Answered step by step

Verified Expert Solution

Question

1 Approved Answer

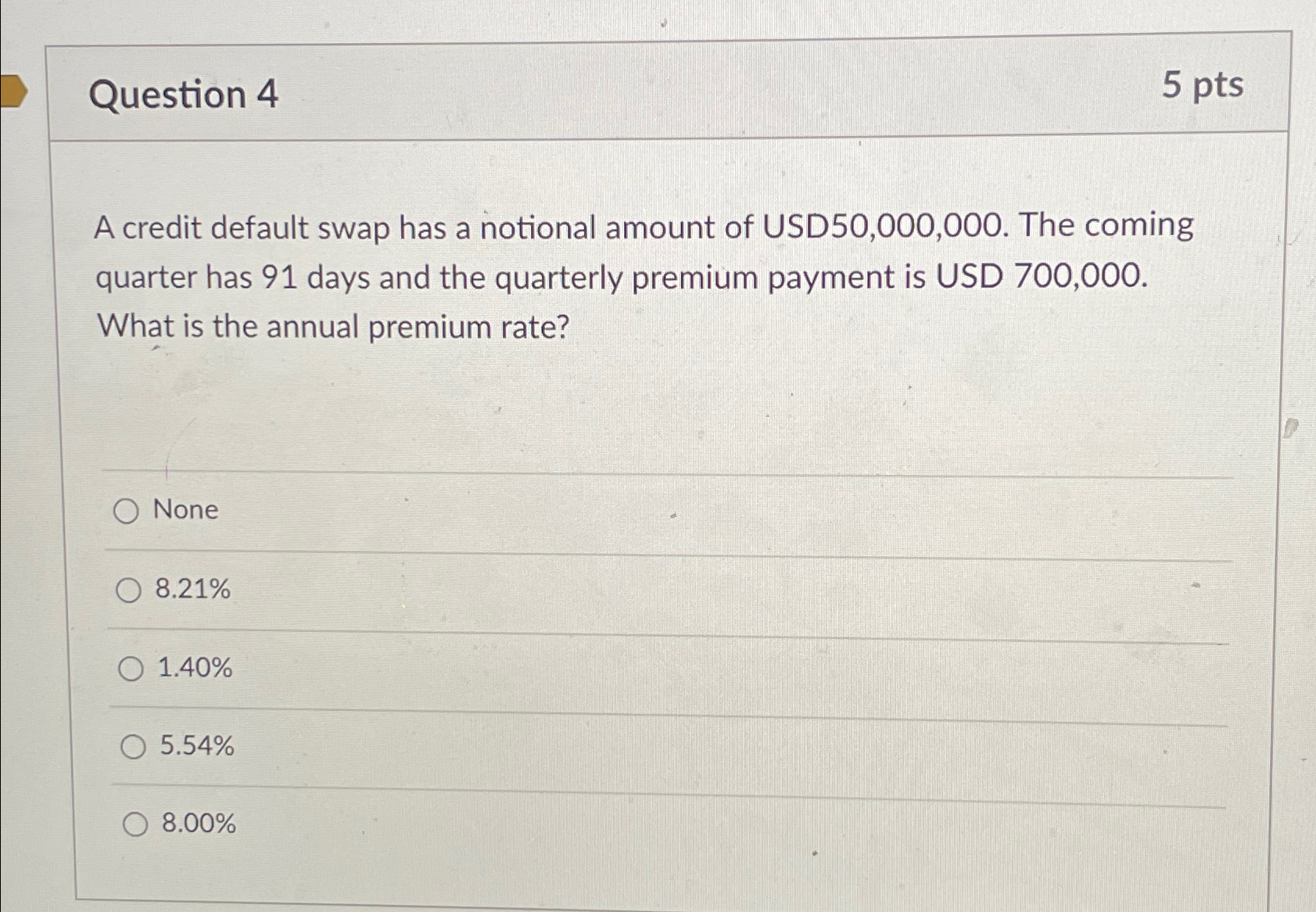

Question 4 5 pts A credit default swap has a notional amount of USD50,000,000. The coming quarter has 91 days and the quarterly premium

Question 4 5 pts A credit default swap has a notional amount of USD50,000,000. The coming quarter has 91 days and the quarterly premium payment is USD 700,000. What is the annual premium rate? O None 8.21% 1.40% 5.54% 8.00%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Principles and Applications

Authors: Sheridan Titman, Arthur Keown, John Martin

12th edition

133423824, 978-0133423822