Answered step by step

Verified Expert Solution

Question

1 Approved Answer

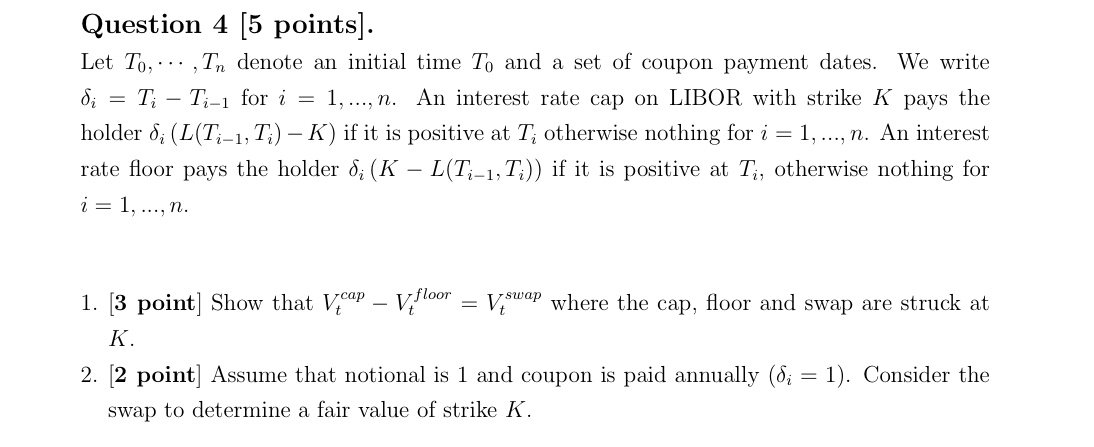

Question 4 [ 5 points ] . Let T 0 , cdots, T n denote an initial time T 0 and a set of coupon

Question points

Let cdots, denote an initial time and a set of coupon payment dates. We write for dots, An interest rate cap on LIBOR with strike pays the holder if it is positive at otherwise nothing for dots, An interest rate floor pays the holder if it is positive at otherwise nothing for dots,

point

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Secured Finance Transactions

Authors: Dominic RM Griffiths

2nd Edition

1787425142, 978-1787425149