Answered step by step

Verified Expert Solution

Question

1 Approved Answer

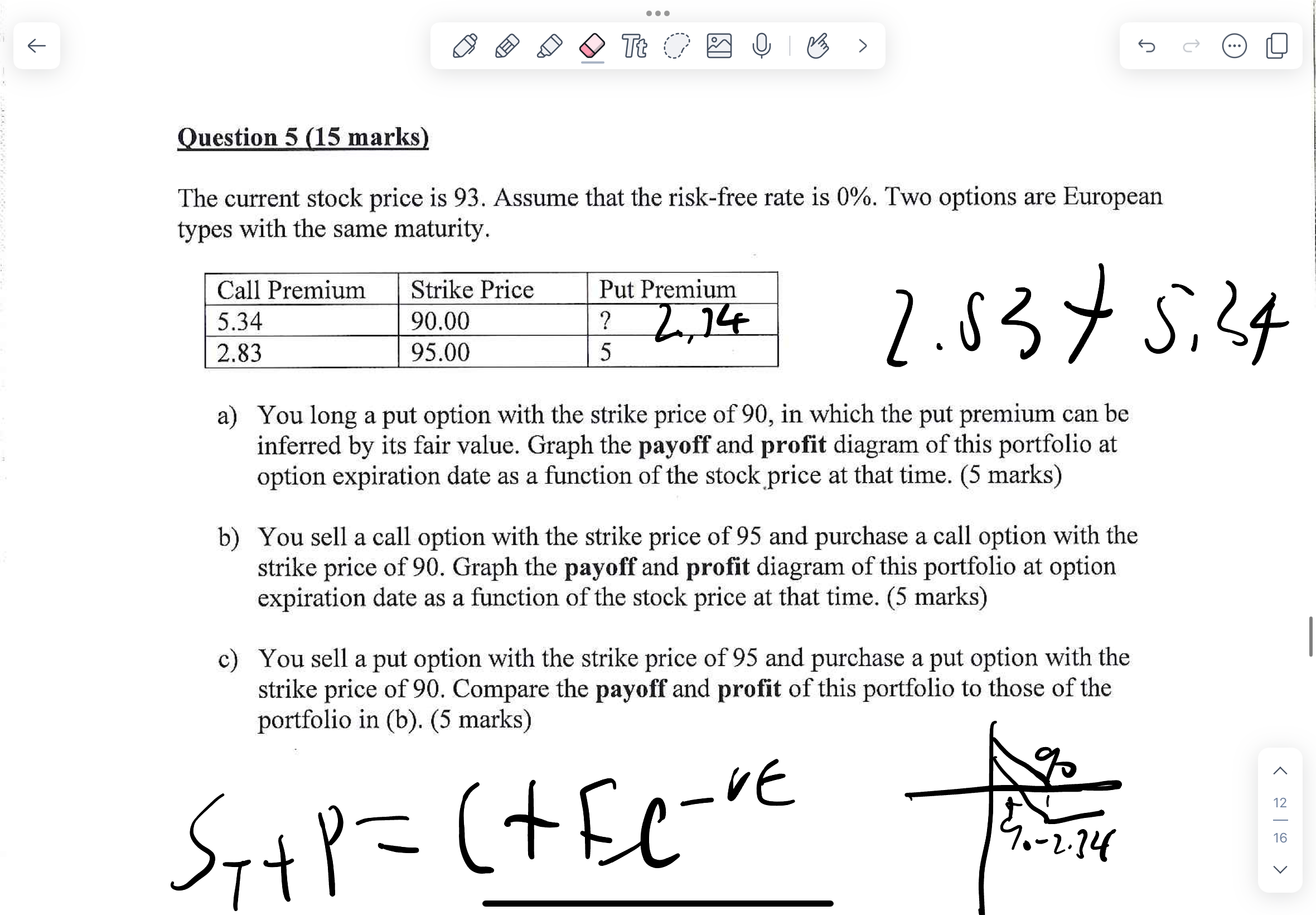

Question 5 ( 1 5 marks ) The current stock price is 9 3 . Assume that the risk - free rate is 0 %

Question marks

The current stock price is Assume that the riskfree rate is Two options are European

types with the same maturity.

a You long a put option with the strike price of in which the put premium can be

inferred by its fair value. Graph the payoff and profit diagram of this portfolio at

option expiration date as a function of the stock price at that time. marks

b You sell a call option with the strike price of and purchase a call option with the

strike price of Graph the payoff and profit diagram of this portfolio at option

expiration date as a function of the stock price at that time. marks

c You sell a put option with the strike price of and purchase a put option with the

strike price of Compare the payoff and profit of this portfolio to those of the

portfolio in b marks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cases In Financial Reporting

Authors: Ellen Engel, D. Eric Hirst, Mary Lea McAnally

7th Edition

1934319791, 9781934319796