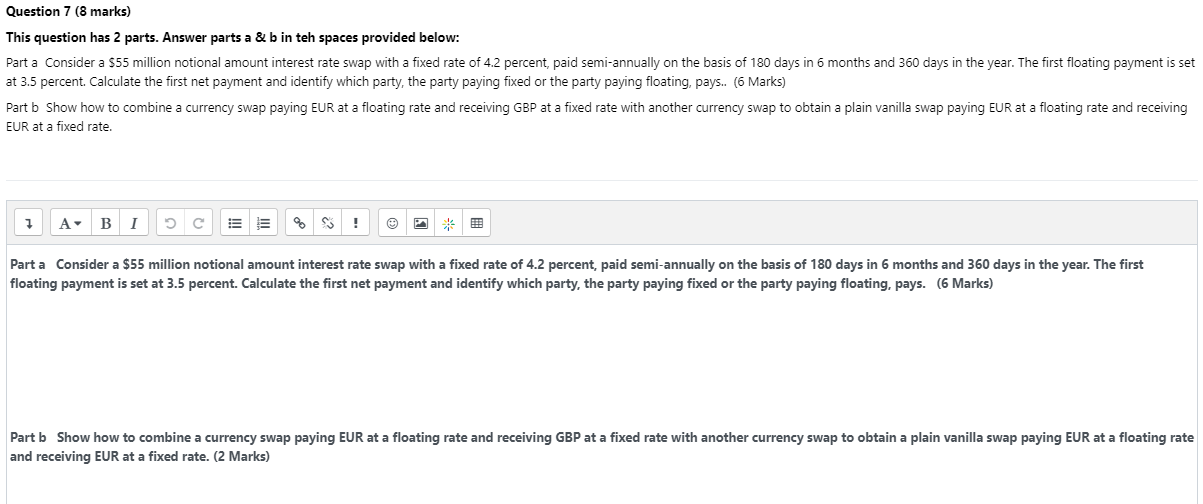

Question 7 (8 marks) This question has 2 parts. Answer parts a & b in teh spaces provided below: Part a Consider a $55 million notional amount interest rate swap with a fixed rate of 4.2 percent, paid semi-annually on the basis of 180 days in 6 months and 360 days in the year. The first floating payment is set at 3.5 percent. Calculate the first net payment and identify which party, the party paying fixed or the party paying floating, pays.. (6 Marks) Part b Show how to combine a currency swap paying EUR at a floating rate and receiving GBP at a fixed rate with another currency swap to obtain a plain vanilla swap paying EUR at a floating rate and receiving EUR at a fixed rate. 7 A B I 5 C % S ! Part a Consider a $55 million notional amount interest rate swap with a fixed rate of 4.2 percent, paid semi-annually on the basis of 180 days in 6 months and 360 days in the year. The first floating payment is set at 3.5 percent. Calculate the first net payment and identify which party, the party paying fixed or the party paying floating, pays. (6 Marks) Part b Show how to combine a currency swap paying EUR at a floating rate and receiving GBP at a fixed rate with another currency swap to obtain a plain vanilla swap paying EUR at a floating rate and receiving EUR at a fixed rate. (2 Marks) Question 7 (8 marks) This question has 2 parts. Answer parts a & b in teh spaces provided below: Part a Consider a $55 million notional amount interest rate swap with a fixed rate of 4.2 percent, paid semi-annually on the basis of 180 days in 6 months and 360 days in the year. The first floating payment is set at 3.5 percent. Calculate the first net payment and identify which party, the party paying fixed or the party paying floating, pays.. (6 Marks) Part b Show how to combine a currency swap paying EUR at a floating rate and receiving GBP at a fixed rate with another currency swap to obtain a plain vanilla swap paying EUR at a floating rate and receiving EUR at a fixed rate. 7 A B I 5 C % S ! Part a Consider a $55 million notional amount interest rate swap with a fixed rate of 4.2 percent, paid semi-annually on the basis of 180 days in 6 months and 360 days in the year. The first floating payment is set at 3.5 percent. Calculate the first net payment and identify which party, the party paying fixed or the party paying floating, pays. (6 Marks) Part b Show how to combine a currency swap paying EUR at a floating rate and receiving GBP at a fixed rate with another currency swap to obtain a plain vanilla swap paying EUR at a floating rate and receiving EUR at a fixed rate. (2 Marks)