Answered step by step

Verified Expert Solution

Question

1 Approved Answer

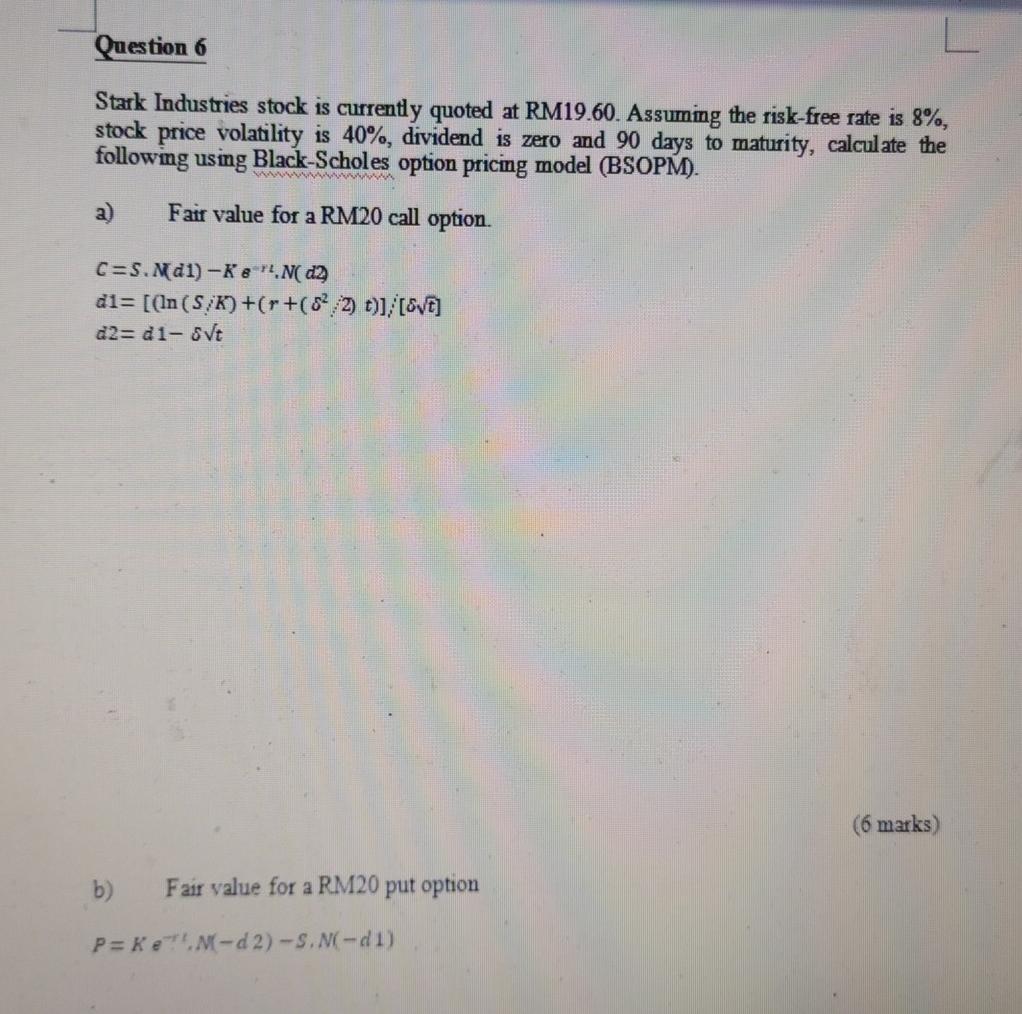

Question 6 Stark Industries stock is currently quoted at RM19.60. Assuming the risk-free rate is 8%, stock price volatility is 40%, dividend is zero and

Question 6 Stark Industries stock is currently quoted at RM19.60. Assuming the risk-free rate is 8%, stock price volatility is 40%, dividend is zero and 90 days to maturity, calculate the following using Black-Scholes option pricing model (BSOPM). a) Fair value for a RM20 call option. C=S.Md1)-K8-"N( d2 di= [(In(SK)+(r+(822) )],[Sv] d2=d1- SVt (6 marks) b) Fair value for a RM20 put option P=ke" -d 2)-S, NK -d1)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Water Finance

Authors: Michael Curley

1st Edition

1498734170, 978-1498734172