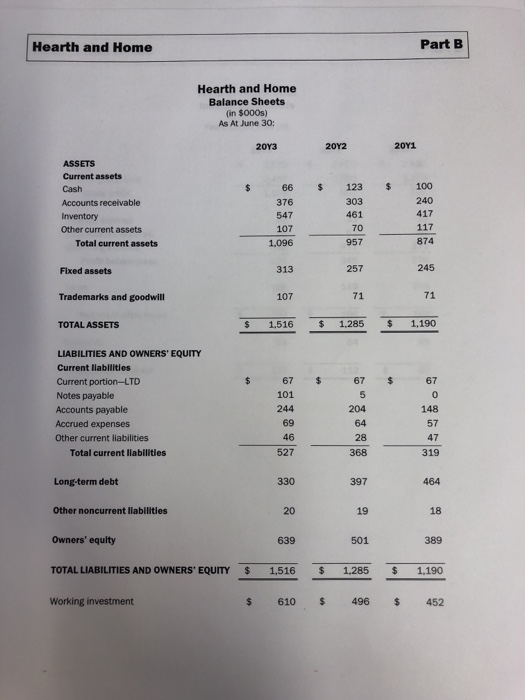

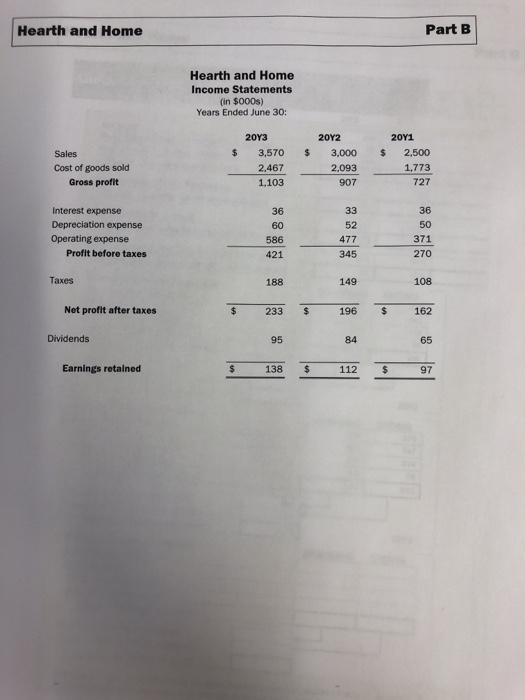

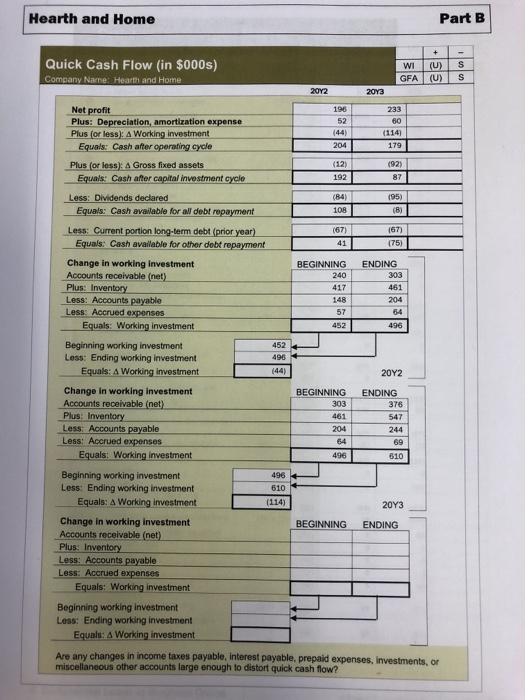

Question() Directions the case link displayed above and use the information provided in earth and Home, Part to answer this question Assume that sales for earth and Home are projected to grow by 6 percent in accounts receivabite balance in the sto pour caution) 4. If the accounts receivable days on hand in 2014 are assumed to be 40 days, what would be 4 3.co 1000 Hearth and Home Part B Hearth and Home Balance Sheets in $000s) As At June 30: 2013 2012 2011 123 100 ASSETS Current assets Cash Accounts receivable Inventory Other current assets Total current assets 303 66 376 547 107 1.096 461 417 117 70 957 874 Fixed assets 313 257 245 Trademarks and goodwill 107 71 71 TOTAL ASSETS $ 1.516 1.286 $ 1,190 67 LIABILITIES AND OWNERS' EQUITY Current liabilities Current portion-LTD Notes payable Accounts payable Accrued expenses Other current liabilities Total current liabilities Long-term debt Other noncurrent liabilities Owners' equity 501 389 TOTAL LIABILITIES AND OWNERS' EQUITY $ 1.516 $ 1.285 $ 1.190 Working investment $ 610 $ 496 $ 452 Hearth and Home Part B Hearth and Home Income Statements (in $000s) Years Ended June 30: $ $ 2013 3,570 2,467 1.103 2011 2,500 2012 3,000 2.093 Sales Cost of goods sold Gross profit $ 1.173 Interest expense Depreciation expense Operating expense Profit before taxes 586 421 Taxes Net profit after taxes Dividends Earnings retained $ 138 $ 112 5 97 Hearth and Home Part Quick Cash Flow (in $000s) WI GFA (U) (U) S S COCINE and Home 2012 2013 Net profit Plus: Depreciation, amortization expense Plus (or less): A Working investment Equals: Cash after operating cycle 44 204 179 (92) (12) 192 Plus (or less): A Gross fixed assets Equals: Cash after capital investment cycle Less: Dividends declared Equals: Cash available for all debt repayment (84) 108 (95) (8) 1671 1671 (75) ENDING 303 Less: Current portion long-term debt (prior year) Equals: Cash available for other debt repayment Change in working investment Accounts receivable (net) Plus: Inventory Less: Accounts payable Less: Accrued expenses Equals: Working investment BEGINNING 240 417 148 57 452 496 452 Beginning working investment Less: Ending working investment Equals: A Working investment 20Y2 ENDING 376 Change in working investment Accounts receivable (net) Plus: Inventory Less: Accounts payable Less: Accrued expenses Equals: Working investment BEGINNING 303 461 204 244 496 610 496 610 (114) 2013 ENDING BEGINNING Beginning working investment Less: Ending working investment Equals: A Working investment Change in working investment Accounts receivable (net) Plus: Inventory Less: Accounts payable Less: Accrued expenses Equals: Working investment Beginning working investment Less: Ending working investment Equals: A Working investment Are any changes in income taxes payable, interest payable, prepaid expenses, investments, or miscellaneous other accounts large enough to distort quick cash flow