Question is complete.

From the information below:

- List all double entries to record the adjustments to the financial statements

- Prepare the statement of comprehensive income for ACRYLO for the year ended 31 March 2020

- Prepare the statement of changes in equity

- Prepare the statement of financial position for ACRYLO as at 31 March 2020

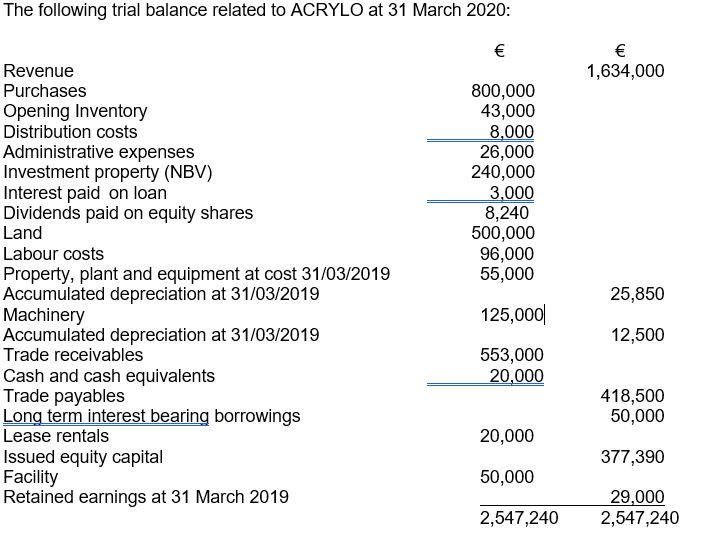

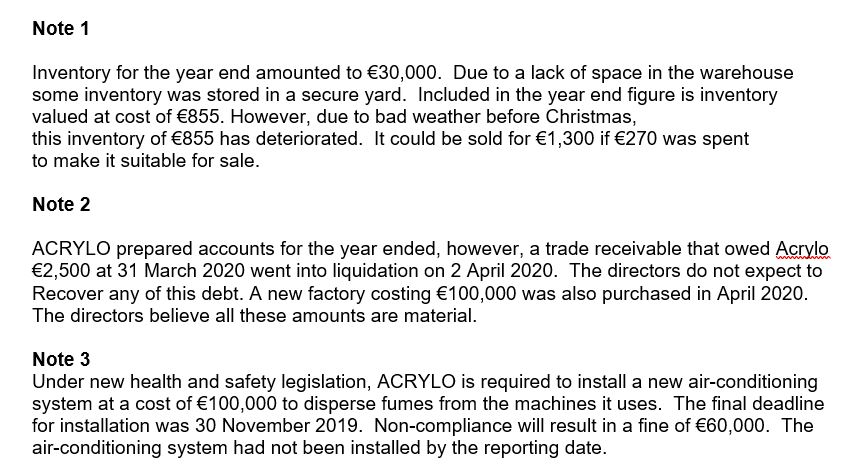

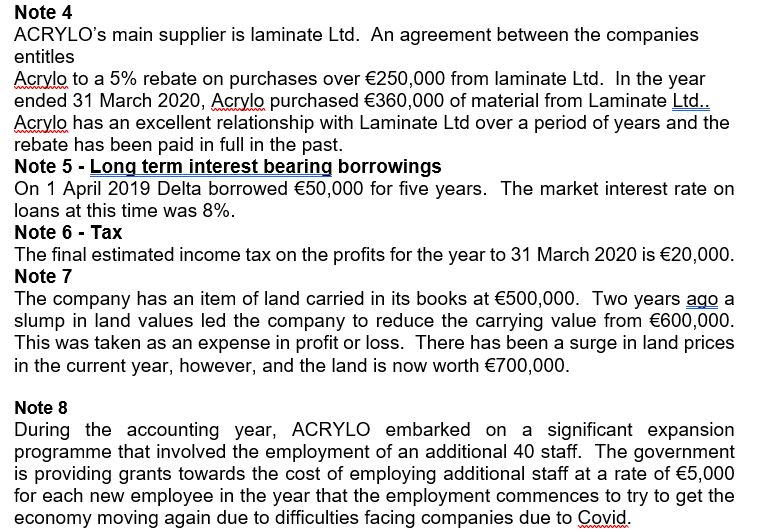

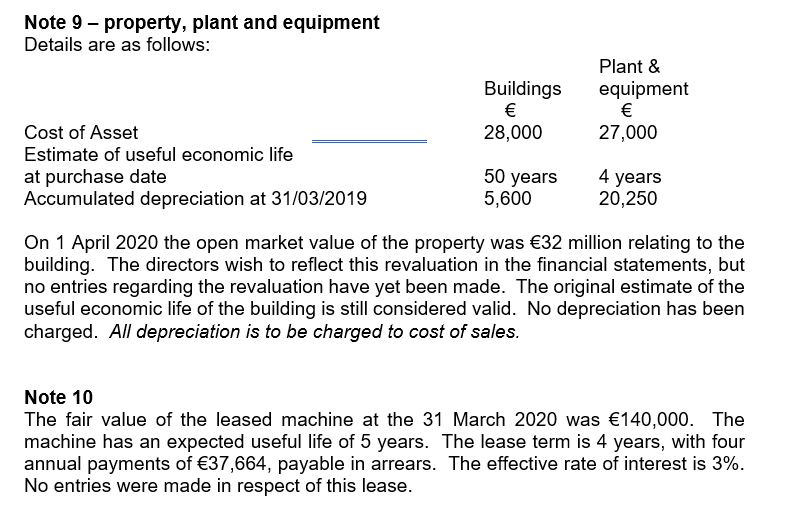

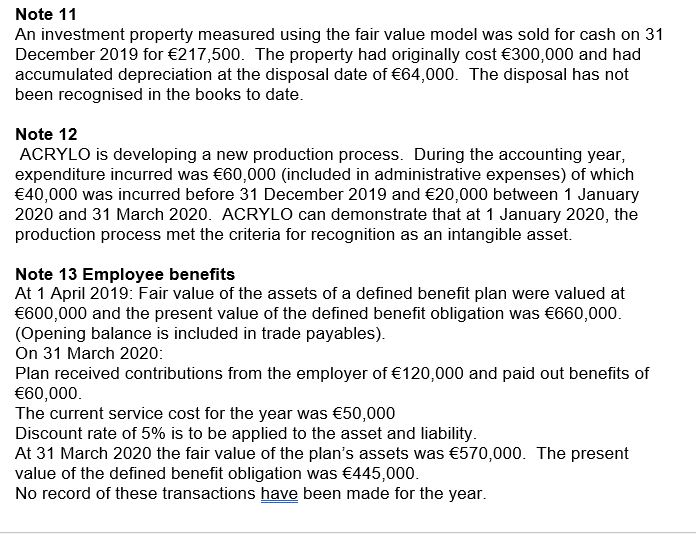

The following trial balance related to ACRYLO at 31 March 2020: 1,634,000 800,000 43,000 8,000 26,000 240,000 3,000 8,240 500,000 96,000 55,000 Revenue Purchases Opening Inventory Distribution costs Administrative expenses Investment property (NBV) Interest paid on loan Dividends paid on equity shares Land Labour costs Property, plant and equipment at cost 31/03/2019 Accumulated depreciation at 31/03/2019 Machinery Accumulated depreciation at 31/03/2019 Trade receivables Cash and cash equivalents Trade payables Long term interest bearing borrowings Lease rentals Issued equity capital Facility Retained earnings at 31 March 2019 25,850 125,000 12,500 553,000 20,000 418,500 50,000 20,000 377,390 50,000 29.000 2,547,240 2,547,240 Note 1 Inventory for the year end amounted to 30,000. Due to a lack of space in the warehouse some inventory was stored in a secure yard. Included in the year end figure is inventory valued at cost of 855. However, due to bad weather before Christmas, this inventory of 855 has deteriorated. It could be sold for 1,300 if 270 was spent to make it suitable for sale. Note 2 ACRYLO prepared accounts for the year ended, however, a trade receivable that owed Acrylo 2,500 at 31 March 2020 went into liquidation on 2 April 2020. The directors do not expect to Recover any of this debt. A new factory costing 100,000 was also purchased in April 2020. The directors believe all these amounts are material. Note 3 Under new health and safety legislation, ACRYLO is required to install a new air-conditioning system at a cost of 100,000 to disperse fumes from the machines it uses. The final deadline for installation was 30 November 2019. Non-compliance will result in a fine of 60,000. The air-conditioning system had not been installed by the reporting date. Note 4 ACRYLO's main supplier is laminate Ltd. An agreement between the companies entitles Acrylo to a 5% rebate on purchases over 250,000 from laminate Ltd. In the year ended 31 March 2020, Acrylo purchased 360,000 of material from Laminate Ltd.. Acrylo has an excellent relationship with Laminate Ltd over a period of years and the rebate has been paid in full in the past. Note 5 - Long term interest bearing borrowings On 1 April 2019 Delta borrowed 50,000 for five years. The market interest