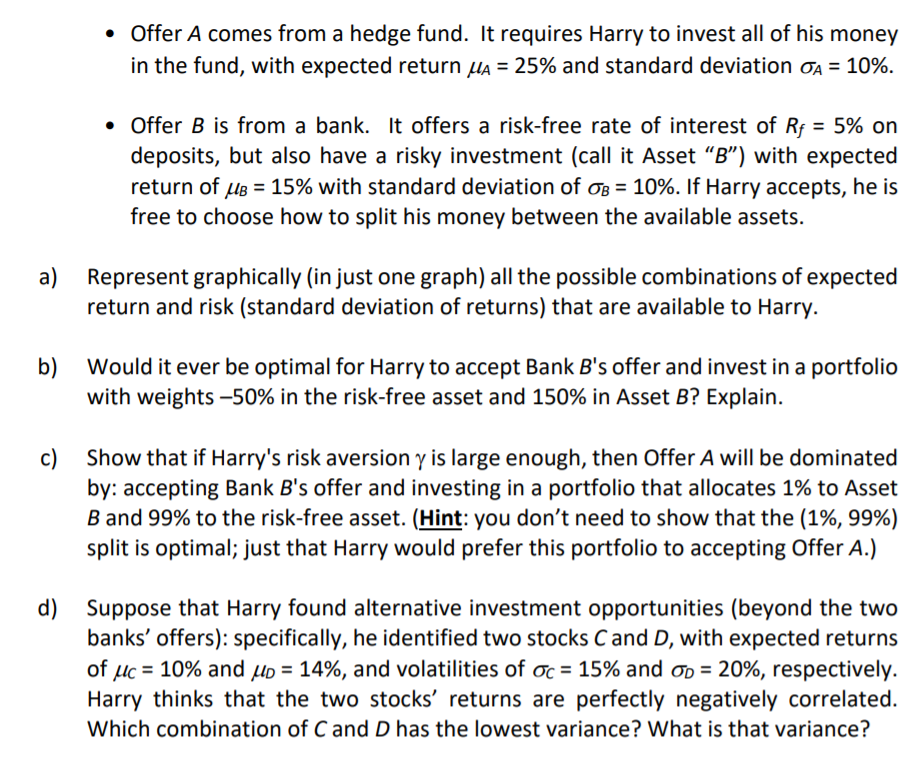

Question 9: Your uncle Harry has won $10million in the National Lottery and he wants to invest the money optimally. Harry's preferences are given by a mean-variance utility function: 1 Usu-Y, 2 where y is his coefficient of risk-aversion, and u and o are the expected return and volatility (standard deviation of return) of any investment opportunity he might consider. Harry has obtained offers from two different investment companies: Offer A comes from a hedge fund. It requires Harry to invest all of his money in the fund, with expected return up = 25% and standard deviation OA = 10%. Offer B is from a bank. It offers a risk-free rate of interest of Rf = 5% on deposits, but also have a risky investment (call it Asset B) with expected return of Ub = 15% with standard deviation of OB = 10%. If Harry accepts, he is free to choose how to split his money between the available assets. a) Represent graphically (in just one graph) all the possible combinations of expected return and risk (standard deviation of returns) that are available to Harry. b) Would it ever be optimal for Harry to accept Bank B's offer and invest in a portfolio with weights -50% in the risk-free asset and 150% in Asset B? Explain. c) Show that if Harry's risk aversion y is large enough, then Offer A will be dominated by: accepting Bank B's offer and investing in a portfolio that allocates 1% to Asset B and 99% to the risk-free asset. (Hint: you don't need to show that the (1%, 99%) split is optimal; just that Harry would prefer this portfolio to accepting Offer A.) d) Suppose that Harry found alternative investment opportunities (beyond the two banks' offers): specifically, he identified two stocks C and D, with expected returns of uc = 10% and Up = 14%, and volatilities of oc = 15% and op = 20%, respectively. Harry thinks that the two stocks' returns are perfectly negatively correlated. Which combination of Cand D has the lowest variance? What is that variance? Question 9: Your uncle Harry has won $10million in the National Lottery and he wants to invest the money optimally. Harry's preferences are given by a mean-variance utility function: 1 Usu-Y, 2 where y is his coefficient of risk-aversion, and u and o are the expected return and volatility (standard deviation of return) of any investment opportunity he might consider. Harry has obtained offers from two different investment companies: Offer A comes from a hedge fund. It requires Harry to invest all of his money in the fund, with expected return up = 25% and standard deviation OA = 10%. Offer B is from a bank. It offers a risk-free rate of interest of Rf = 5% on deposits, but also have a risky investment (call it Asset B) with expected return of Ub = 15% with standard deviation of OB = 10%. If Harry accepts, he is free to choose how to split his money between the available assets. a) Represent graphically (in just one graph) all the possible combinations of expected return and risk (standard deviation of returns) that are available to Harry. b) Would it ever be optimal for Harry to accept Bank B's offer and invest in a portfolio with weights -50% in the risk-free asset and 150% in Asset B? Explain. c) Show that if Harry's risk aversion y is large enough, then Offer A will be dominated by: accepting Bank B's offer and investing in a portfolio that allocates 1% to Asset B and 99% to the risk-free asset. (Hint: you don't need to show that the (1%, 99%) split is optimal; just that Harry would prefer this portfolio to accepting Offer A.) d) Suppose that Harry found alternative investment opportunities (beyond the two banks' offers): specifically, he identified two stocks C and D, with expected returns of uc = 10% and Up = 14%, and volatilities of oc = 15% and op = 20%, respectively. Harry thinks that the two stocks' returns are perfectly negatively correlated. Which combination of Cand D has the lowest variance? What is that variance