Question

Question: Michelle started working for Quick Solutions located in Regina, Saskatchewan, on June 1, 1982. She joined the company's defined contribution registered pension plan on

Question:

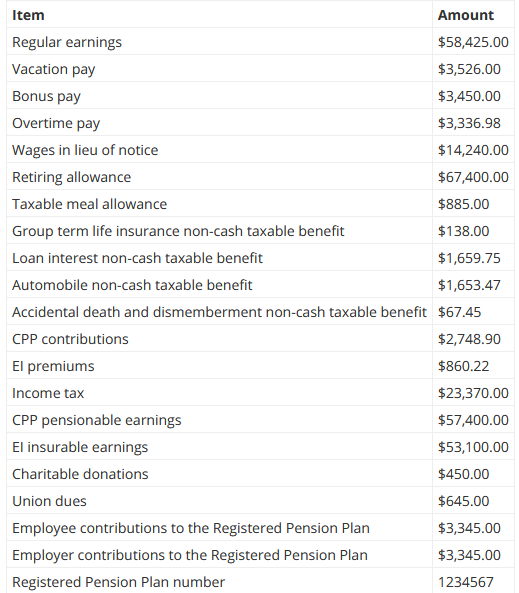

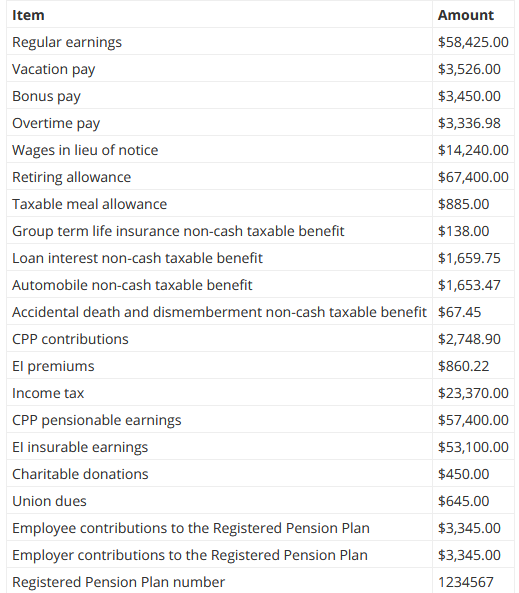

Michelle started working for Quick Solutions located in Regina, Saskatchewan, on June 1, 1982. She joined the company's defined contribution registered pension plan on January 1, 1986 and was fully vested in this plan when her employment was terminated in October, 2019. As part of the termination package, Michelle received a retiring allowance of $67,400.00. Michelle had asked her employer to transfer the entire eligible amount to a RRSP and took the non-eligible amount in cash.Calculate the eligible and non-eligible portions of Michelle's retiring allowance as well as the income tax withheld on the amount received in cash. Include these amounts when completing Michelle's T4 slip. The $23,370.00 income tax shown on the year-end payroll register does not include the tax amount withheld on the retiring allowance.

Complete Michelle's T4 using the information from the year-end payroll register.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Accounting

Authors: Fred Phillips, Robert Libby, Patricia Libby

6th edition

1259864235, 1259864230, 1260159547, 126015954X, 978-1259864230