Answered step by step

Verified Expert Solution

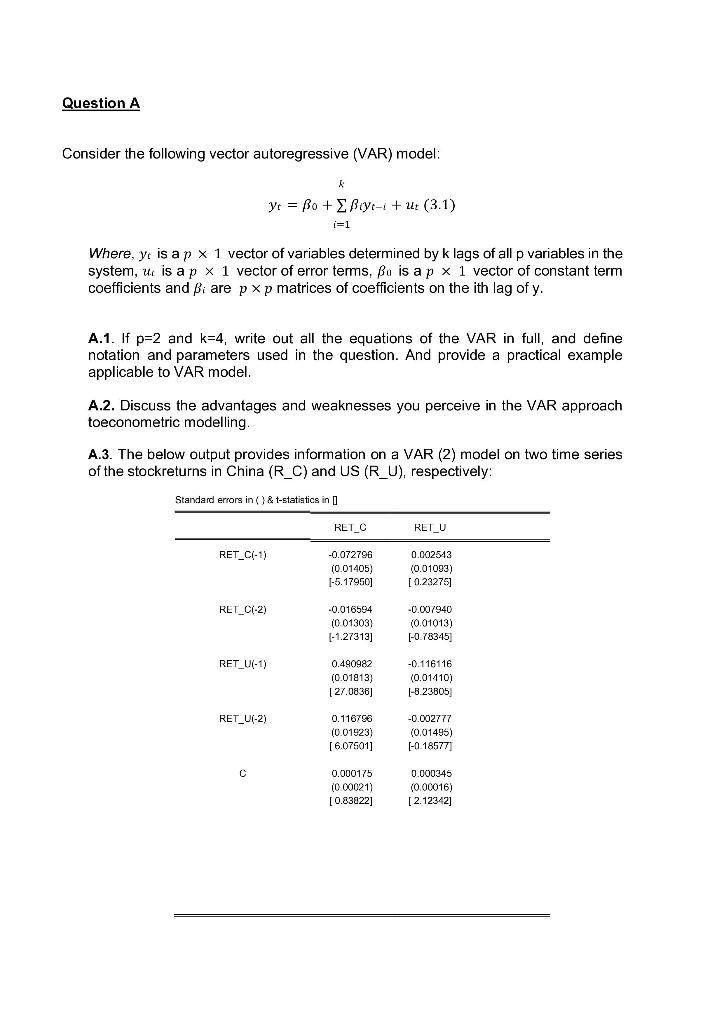

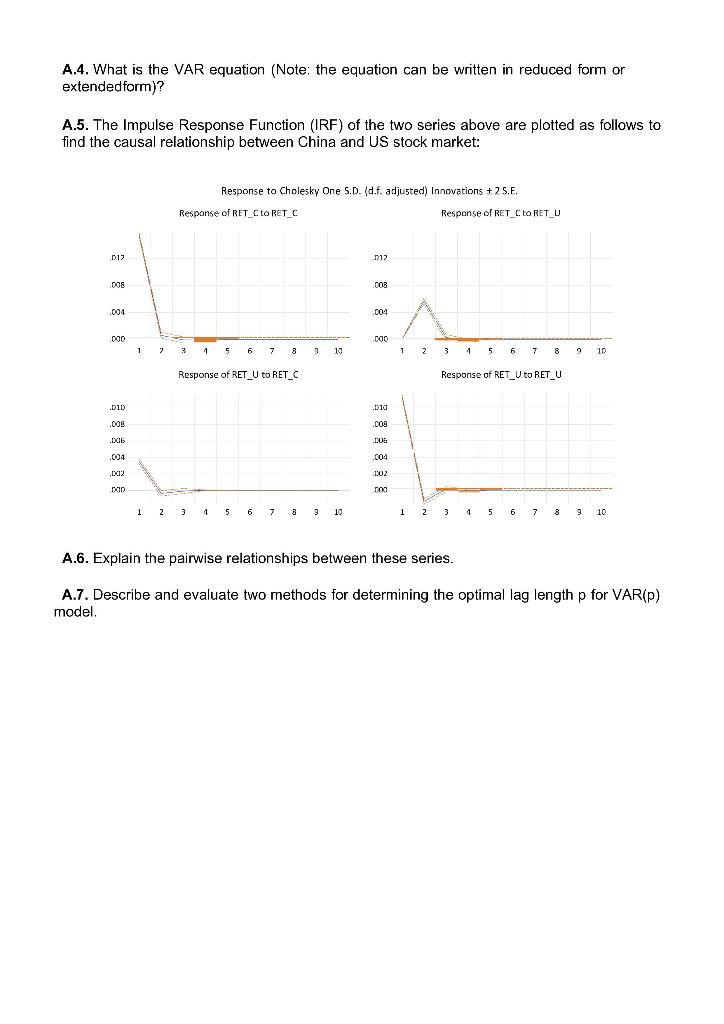

Question

1 Approved Answer

Question B 1. The table below presents the temperature, in Celsius degrees, at 9pm over the last 10 days in Aberdeen: Day 1 2 3

Question B

1. The table below presents the temperature, in Celsius degrees, at 9pm over the last 10 days in Aberdeen:

| Day | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Temperature | 1.5 | 2.3 | 3.7 | 3.0 | 1.4 | -1.3 | -2.4 | -3.7 | -0.5 | 1.3 |

-

- a. Calculate a 3-day moving average for each day. Indicate the value of the forecast for the temperature on day 11 at 9pm.

-

- b. Apply exponential smoothing with smoothing constant of 0.8. Indicate the value of the forecast for the temperature at 9pm on day 11.

-

- c. Briefly explain which of the two forecasts would you prefer.

- d. Box and Jenkins (1970) where the first to develop a systematic methodology which identifies and fits a combination of two processe

- e. Indicate which model Box and Jenkins (1970) identify. Briefly discuss the different components.

-

- d. The estimation model by Box and Jenkins (1970) includes an important assumption regarding the error term of the series. Clearly Indicate which assumption should be meet for the model to be accurate. Refer what should be done in a scenario that the assumption is not valid.

-

- e. Briefly indicate the reason why forecasters usually prefer the Box and Jenkins (1970) combination model.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Report Of The Follow Up International Conference On Financing For Development To Review The Implementation Of The Monterrey Consensus Doha Qatar 29 November 2 December 2008

Authors: United Nations

1st Edition

9211045940,9210558685