Answered step by step

Verified Expert Solution

Question

1 Approved Answer

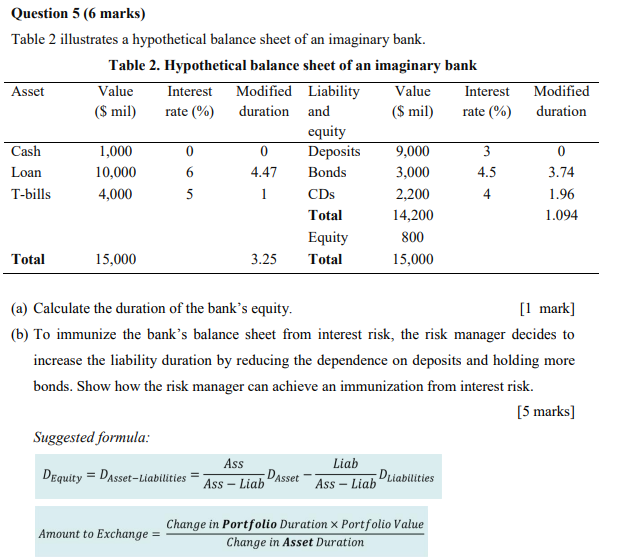

Question 5 (6 marks) Table 2 illustrates a hypothetical balance sheet of an imaginary bank. Table 2. Hypothetical balance sheet of an imaginary bank

Question 5 (6 marks) Table 2 illustrates a hypothetical balance sheet of an imaginary bank. Table 2. Hypothetical balance sheet of an imaginary bank Asset Value Interest Modified Liability Value Interest Modified ($ mil) rate (%) duration and ($ mil) rate (%) duration equity Cash 1,000 0 0 Deposits 9,000 3 0 Loan 10,000 6 4.47 Bonds 3,000 4.5 3.74 T-bills 4,000 5 1 CDs 2,200 4 1.96 Total 14,200 1.094 Equity 800 3.25 Total 15,000 Total 15,000 (a) Calculate the duration of the bank's equity. [1 mark] (b) To immunize the bank's balance sheet from interest risk, the risk manager decides to increase the liability duration by reducing the dependence on deposits and holding more bonds. Show how the risk manager can achieve an immunization from interest risk. Suggested formula: DEquity =DAsset-Liabilities Ass Ass-Liab DAsset Liab Ass Liab DLiabilities Amount to Exchange = Change in Portfolio Duration x Portfolio Value Change in Asset Duration [5 marks]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuation Measuring and managing the values of companies

Authors: Mckinsey, Tim Koller, Marc Goedhart, David Wessel

5th edition

978-0470424650, 9780470889930, 470424656, 470889934, 978-047042470