Answered step by step

Verified Expert Solution

Question

1 Approved Answer

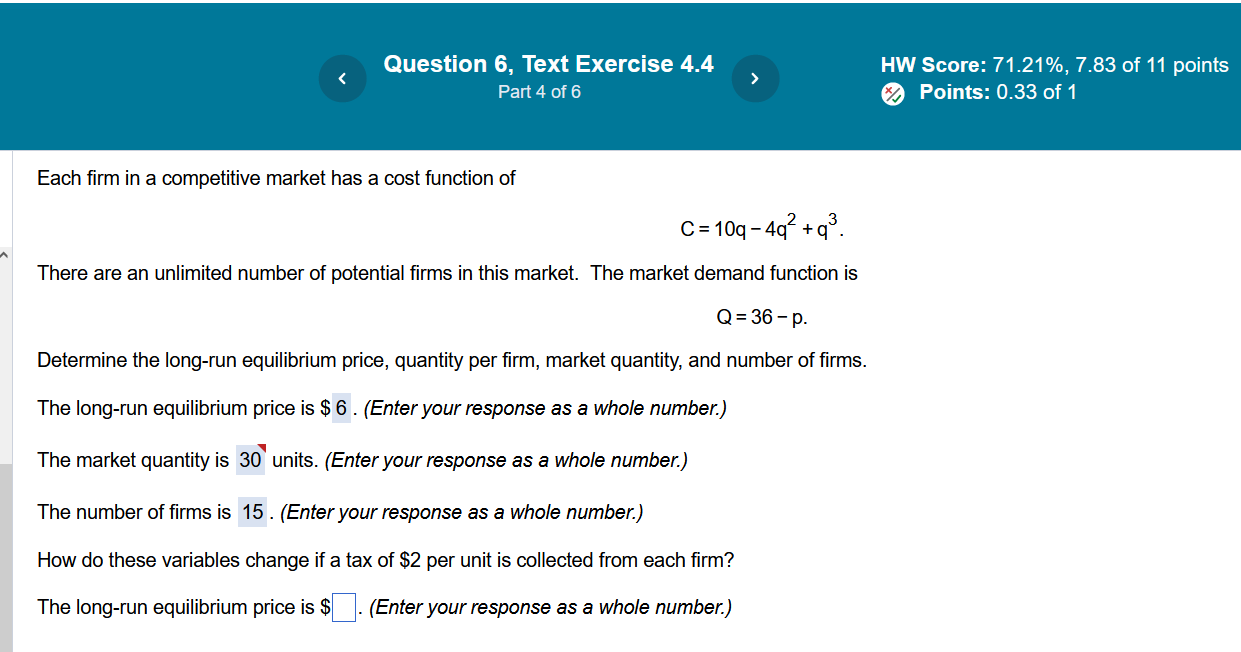

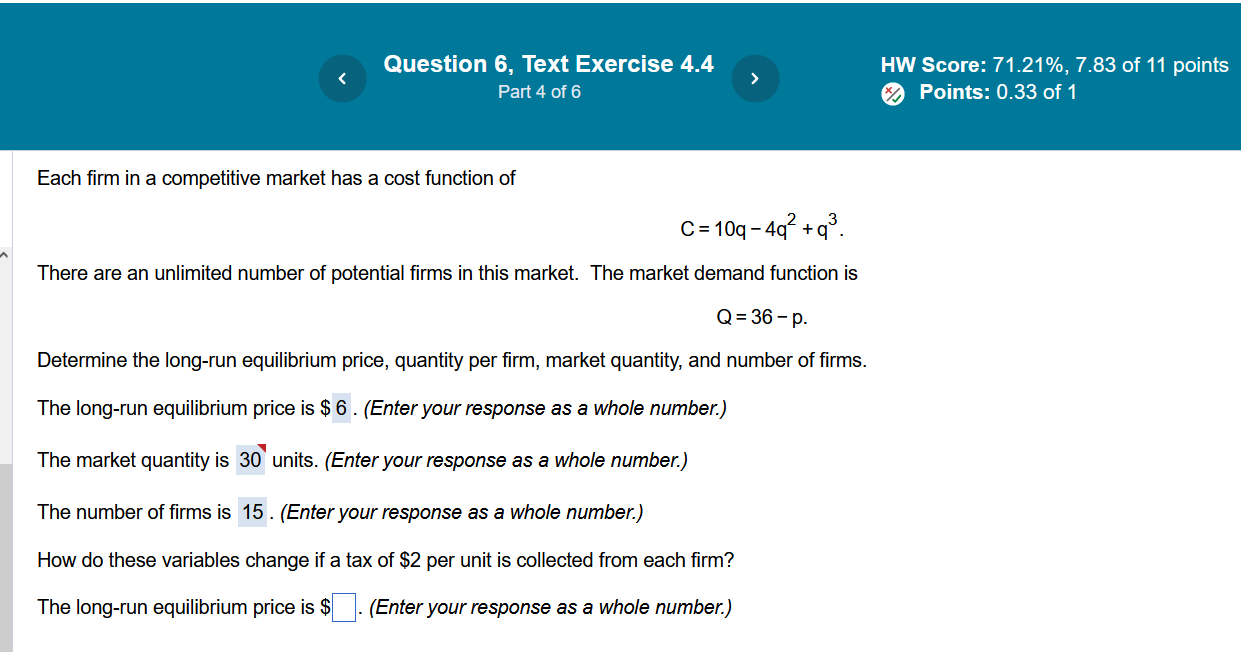

Question 6, Text Exercise 4.4 5 HW Score: 71.21%, 7.83 of 11 points Part 4 of 6 [/ ML E R Rl i Each firm

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding The Law

Authors: Donald L Carper, John A McKinsey, Bill W West

5th Edition

0324375123, 9780324375121