Question 5 One difference between monopolistic competition and oligopoly is that firms in monopolistic competition are assumed to A cooperate in setting price and output

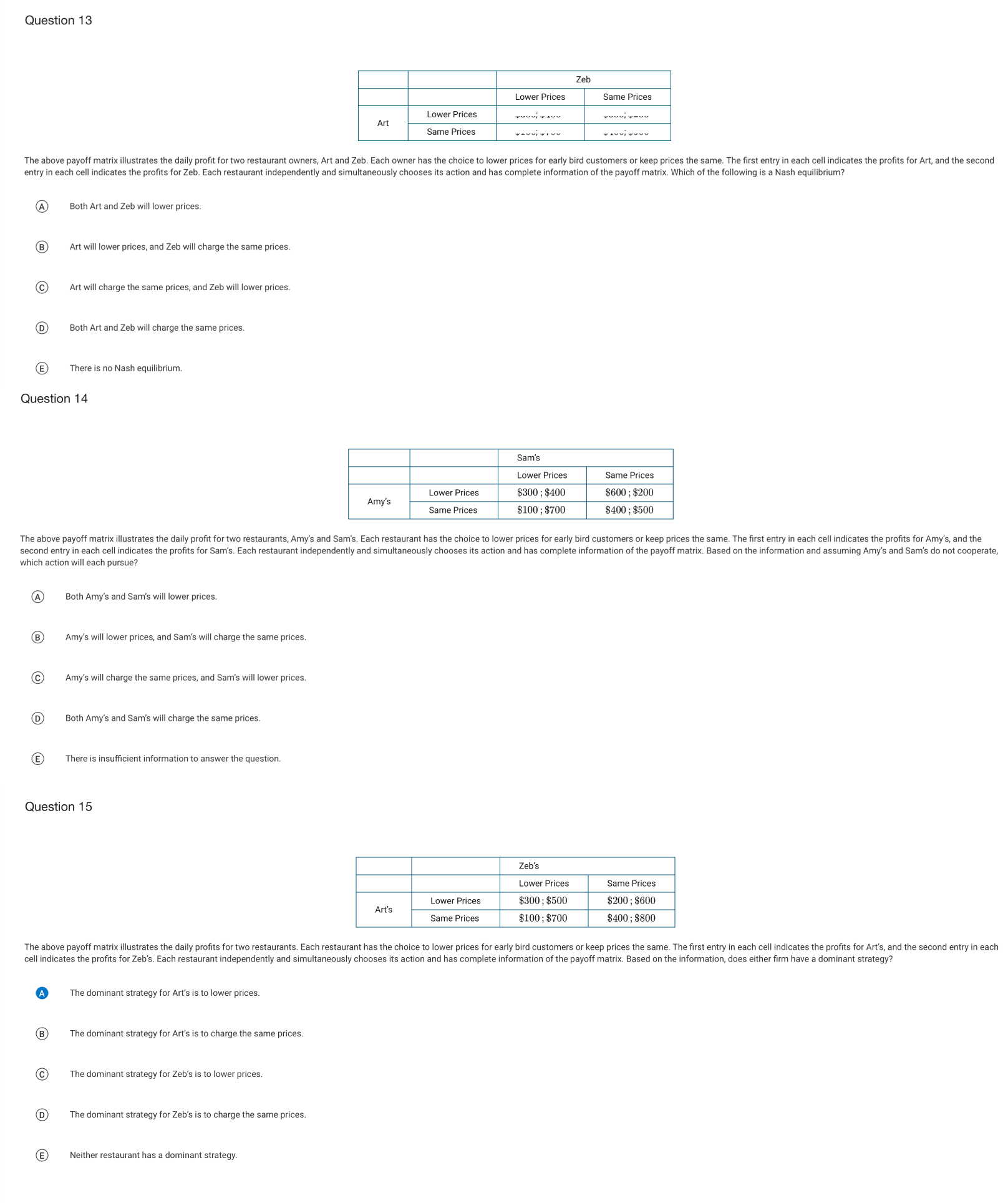

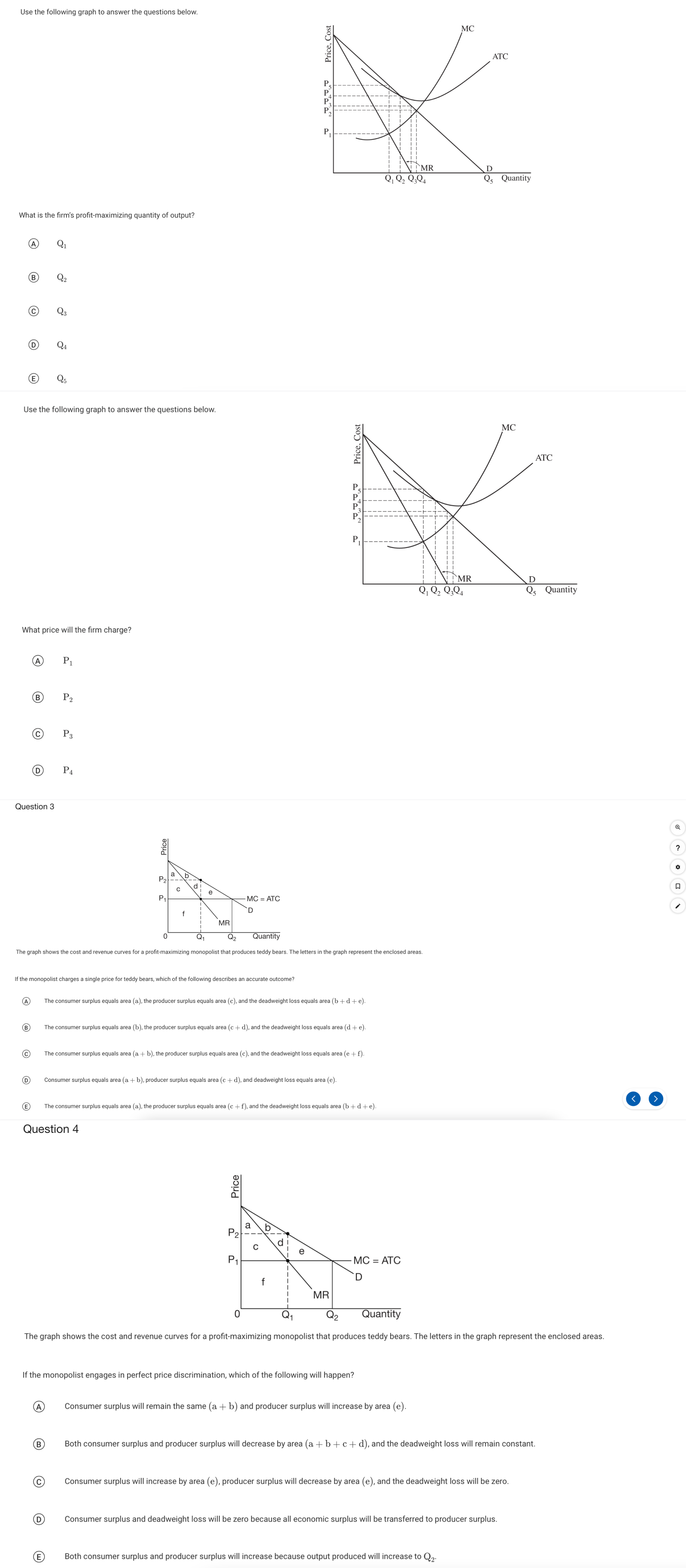

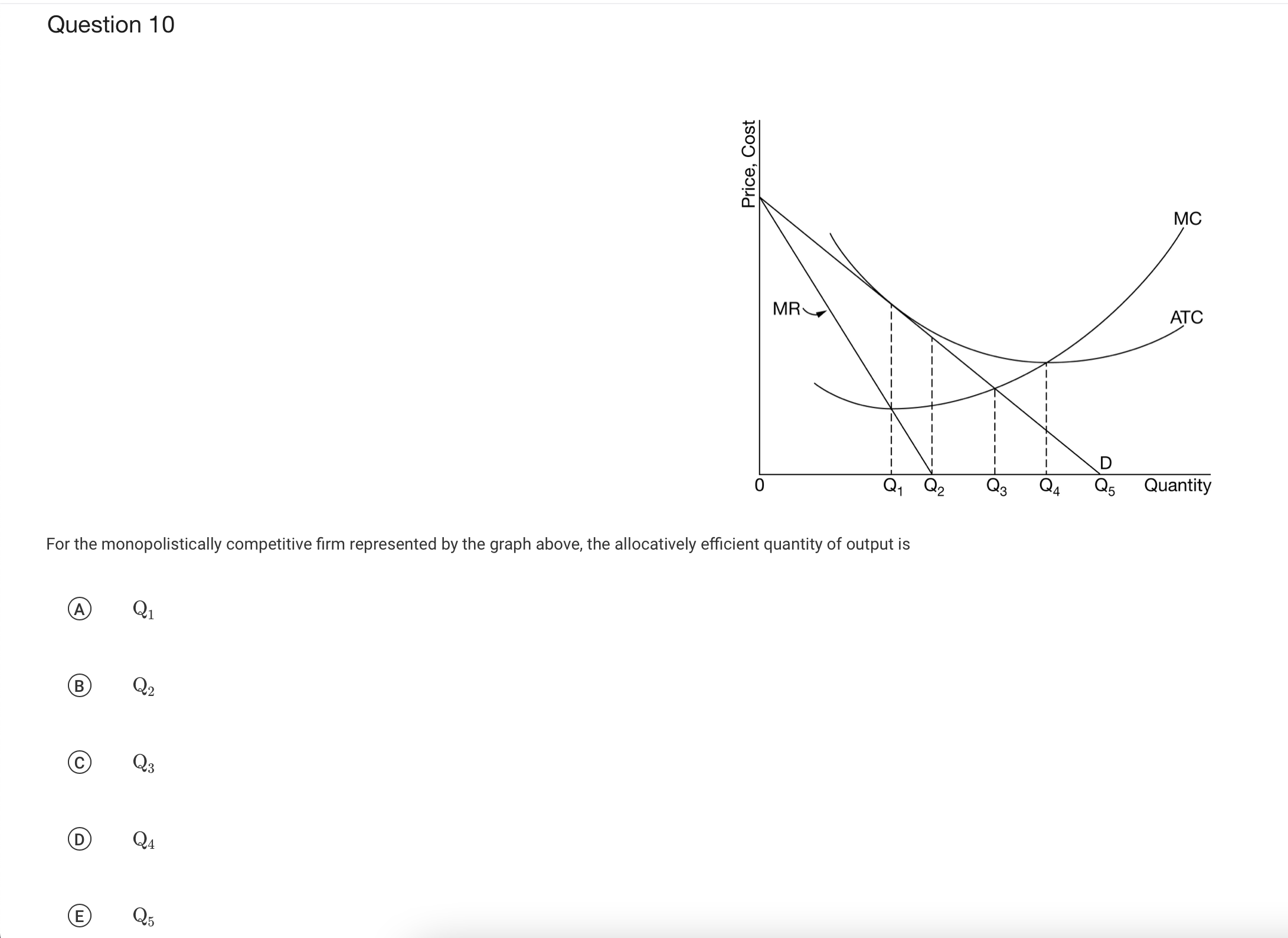

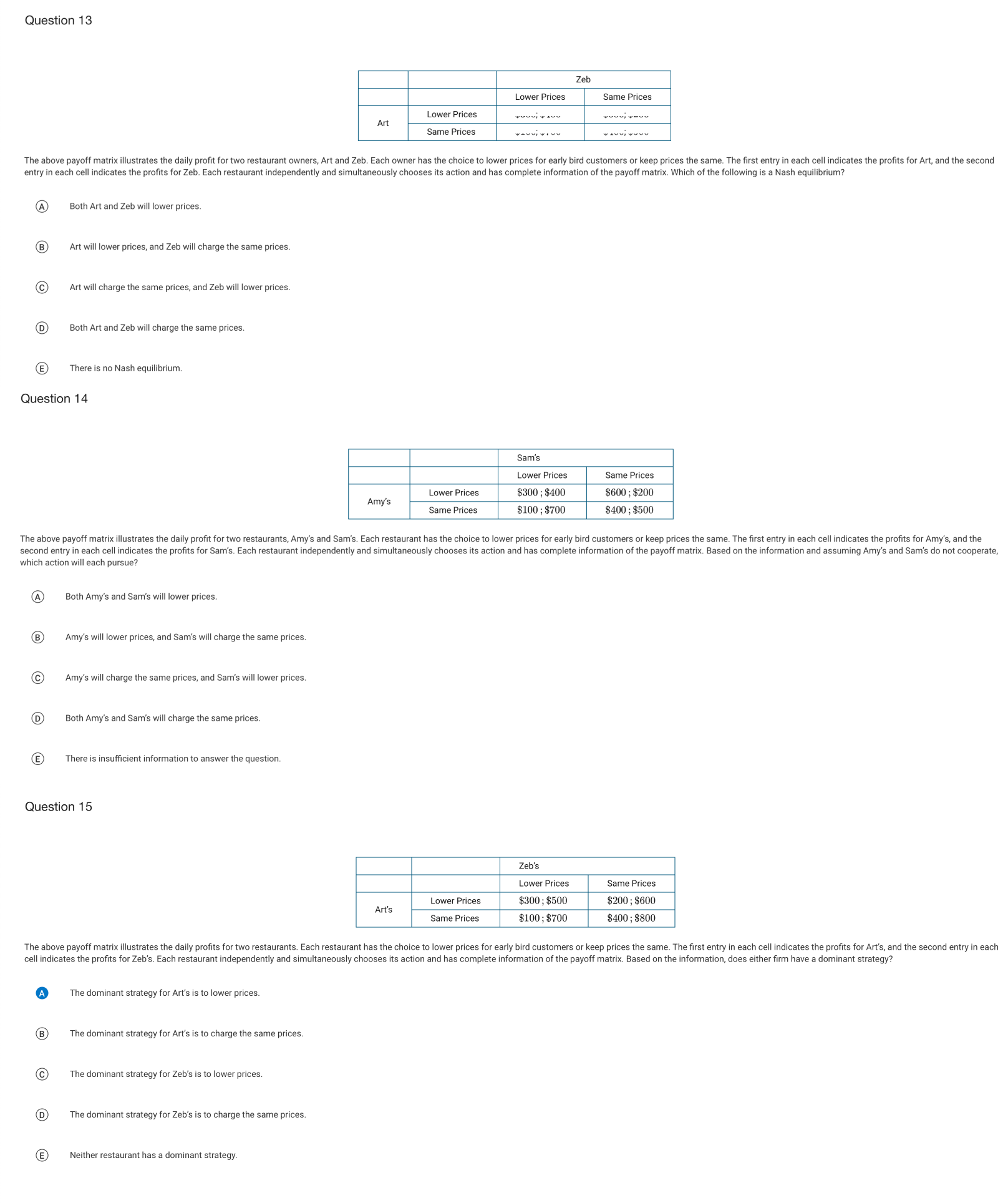

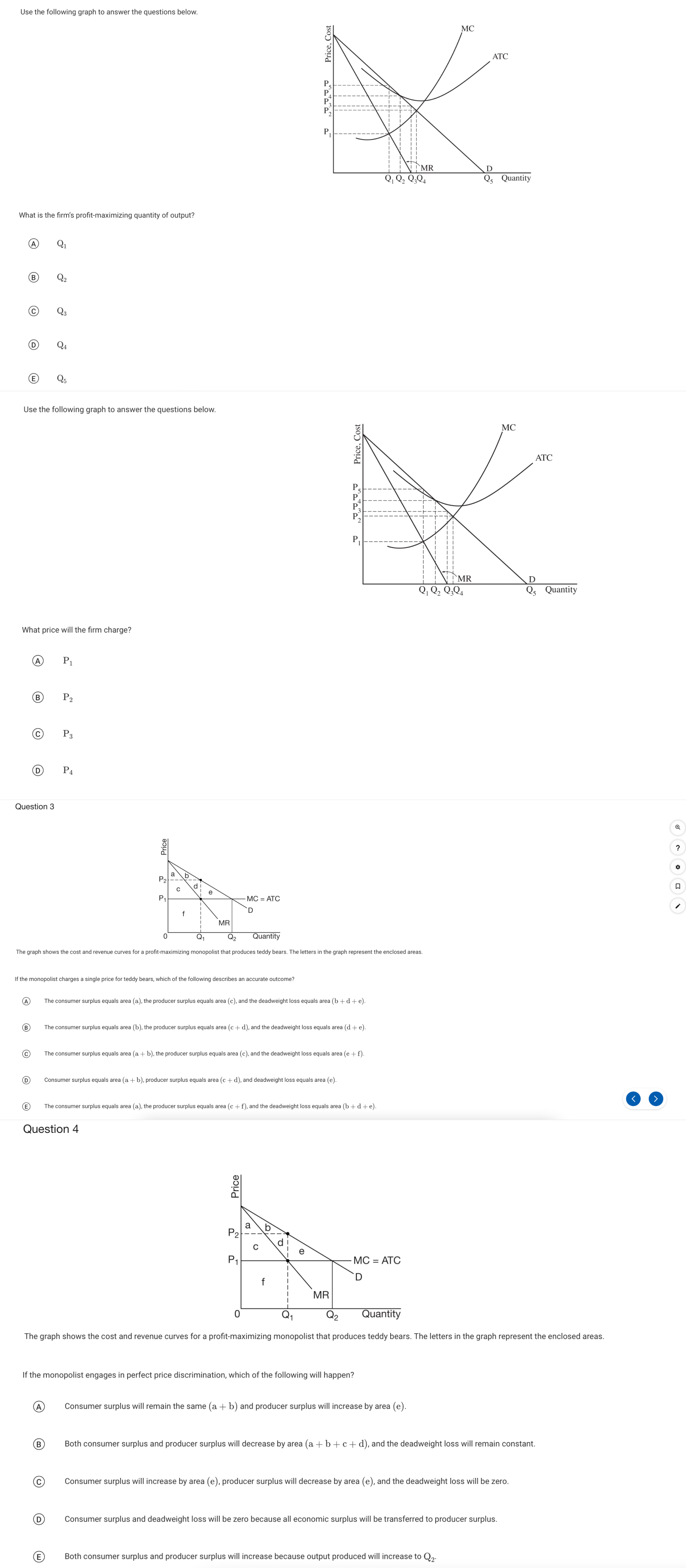

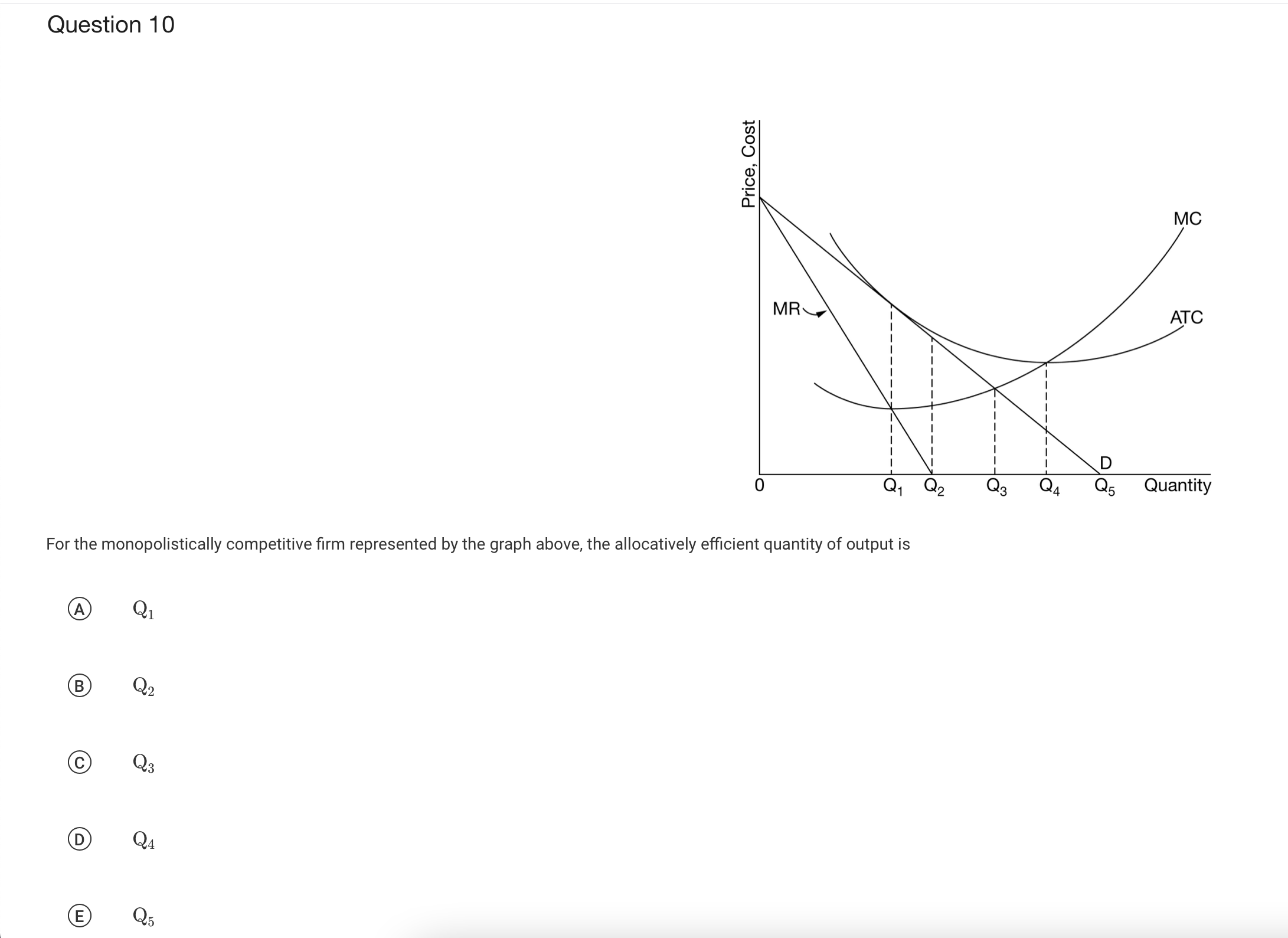

Question 5 One difference between monopolistic competition and oligopoly is that firms in monopolistic competition are assumed to A cooperate in setting price and output B act independently in setting price and output C be interdependent D face high barriers to entry E be price takers Question 6 Which of the following explains why imperfectly competitive markets are inefficient? A Total costs increase as output increases. B Price is greater than marginal cost. C Firms do not earn zero economic profit. D Firms incur high start-up costs when setting up their factories. E Firms use relatively more capital than labor to produce goods or services. Question 7 Which of the following