rate on loans at this time was 8%. Note 6 - Tax The final estimated income tax on the profits for the year to 31 March 2020 is 20,000. Note 7 The company has an item of land carried in its books at 500,000. Two years ago a slump in land values led the company to reduce the carrying value from 600,000. This was taken as an expense in profit or loss. There has been a surge in land prices in the current year, however, and the land is now worth 700,000. Note 8 During the accounting year, ACRYLO embarked on a significant expansion programme that involved the employment of an additional 40 staff. The government is providing grants towards the cost of employing additional staff at a rate of 5,000 for each new employee in the year that the employment commences to try to get the economy moving again due to difficulties facing companies due to Covid. Note 9 - property, plant and equipment Details are as follows: Buildings 28,000 Plant & equipment 27,000 Cost of Asset Estimate of useful economic life at purchase date Accumulated depreciation at 31/03/2019 50 years 5,600 4 years 20,250 On 1 April 2020 the open market value of the property was 32 million relating to the building. The directors wish to reflect this revaluation in the financial statements, but no entries regarding the revaluation have yet been made. The original estimate of the useful economic life of the building is still considered valid. No depreciation has been charged. All depreciation is to be charged to cost of sales. Note 10 The fair value of the leased machine at the 31 March 2020 was 140,000. The machine has an expected useful life of 5 years. The lease term is 4 years, with four annual payments of 37,664, payable in arrears. The effective rate of interest is 3%. No entries were made in respect of this lease. Note 11 An investment property measured using the fair value model was sold for cash on 31 December 2019 for 217,500. The property had originally cost 300,000 and had accumulated depreciation at the disposal date of 64,000. The disposal has not been recognised in the books to date. Note 12 ACRYLO is developing a new production process. During the accounting year, expenditure incurred was 60,000 (included in administrative expenses) of which 40,000 was incurred before 31 December 2019 and 20,000 between 1 January 2020 and 31 March 2020. ACRYLO can demonstrate that at 1 January 2020, the production process met the criteria for recognition as an intangible asset. Note 13 Employee benefits At 1 April 2019: Fair value of the assets of a defined benefit plan were valued at 600,000 and the present value of the defined benefit obligation was 660,000. (Opening balance is included in trade payables). On 31 March 2020: Plan received contributions from the employer of 120,000 and paid out benefits of 60,000. The current service cost