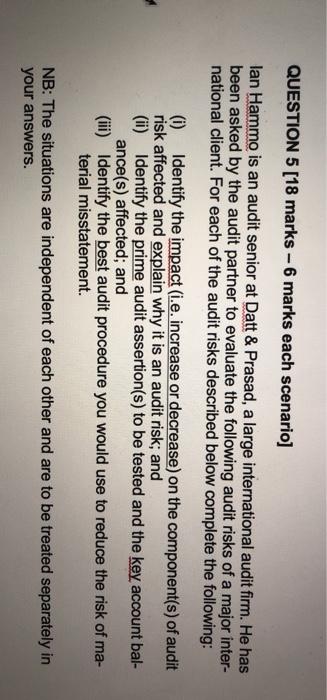

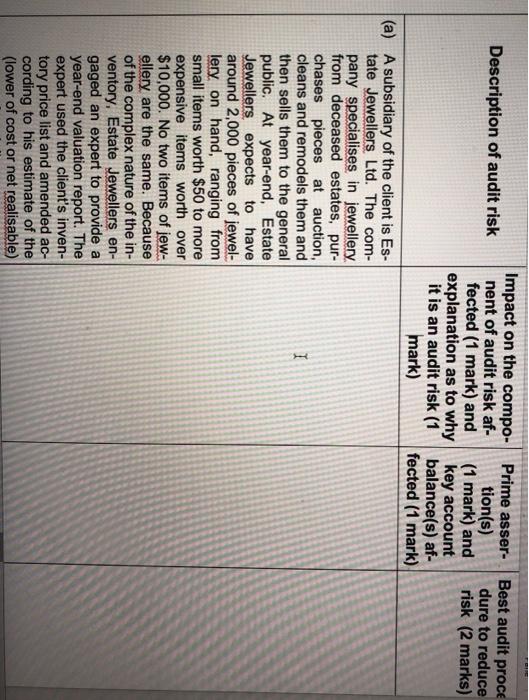

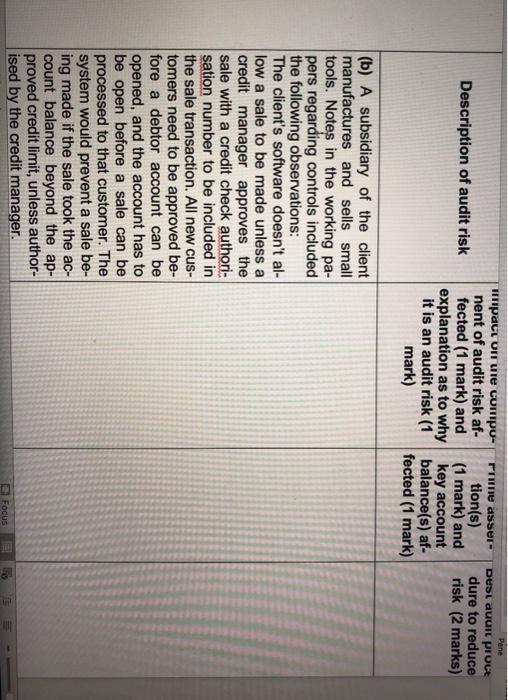

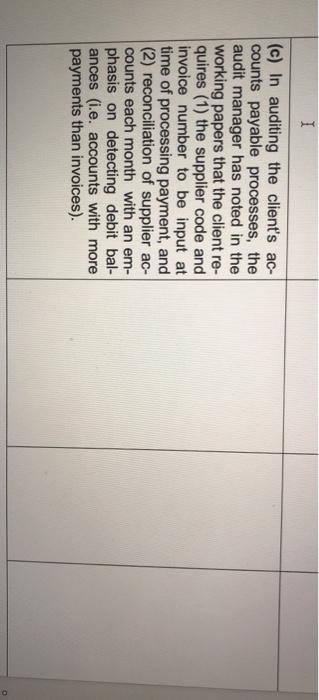

QUESTION 5 [18 marks - 6 marks each scenario] lan Hammo is an audit senior at Datt & Prasad, a large international audit firm. He has been asked by the audit partner to evaluate the following audit risks of a major inter- national client. For each of the audit risks described below complete the following: (i) Identify the impact (i.e. increase or decrease) on the component(s) of audit risk affected and explain why it is an audit risk; and (ii) Identify the prime audit assertion(s) to be tested and the key account bal- ance(s) affected; and (iii) Identify the best audit procedure you would use to reduce the risk of ma- terial misstatement. NB: The situations are independent of each other and are to be treated separately in your answers. Description of audit risk Impact on the compo Prime asser- nent of audit risk af- tion(s) fected (1 mark) and (1 mark) and explanation as to why key account it is an audit risk (1 balance(s) af- mark) fected (1 mark) Best audit proce dure to reduce risk (2 marks) I (a) A subsidiary of the client is Es- tate Jewellers Ltd. The com- pany specialises in jewellery from deceased estates, pur- chases pieces at auction, cleans and remodels them and then sells them to the general public. At year-end, Estate Jewellers expects to have around 2,000 pieces of jewel- lery on hand, ranging from small items worth $50 to more expensive items worth over $10,000. No two items of jew- ellery are the same. Because of the complex nature of the in- ventory. Estate Jewellers en- gaged an expert to provide a year-end valuation report. The expert used the client's inven- tory price list and amended ac- cording to his estimate of the (lower of cost or net realisable) Pene Dust auui prout dure to reduce risk (2 marks) Prire asser- nent of audit risk af tion(s) fected (1 mark) and (1 mark) and explanation as to why key account it is an audit risk (1 balance(s) af- mark) fected (1 mark) Description of audit risk (b) A subsidiary of the client manufactures and sells small tools. Notes in the working pa- pers regarding controls included the following observations: The client's software doesn't al- low a sale to be made unless a credit manager approves the sale with a credit check authori- sation number to be included in the sale transaction. All new cus- tomers need to be approved be- fore a debtor account can be opened, and the account has to be open before a sale can be processed to that customer. The system would prevent a sale be- ing made if the sale took the ac- count balance beyond the ap- proved credit limit, unless author- ised by the credit manager. Focus I (c) In auditing the client's ac- counts payable processes, the audit manager has noted in the working papers that the client re- quires (1) the supplier code and invoice number to be input at time of processing payment, and (2) reconciliation of supplier ac- counts each month with an em- phasis on detecting debit bal- ances (.e. accounts with more payments than invoices). QUESTION 5 [18 marks - 6 marks each scenario] lan Hammo is an audit senior at Datt & Prasad, a large international audit firm. He has been asked by the audit partner to evaluate the following audit risks of a major inter- national client. For each of the audit risks described below complete the following: (i) Identify the impact (i.e. increase or decrease) on the component(s) of audit risk affected and explain why it is an audit risk; and (ii) Identify the prime audit assertion(s) to be tested and the key account bal- ance(s) affected; and (iii) Identify the best audit procedure you would use to reduce the risk of ma- terial misstatement. NB: The situations are independent of each other and are to be treated separately in your answers. Description of audit risk Impact on the compo Prime asser- nent of audit risk af- tion(s) fected (1 mark) and (1 mark) and explanation as to why key account it is an audit risk (1 balance(s) af- mark) fected (1 mark) Best audit proce dure to reduce risk (2 marks) I (a) A subsidiary of the client is Es- tate Jewellers Ltd. The com- pany specialises in jewellery from deceased estates, pur- chases pieces at auction, cleans and remodels them and then sells them to the general public. At year-end, Estate Jewellers expects to have around 2,000 pieces of jewel- lery on hand, ranging from small items worth $50 to more expensive items worth over $10,000. No two items of jew- ellery are the same. Because of the complex nature of the in- ventory. Estate Jewellers en- gaged an expert to provide a year-end valuation report. The expert used the client's inven- tory price list and amended ac- cording to his estimate of the (lower of cost or net realisable) Pene Dust auui prout dure to reduce risk (2 marks) Prire asser- nent of audit risk af tion(s) fected (1 mark) and (1 mark) and explanation as to why key account it is an audit risk (1 balance(s) af- mark) fected (1 mark) Description of audit risk (b) A subsidiary of the client manufactures and sells small tools. Notes in the working pa- pers regarding controls included the following observations: The client's software doesn't al- low a sale to be made unless a credit manager approves the sale with a credit check authori- sation number to be included in the sale transaction. All new cus- tomers need to be approved be- fore a debtor account can be opened, and the account has to be open before a sale can be processed to that customer. The system would prevent a sale be- ing made if the sale took the ac- count balance beyond the ap- proved credit limit, unless author- ised by the credit manager. Focus I (c) In auditing the client's ac- counts payable processes, the audit manager has noted in the working papers that the client re- quires (1) the supplier code and invoice number to be input at time of processing payment, and (2) reconciliation of supplier ac- counts each month with an em- phasis on detecting debit bal- ances (.e. accounts with more payments than invoices)

![For Mowen/hansen/heitgers Cornerstones Of Managerial Accounting, 6th Edition, [instant Access]](https://dsd5zvtm8ll6.cloudfront.net/si.question.images/book_images/2022/04/6257c87e3025b_1256257c87dcfa77.jpg)