Answered step by step

Verified Expert Solution

Question

1 Approved Answer

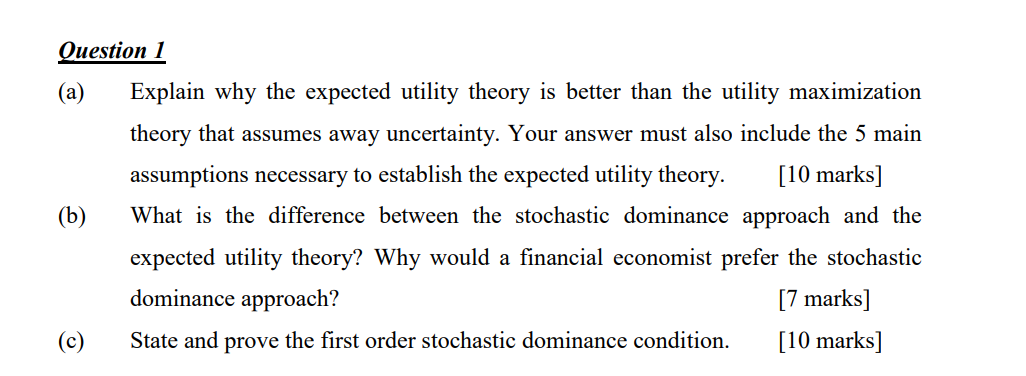

Question I (a) Explain why the expected utility theory is better than the utility maximization theory that assumes away uncertainty. Your answer must also include

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Puzzle Of Latin American Economic Development

Authors: Patrice Franko

2nd Edition

0742524663, 9780742524668