Answered step by step

Verified Expert Solution

Question

1 Approved Answer

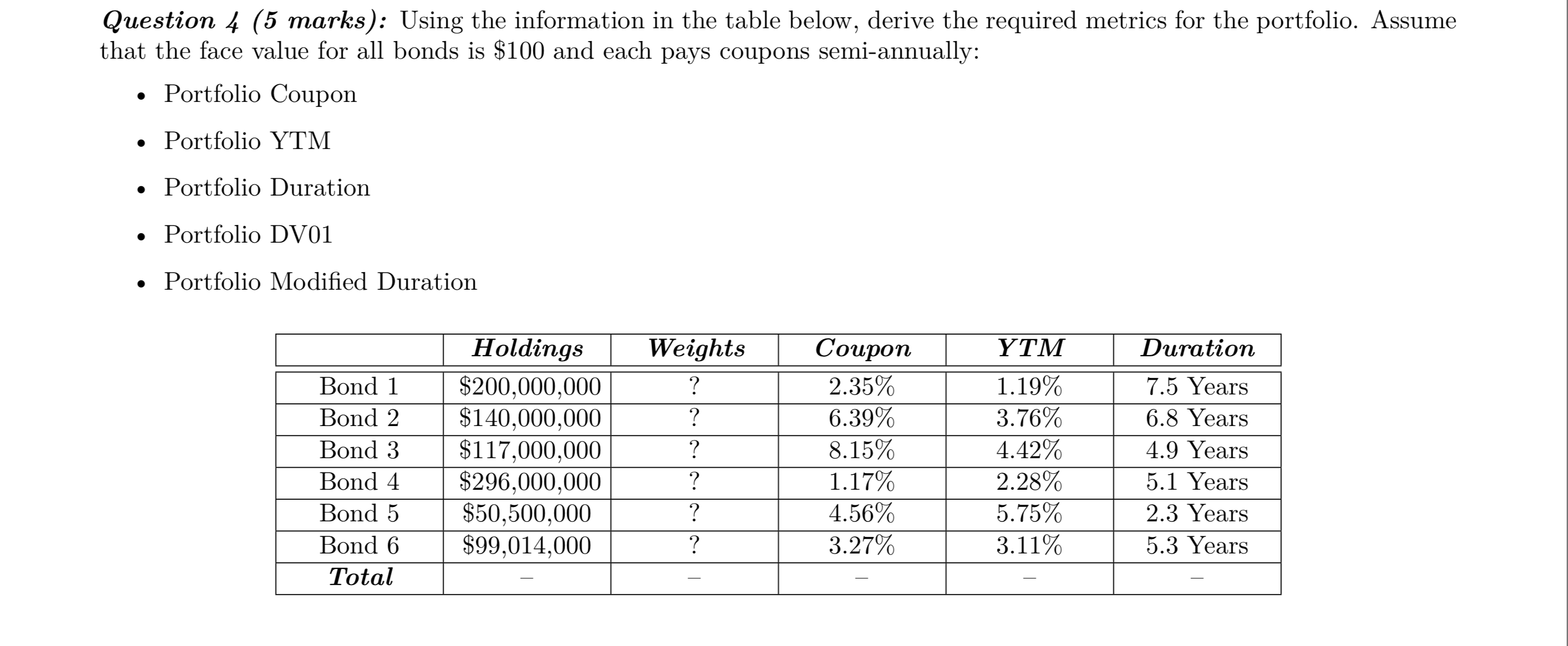

Question 4 (5 marks): Using the information in the table below, derive the required metrics for the portfolio. Assume that the face value for

Question 4 (5 marks): Using the information in the table below, derive the required metrics for the portfolio. Assume that the face value for all bonds is $100 and each pays coupons semi-annually: Portfolio Coupon Portfolio YTM Portfolio Duration Portfolio DV01 Portfolio Modified Duration Holdings Weights Coupon YTM Duration Bond 1 $200,000,000 ? 2.35% 1.19% 7.5 Years Bond 2 $140,000,000 ? 6.39% 3.76% 6.8 Years Bond 3 $117,000,000 ? 8.15% 4.42% 4.9 Years Bond 4 $296,000,000 ? 1.17% 2.28% 5.1 Years Bond 5 $50,500,000 ? 4.56% 5.75% 2.3 Years Bond 6 $99,014,000 ? 3.27% 3.11% 5.3 Years Total

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding financial statements

Authors: Lyn M. Fraser, Aileen Ormiston

9th Edition

136086241, 978-0136086246