Answered step by step

Verified Expert Solution

Question

1 Approved Answer

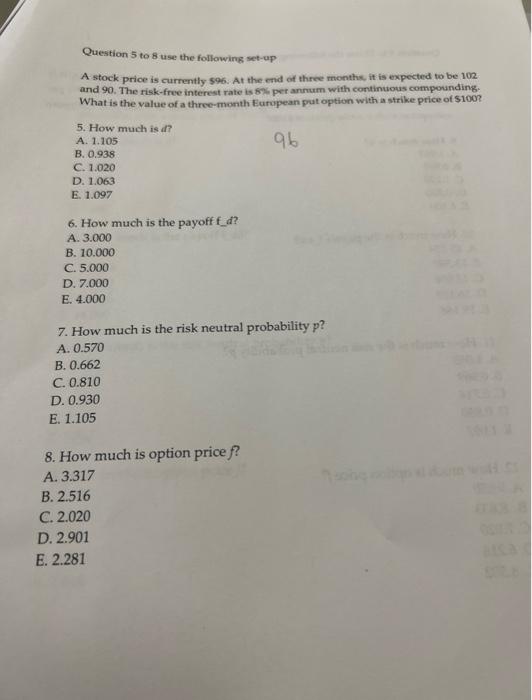

Question 5 to 8 use the following set-up A stock price is currently $96. At the end of three months, it is expected to be

Question 5 to 8 use the following set-up A stock price is currently $96. At the end of three months, it is expected to be 102 and 90. The risk-free interest rate is 8% per annum with continuous compounding. What is the value of a three-month European put option with a strike price of $100? 96 5. How much is d? A. 1.105 B. 0.938 C. 1.020 D. 1.063 E. 1.097 6. How much is the payoff f_d? A. 3.000 B. 10.000 C. 5.000 D. 7.000 E. 4.000 7. How much is the risk neutral probability p? A. 0.570 B. 0.662 C. 0.810 D. 0.930 E. 1.105 8. How much is option price f? A. 3.317 B. 2.516 C. 2.020 D. 2.901 E. 2.281 1014 doum wall Ci A CEN

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Currency Wars Offense And Defense Through Systemic Thinking

Authors: Jeffrey Yi-Lin Forrest , Yirong Ying , Zaiwu Gong

1st Edition

3319677640,3319677659