Answered step by step

Verified Expert Solution

Question

1 Approved Answer

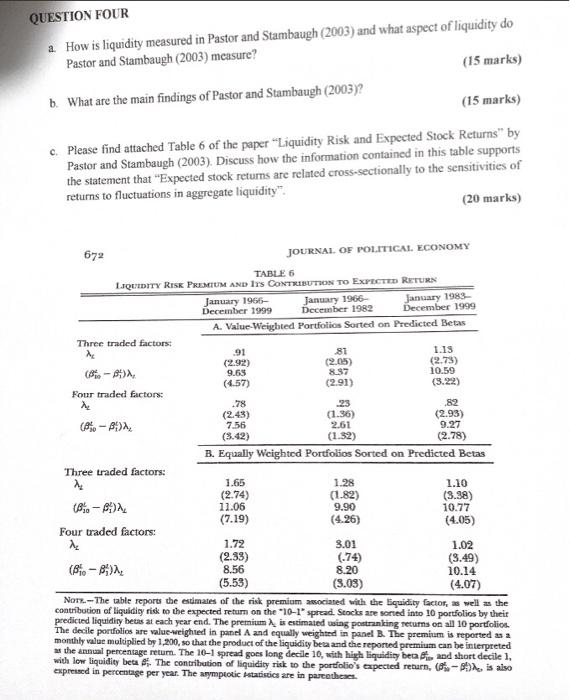

QUESTION FOUR How is liquidity measured in Pastor and Stambaugh (2003) and what aspect of liquidity do Pastor and Stambaugh (2003) measure? (15 marks) b.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Beyond Bitcoin Economics Of Digital Currencies And Blockchain Technologies

Authors: Hanna Halaburda, Miklos Sarvary, Guillaume Haeringer

2nd Edition

3030889300,3030889319