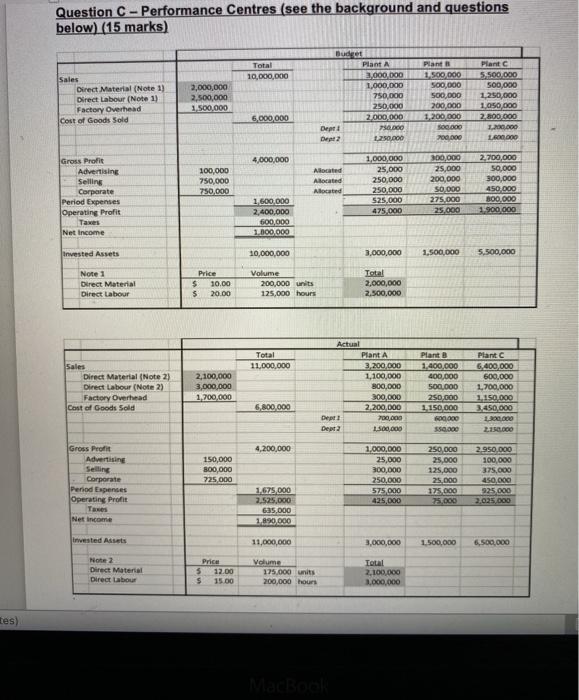

Question C - Performance Centres (see the background and questions below) (15 marks) Total 10,000,000 [Sales Direct Material (Note 1) Direct Labour (Note 1) Factory Overhead Cost of Goods Sold 2,000,000 2,500,000 1.500,000 Budet Plant 3.000.000 1.000.000 750,000 250,000 2,000,000 Depe 750.000 Det 250.000 Plant 1.500.000 500,000 500,000 200.000 1.200.000 SORDO 700.000 Plant 5.500.000 500,000 1.250,000 1.050.000 2.800.000 1.200.000 LRO.000 5,000,000 4,000,000 100,000 750,000 750,000 Alocated Alocated Alocated Gross Profit Advertising Selling Corporate Period Expenses Operating Profit Taxes Net Income 1,000,000 25,000 250,000 250.000 525.000 475,000 300,000 2,700,000 25,000 50,000 200,000 300,000 50.000 450.000 275.000 B00,000 25.000 1.900 000 1.600.000 2,400,000 600,000 1,000,000 Invested Assets 10,000,000 3,000,000 1,500,000 5,500,000 Note 1 Direct Material Direct Labour Price $ 10.00 $ 20.00 Volume 200,000 units 125,000 hours Total 2,000,000 2,500,000 Total 11,000,000 Sales Direct Material (Note 2) Direct Labour (Note 2) Factory Overhead Cost of Goods Sold 2,100,000 3,000,000 1.700.000 Actual Plant A 3,200.000 1,100,000 300,000 300.000 2,200,000 Dept 700,000 Dept2 1.500.000 Plant B 1.400.000 400.000 500,000 250.000 1 150,000 Plant 6,400,000 600,000 1.700,000 1.150.000 3,450,000 100.000 6.800.000 2000 4,200,000 Gross Profit Advertising Selling Corporate Period Expenses Operating Profit 150,000 800,000 725,000 1,000,000 25,000 300,000 250,000 575 000 425,000 250 000 25,000 125.000 25.000 175.000 2.950.000 100,000 375,000 450,000 925.000 2,025.000 1.675,000 2.525,000 635,000 1.890 000 Net Income Invested Assets 11,000,000 3,000,000 1.500.000 6,500,000 Note 2 Direct Material Direct Labour Price 5 12.00 $ 15.00 Volume 175,000 units 200,000 hours Total 2.100.000 3,000,000 tes) The first table is the budget, and the second table is the actual results for the year. Round amounts to dollars and percentages to one decimal. Note that there are several cost centres, profit centres and investment centres in the budget and actuals results. The Total" column is the entire company managed by a chief executive officer while Plants, Departments (e.g., Dept 1 and 2) and specific period costs are managed by other managers given their assigned responsibilities. Within the Plants, there are two departments per Plant (e.g., Plant A has departments 1 and 2 and Plant B also has departments 1 and 2, separately managed). Period costs are allocated based on an activity-based accounting driver and are not separate cost centres within the Plants. The company manages with four investments centres, four profit centres and nine costs centres. The company has set goals for return on sales of 10%, return on investment of 10% and positive residual income. Questions 1. Briefly describe why responsibility centres are used and a major requirement that enhances usefulness and motivation to managers. 2. For the appropriate responsibility centres based on the actual results, calculate: a. Return on Sales b. Return on Investment c. Residual Income 3. Which of the responsibility centres in 2 are not performing to expectations? 4. Calculate the budget to actual performance for the nine cost centres. These include plant departments and total advertising, selling and corporate costs. 5. Which cost centres in 4 are not performing to expectations? Secondly, if considering sales performance would you change your opinion on any cost centres? 6. Overall, are there responsibility centres you would advise the CFO to monitor closely and have discussions. 