is true in imperfectly competitive markets? A Firms produce standardized or identical products. B Firms enjoy economies of scale in production. C Firms produce output at constant marginal cost. D Firms must lower their product prices to sell additional units. E) New firms can easily enter or exit the market. Question 8 Which of the following is true of a natural monopoly? A) The average total cost is constant throughout the entire effective demand. B Marginal cost decreases throughout the entire effective demand. C The average total cost initially decreases and then increases throughout the entire effective demand. D The marginal cost initially increases and then decreases throughout the entire effective demand. E The average total cost decreases throughout the entire effective demand. Question 9 A firm with market power engages in price discrimination in order to A cover the cost of serving each consumer B increase its profits C charge a lower price D produce the allocationy efficient quantity increase consumer surplusQuestion 11 A monopolistically competitive firm's demand curve will be least elastic if A the number of rival firms producing very similar products increases B the number of rival firms producing more differentiated products increases C the number of rival firms producing very similar products decreases D the number of rival firms producing more differentiated products decreases E a monopolistically competitive firm's demand curve becomes perfectly elastic Question 12 Monopolistically competitive markets are characterized by A a large number of firms B economies of scale C standardized products (D mutual interdependence (E) positive economic profit in the long runQuestion 13 Zeb Lower Prices Same Prices Art Lower Prices Same Prices The above payoff matrix illustrates the daily profit for two restaurant owners, Art and Zeb. Each owner has the choice to lower prices for early bird customers or keep prices the same. The first entry in each cell indicates the profits for Art, and the second entry in each cell indicates the profits for Zeb. Each restaurant independently and simultaneously chooses its action and has complete information of the payoff matrix. Which