Answered step by step

Verified Expert Solution

Question

1 Approved Answer

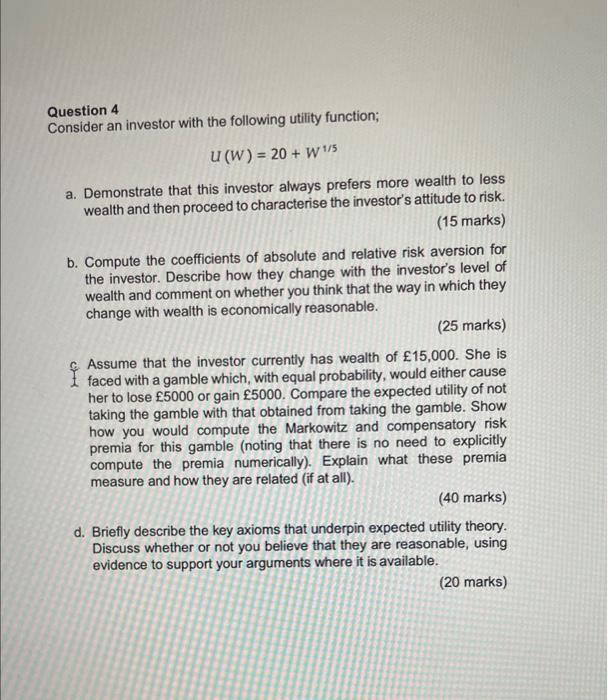

Question 4 Consider an investor with the following utility function; U(W)=20+W1/5 a. Demonstrate that this investor always prefers more wealth to less wealth and then

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Theory And Practice

Authors: Prasanna Chandra

10th Edition

9353166527, 978-9353166526