for the year was 50,000 Discount rate of 5% is to be applied to the asset and liability. At 31 March 2020 the fair value of the plan's assets was 570,000. The present value of the defined benefit obligation was 445,000. No record of these transactions have been made for the year. The following trial balance related to ACRYLO at 31 March 2020: 1,634,000 800,000 43,000 8,000 26,000 240,000 3,000 8,240 500,000 96,000 55,000 Revenue Purchases Opening Inventory Distribution costs Administrative expenses Investment property (NBV) Interest paid on loan Dividends paid on equity shares Land Labour costs Property, plant and equipment at cost 31/03/2019 Accumulated depreciation at 31/03/2019 Machinery Accumulated depreciation at 31/03/2019 Trade receivables Cash and cash equivalents Trade payables Long term interest bearing borrowings Lease rentals Issued equity capital Facility Retained earnings at 31 March 2019 25,850 125,000 12,500 553,000 20,000 418,500 50,000 20,000 377,390 50,000 29.000 2,547,240 2,547,240 Note 1 Inventory for the year end amounted to 30,000. Due to a lack of space in the warehouse some inventory was stored in a secure yard. Included in the year end figure is inventory valued at cost of 855. However, due to bad weather before Christmas, this inventory of 855 has deteriorated. It could be sold for 1,300 if 270 was spent to make it suitable for sale. Note 2 ACRYLO prepared accounts for the year ended, however, a trade receivable that owed Acrylo 2,500 at 31 March 2020 went into liquidation on 2 April 2020. The directors do not expect to Recover any of this debt. A new factory costing 100,000 was also purchased in April 2020. The directors believe all these amounts are material. Note 3 Under new health and safety legislation, ACRYLO is required to install a new air-conditioning system at a cost of 100,000 to disperse fumes from the machines it uses. The final deadline for installation was 30 November 2019. Non-compliance will result in a fine of 60,000. The air-conditioning system had not been installed by the reporting date. Note 4 ACRYLO's main supplier is laminate Ltd. An agreement between the companies entitles Acrylo to a 5% rebate on purchases over 250,000 from laminate Ltd. In the year ended 31 March 2020, Acrylo purchased 360,000 of material from Laminate Ltd.. Acrylo has an excellent relationship with Laminate Ltd over a period of years and the rebate has been paid in full in the past. Note 5 - Long term interest bearing borrowings On 1 April 2019 Delta borrowed 50,000 for five years. The market interest rate on loans at this time was 8%. Note 6 - Tax The final estimated income tax on the profits for the year to 31 March 2020 is 20,000. Note 7 The company has an item of land carried in its books at 500,000. Two years ago a slump in land values led the company to reduce the carrying value from 600,000. This was taken as an expense in profit or loss. There has been a surge in land prices in the current year, however, and the land is now worth 700,000. Note 8 During the accounting year, ACRYLO embarked on a significant expansion programme that involved the employment of an additional 40 staff. The government is providing grants towards the cost of employing additional staff at a rate of 5,000 for each new employee in the year that the employment commences to try to get the economy moving again due to difficulties facing companies due to Covid. Note 9 - property, plant and equipment Details are as follows: Buildings 28,000 Plant & equipment 27,000 Cost of Asset Estimate of useful economic life at purchase date Accumulated depreciation at 31/03/2019 50 years 5,600 4 years 20,250 On 1 April 2020 the open market value of the property was 32 million relating to the building. The directors wish to reflect this revaluation in the financial statements, but no entries regarding the revaluation have yet been made. The original estimate of the useful economic life of the building is still considered valid. No depreciation has been charged. All depreciation is to be charged to cost of sales. Note 10 The fair value of the leased machine at the 31 March 2020 was 140,000. The machine has an expected useful life of 5 years. The lease term is 4 years, with four annual payments of 37,664, payable in arrears. The effective rate of interest is 3%. No entries were made in respect of this lease. Note 11 An investment property measured using the fair value model was sold for cash on 31 December 2019 for 217,500. The property had originally cost 300,000 and had accumulated depreciation at the disposal date of 64,000. The disposal has not been recognised in the books to date. Note 12 ACRYLO is developing a new production process. During the accounting year, expenditure incurred was 60,000 (included in administrative expenses) of which 40,000 was incurred before 31 December 2019 and 20,000 between 1 January 2020 and 31 March 2020. ACRYLO can demonstrate that at 1 January 2020, the production process met the criteria for recognition as an intangible asset. Note 13 Employee benefits At 1 April 2019: Fair value of the assets of a defined benefit plan were valued at 600,000 and the present value of the defined benefit obligation was 660,000. (Opening balance is included in trade payables). On 31 March 2020: Plan received contributions from the employer of 120,000 and paid out benefits of 60,000. The current service cost for the year was 50,000 Discount rate of 5% is to be applied to the asset and liability. At 31 March 2020 the fair value of the plan's assets was 570,000. The present value of the defined benefit obligation was 445,000. No record of these transactions have been made for the year