of the following is a Nash equilibrium? A Both Art and Zeb will lower prices. B Art will lower prices, and Zeb will charge the same prices. C Art will charge the same prices, and Zeb will lower prices. D Both Art and Zeb will charge the same prices. E) There is no Nash equilibrium. Question 14 Sam's Lower Prices Same Prices Lower Prices $300 ; $400 $600 ; $200 Amy's Same Prices $100 ; $700 $400 ; $500 The above payoff matrix illustrates the daily profit for two restaurants, Amy's and Sam's. Each restaurant has the choice to lower prices for early bird customers or keep prices the same. The first entry in each cell indicates the profits for Amy's, and the second entry in each cell indicates the profits for Sam's. Each restaurant independently and simultaneously chooses its action and has complete information of the payoff matrix. Based on the information and assuming Amy's and Sam's do not cooperate, which action will each pursue? A Both Amy's and Sam's will lower prices. B Amy's will lower prices, and Sam's will charge the same prices. C Amy's will charge the same prices, and Sam's will lower prices. D Both Amy's and Sam's will charge the same prices. There is insufficient information to answer the question. Question 15 Zeb's Lower Prices Same Prices Lower Prices $300 ; $500 $200 ; $600 Art's Same Prices $100 ; $700 $400 ; $800 The above payoff matrix illustrates the daily profits for two restaurants. Each restaurant has the choice to lower prices for early bird customers or keep prices the same. The first entry in each cell indicates the profits for Art's, and the second entry in each ell indicates the profits for Zeb's. Each restaurant independently and simultaneously chooses its action and has complete information of the payoff matrix. Based on the information, does either firm have a dominant strategy? A The dominant strategy for Art's is to lower prices. B) The dominant strategy for Art's is to charge the same prices. C The dominant strategy for Zeb's is to lower prices. D The dominant strategy for Zeb's is to charge the same prices. E Neither restaurant has a dominant strategy.Use the following graph to answer the questions below. Price. Cost Q Quantity What is the