,180 2.000 2.500 Share capital Retained earnings Equity of parent Non-controlling interests 5,180 970 6,150 4,500 700 5,200 Non-current liabilities 9,000 7,000 Bank borrowings, long term Current liabilities Trade payables Bank borrowing, current portion Income tax payable Interest payable Dividend payable TOTAL EQUITY AND LIABILITIES 700 200 400 50 400 820 500 800 280 1.750 2.400 16,900 14,600 Additional information 1. There was no disposal of fixed assets in the year. The depreciation charge on buildings and equipment was $1,500,000 2. Cash flow associated with dividends from associates is reported as cash flows from investing activities and finance cost paid is reported as cash flows from operating activities. 3. A dividend $400,000 was declared and payable at 31 December 2019. Required 1). Explain whether inventories increase or decrease during 2019 meaning the group had more cash or less cash (2 marks). (2). Bank borrowing is reported as Financing Activities. Explain in what situation finance cost paid may be reported as Operating Activities? (2 marks) (3). Prepare a consolidated statement of cash flows, using the indirect method for the year ended 31 December 2019 as required by IAS 7 (show all calculations). (16 marks) Question 4 (20 marks) Consolidated Statement of Profit or loss as at 31 December 2019 Operating profit before tax Share of associates' profit after tax Finance cost Profit before taxation Income tax Profit for the year $'000 2,240 360 (1,000) 1,600 (250) 1,350 Attributable to owners of the parent 1,000 non-controlling interests 350 1.350 Consolidated Statement of Financial Position as at 31 December 2019 31 December 2018 $'000 $'000 $'000 $'000 ASSETS Non-current assets Buildings and equipment Goodwill Investment in Associates 10,000 900 500 9,000 900 300 11,400 10,200 Current assets Inventories Trade receivables Cash and cash equivalents 2,000 3,000 500 2,100 2,000 300 5,500 4.400 TOTAL ASSETS 16,900 14,600 EQUITY AND LIABILITIES EQUITY 2,000 3,180 2.000 2.500 Share capital Retained earnings Equity of parent Non-controlling interests 5,180 970 6,150 4,500 700 5,200 Non-current liabilities 9,000 7,000 Bank borrowings, long term Current liabilities Trade payables Bank borrowing, current portion Income tax payable Interest payable Dividend payable TOTAL EQUITY AND LIABILITIES 700 200 400 50 400 820 500 800 280 1.750 2.400 16,900 14,600 Additional information 1. There was no disposal of fixed assets in the year. The depreciation charge on buildings and equipment was $1,500,000 2. Cash flow associated with dividends from associates is reported as cash flows from investing activities and finance cost paid is reported as cash flows from operating activities. 3. A dividend $400,000 was declared and payable at 31 December 2019. Required 1). Explain whether inventories increase or decrease during 2019 meaning the group had more cash or less cash (2 marks). (2). Bank borrowing is reported as Financing Activities. Explain in what situation finance cost paid may be reported as Operating Activities? (2 marks) (3). Prepare a consolidated statement of cash flows, using the indirect method for the year ended 31 December 2019 as required by IAS 7 (show all calculations). (16 marks)