7. What is one human resources issue you would investigate? Question C - Performance Centres (see the background and questions below) (15 marks) Total 10,000,000 [Sales Direct Material (Note 1) Direct Labour (Note 1) Factory Overhead Cost of Goods Sold 2,000,000 2,500,000 1.500,000 Budet Plant 3.000.000 1.000.000 750,000 250,000 2,000,000 Depe 750.000 Det 250.000 Plant 1.500.000 500,000 500,000 200.000 1.200.000 SORDO 700.000 Plant 5.500.000 500,000 1.250,000 1.050.000 2.800.000 1.200.000 LRO.000 5,000,000 4,000,000 100,000 750,000 750,000 Alocated Alocated Alocated Gross Profit Advertising Selling Corporate Period Expenses Operating Profit Taxes Net Income 1,000,000 25,000 250,000 250.000 525.000 475,000 300,000 2,700,000 25,000 50,000 200,000 300,000 50.000 450.000 275.000 B00,000 25.000 1.900 000 1.600.000 2,400,000 600,000 1,000,000 Invested Assets 10,000,000 3,000,000 1,500,000 5,500,000 Note 1 Direct Material Direct Labour Price $ 10.00 $ 20.00 Volume 200,000 units 125,000 hours Total 2,000,000 2,500,000 Total 11,000,000 Sales Direct Material (Note 2) Direct Labour (Note 2) Factory Overhead Cost of Goods Sold 2,100,000 3,000,000 1.700.000 Actual Plant A 3,200.000 1,100,000 300,000 300.000 2,200,000 Dept 700,000 Dept2 1.500.000 Plant B 1.400.000 400.000 500,000 250.000 1 150,000 Plant 6,400,000 600,000 1.700,000 1.150.000 3,450,000 100.000 6.800.000 2000 4,200,000 Gross Profit Advertising Selling Corporate Period Expenses Operating Profit 150,000 800,000 725,000 1,000,000 25,000 300,000 250,000 575 000 425,000 250 000 25,000 125.000 25.000 175.000 2.950.000 100,000 375,000 450,000 925.000 2,025.000 1.675,000 2.525,000 635,000 1.890 000 Net Income Invested Assets 11,000,000 3,000,000 1.500.000 6,500,000 Note 2 Direct Material Direct Labour Price 5 12.00 $ 15.00 Volume 175,000 units 200,000 hours Total 2.100.000 3,000,000 tes) The first table is the budget, and the second table is the actual results for the year. Round amounts to dollars and percentages to one decimal. Note that there are several cost centres, profit centres and investment centres in the budget and actuals results. The Total" column is the entire company managed by a chief executive officer while Plants, Departments (e.g., Dept 1 and 2) and specific period costs are managed by other managers given their assigned responsibilities. Within the Plants, there are two departments per Plant (e.g., Plant A has departments 1 and 2 and Plant B also has departments 1 and 2, separately managed). Period costs are allocated based on an activity-based accounting driver and are not separate cost centres within the Plants. The company manages with four investments centres, four profit centres and nine costs centres. The company has set goals for return on sales of 10%, return on investment of 10% and positive residual income. Questions 1. Briefly describe why responsibility centres are used and a major requirement that enhances usefulness and motivation to managers. 2. For the appropriate responsibility centres based on the actual results, calculate: a. Return on Sales b. Return on Investment c. Residual Income 3. Which of the responsibility centres in 2 are not performing to expectations? 4. Calculate the budget to actual performance for the nine cost centres. These include plant departments and total advertising, selling and corporate costs. 5. Which cost centres in 4 are not performing to expectations? Secondly, if considering sales performance would you change your opinion on any cost centres? 6. Overall, are there responsibility centres you would advise the CFO to monitor closely and have discussions. 7. What is one human resources issue you would investigate