firm's profit-maximizing quantity of output? (A) Q (B) C) Q D QA E) Use the following graph to answer the questions below. What price will the firm charge? (A) P1 B) P2 C P D PA Question 3 Price P 2 - MC = ATC MR Quantity The graph shows the cost and revenue curves for a profit-maximizing monopolist that produces teddy bears. The letters in the graph represent the enclosed areas. If the monopolist charges a single price for te urate outcome? A) The consumer surplus equals area (a), the producer surplus equals area (c), and the deadweight loss equals area (b + d + e). B The consumer surplus equals area (b), the producer surplus equals area (c + d), and the deadweight loss equals area (d + e). C The consumer surplus equals area (a + b), the produce is area (c), and the deadweight loss equals area (e + f). D Consumer surplus equals area (a + b), producer surplus equals area (c + d), and deadweight loss equals area (e). The consumer surplus equals area (a), the producer surplus equals area (c + f), and the deadweight loss equals area (b + d + e). Question 4 Price P2 P - MC = ATC MR Q. Q2 Quantity The graph shows the cost and revenue curves for a profit-maximizing monopolist that produces teddy bears. The letters in the graph represent the enclosed areas. If the monopolist engages in perfect price discrimination, which of the following will happen? A Consumer surplus will remain the same (a + b) and producer surplus will increase by area (e). B Both consumer surplus and producer surplus will decrease by area (a + b + c + d), and the deadweight loss will remain constant. C Consumer surplus will increase by area (e), producer surplus will decrease by area (e), and the deadweight loss will be zero. D Consumer surplus and deadweight loss will be zero because all economic surplus will be transferred to producer surplus. (E Both consumer surplus and producer surplus will increase because output produced will increase to Q2-Question 10 Price, Cost MC MR ATC D Q1 Q2 Q 3 QA Q5 Quantity For the monopolistically competitive firm represented by the graph above, the allocationy efficient quantity of output is A Q1 B Q2 C Q3 D QA E Q5

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance