Question

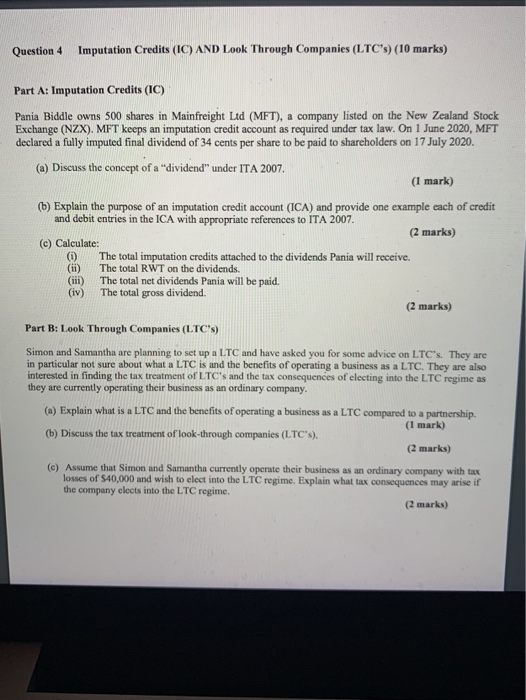

Question 4 Imputation Credits (IC) AND Look Through Companies (LTC's) (10 marks) Part A: Imputation Credits (IC) Pania Biddle owns 500 shares in Mainfreight Ltd

Question 4 Imputation Credits (IC) AND Look Through Companies (LTC's) (10 marks) Part A: Imputation Credits (IC) Pania Biddle owns 500 shares in Mainfreight Ltd (MFT), a company listed on the New Zealand Stock Exchange (NZX). MFT keeps an imputation credit account as required under tax law. On 1 June 2020, MFT declared a fully imputed final dividend of 34 cents per share to be paid to shareholders on 17 July 2020. (a) Discuss the concept of a "dividend" under ITA 2007. (1 mark) (6) Explain the purpose of an imputation credit account (ICA) and provide one example each of credit and debit entries in the ICA with appropriate references to ITA 2007. (2 marks) (c) Calculate: (0) The total imputation credits attached to the dividends Pania will receive. (11) The total RWT on the dividends. (iii) The total net dividends Pania will be paid. (iv) The total gross dividend (2 marks) Part B: Look Through Companies (LTC's) Simon and Samantha are planning to set up a LTC and have asked you for some advice on LTC's. They are in particular not sure about what a LTC is and the benefits of operating a business as a LTC. They are also interested in finding the tax treatment of LTC's and the tax consequences of electing into the LTC regime as they are currently operating their business as an ordinary company. (a) Explain what is a LTC and the benefits of operating a business as a LTC compared to a partnership (1 mark) (6) Discuss the tax treatment of look-through companies (LTC's). (2 marks) (c) Assume that Simon and Samantha currently operate their business as an ordinary company with tax losses of $40,000 and wish to clect into the LTC regime. Explain what tax consequences may arise if the company clocts into the LTC regime. (2 marks)

Question 4 Imputation Credits (IC) AND Look Through Companies (LTC's) (10 marks) Part A: Imputation Credits (IC) Pania Biddle owns 500 shares in Mainfreight Ltd (MFT), a company listed on the New Zealand Stock Exchange (NZX). MFT keeps an imputation credit account as required under tax law. On 1 June 2020, MFT declared a fully imputed final dividend of 34 cents per share to be paid to shareholders on 17 July 2020. (a) Discuss the concept of a "dividend" under ITA 2007. (1 mark) (6) Explain the purpose of an imputation credit account (ICA) and provide one example each of credit and debit entries in the ICA with appropriate references to ITA 2007. (2 marks) (c) Calculate: (0) The total imputation credits attached to the dividends Pania will receive. (11) The total RWT on the dividends. (iii) The total net dividends Pania will be paid. (iv) The total gross dividend (2 marks) Part B: Look Through Companies (LTC's) Simon and Samantha are planning to set up a LTC and have asked you for some advice on LTC's. They are in particular not sure about what a LTC is and the benefits of operating a business as a LTC. They are also interested in finding the tax treatment of LTC's and the tax consequences of electing into the LTC regime as they are currently operating their business as an ordinary company. (a) Explain what is a LTC and the benefits of operating a business as a LTC compared to a partnership (1 mark) (6) Discuss the tax treatment of look-through companies (LTC's). (2 marks) (c) Assume that Simon and Samantha currently operate their business as an ordinary company with tax losses of $40,000 and wish to clect into the LTC regime. Explain what tax consequences may arise if the company clocts into the LTC regime. (2 marks) Question 4 Imputation Credits (IC) AND Look Through Companies (LTC's) (10 marks) Part A: Imputation Credits (IC) Pania Biddle owns 500 shares in Mainfreight Ltd (MFT), a company listed on the New Zealand Stock Exchange (NZX). MFT keeps an imputation credit account as required under tax law. On 1 June 2020, MFT declared a fully imputed final dividend of 34 cents per share to be paid to shareholders on 17 July 2020. (a) Discuss the concept of a "dividend" under ITA 2007. (1 mark) (6) Explain the purpose of an imputation credit account (ICA) and provide one example each of credit and debit entries in the ICA with appropriate references to ITA 2007. (2 marks) (c) Calculate: (0) The total imputation credits attached to the dividends Pania will receive. (11) The total RWT on the dividends. (iii) The total net dividends Pania will be paid. (iv) The total gross dividend (2 marks) Part B: Look Through Companies (LTC's) Simon and Samantha are planning to set up a LTC and have asked you for some advice on LTC's. They are in particular not sure about what a LTC is and the benefits of operating a business as a LTC. They are also interested in finding the tax treatment of LTC's and the tax consequences of electing into the LTC regime as they are currently operating their business as an ordinary company. (a) Explain what is a LTC and the benefits of operating a business as a LTC compared to a partnership (1 mark) (6) Discuss the tax treatment of look-through companies (LTC's). (2 marks) (c) Assume that Simon and Samantha currently operate their business as an ordinary company with tax losses of $40,000 and wish to clect into the LTC regime. Explain what tax consequences may arise if the company clocts into the LTC regime. (2 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Ethics

Authors: Iris Stuart

1st Edition

1118542401, 9781118542408