question number 3 is what I need answered. Thanks!

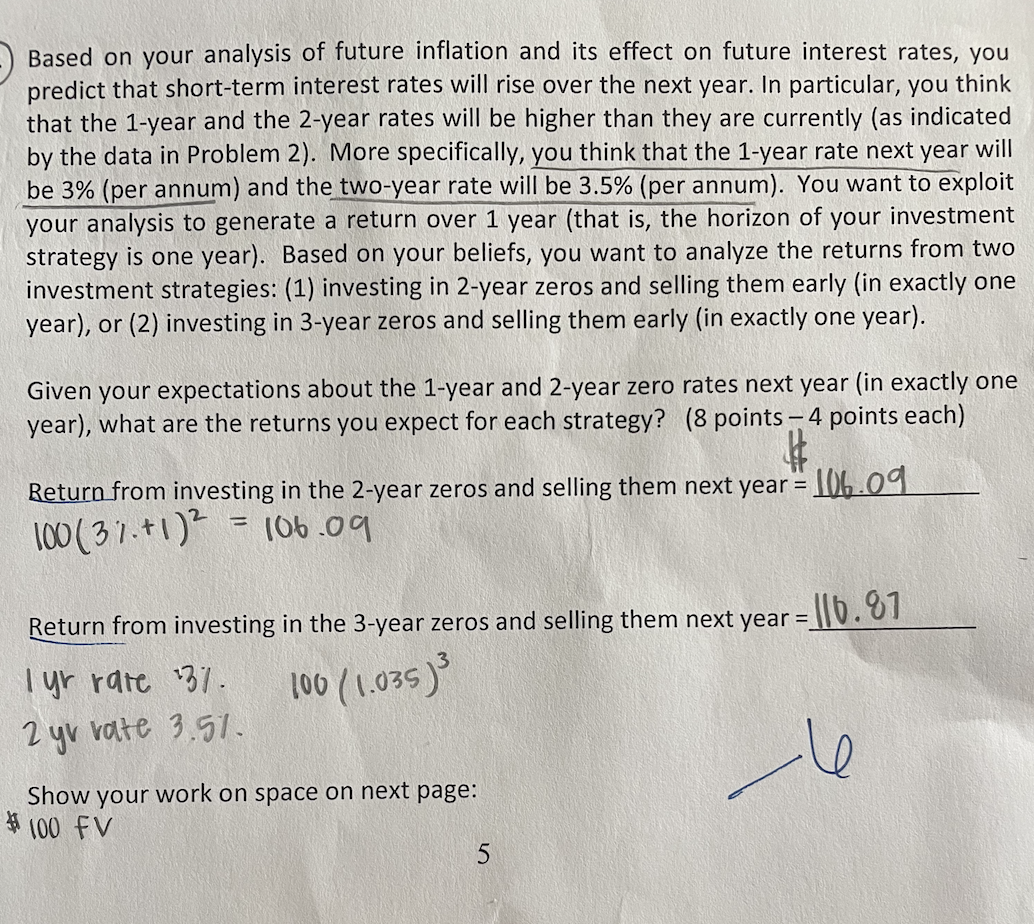

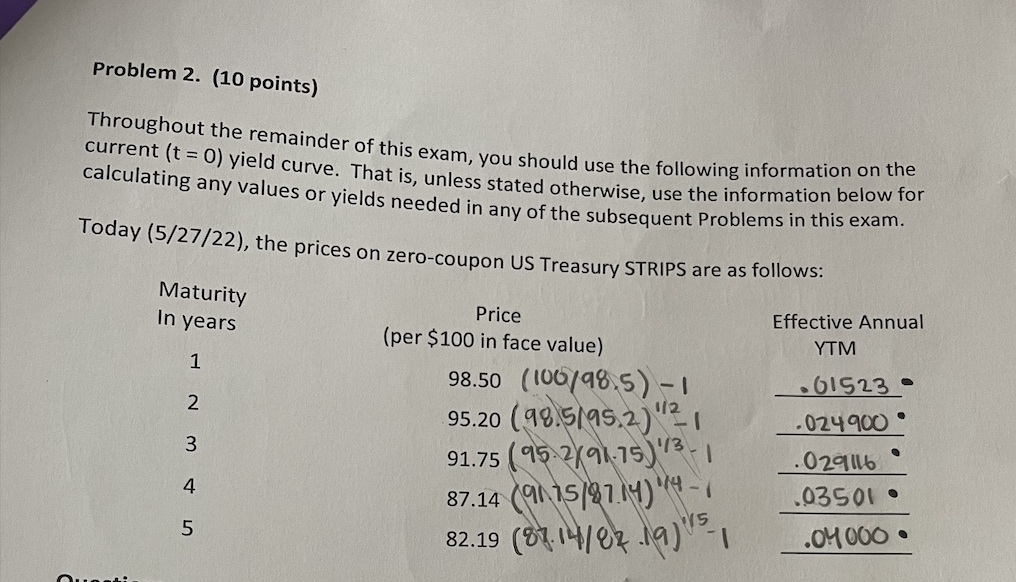

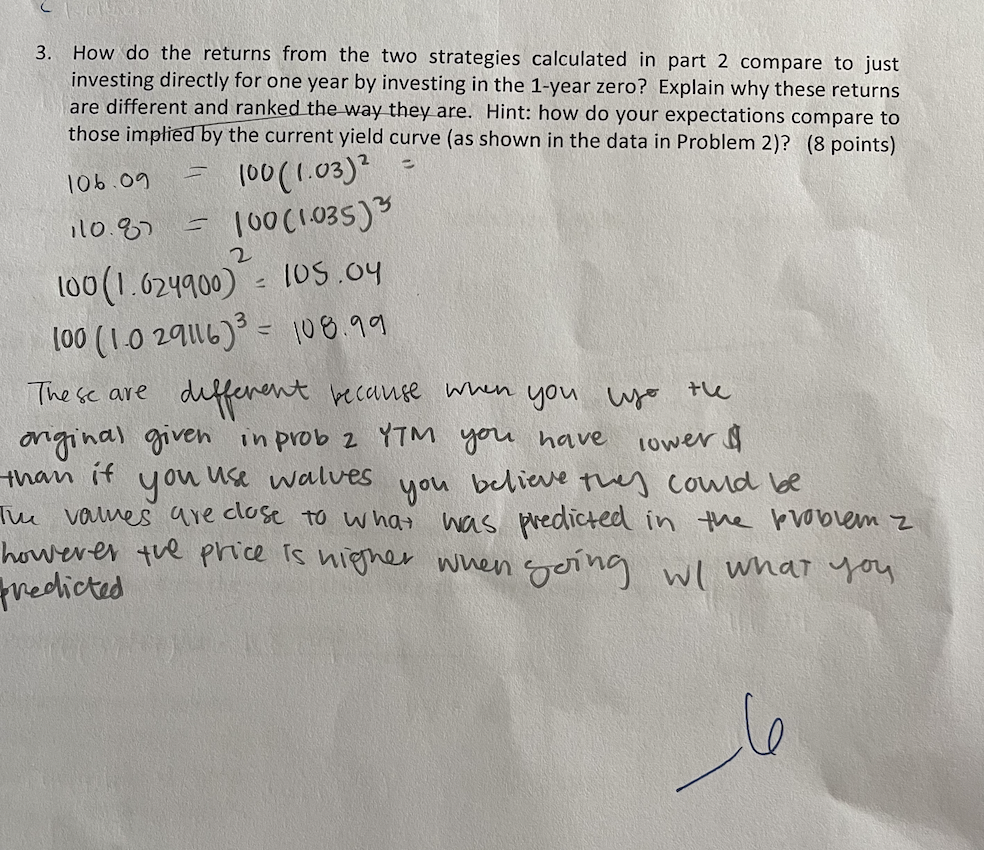

Based on your analysis of future inflation and its effect on future interest rates, you predict that short-term interest rates will rise over the next year. In particular, you think that the 1-year and the 2-year rates will be higher than they are currently (as indicated by the data in Problem 2). More specifically, you think that the 1-year rate next year will be 3% (per annum) and the two-year rate will be 3.5% (per annum). You want to exploit your analysis to generate a return over 1 year (that is, the horizon of your investment strategy is one year). Based on your beliefs, you want to analyze the returns from two investment strategies: (1) investing in 2-year zeros and selling them early (in exactly one year), or (2) investing in 3-year zeros and selling them early (in exactly one year). Given your expectations about the 1-year and 2-year zero rates next year (in exactly one year), what are the returns you expect for each strategy? (8 points - 4 points each) # Return from investing in the 2-year zeros and selling them next year = 100 (37%.+1) = 106.09 106.09 Return from investing in the 3-year zeros and selling them next year = 1 yr rate 3%. 100 (1.035) 2 yv vate 3.5%. Show your work on space on next page: #100 FV 5 116.87 Problem 2. (10 points) Throughout the remainder of this exam, you should use the following information on the current (t = 0) yield curve. That is, unless stated otherwise, use the information below for calculating any values or yields needed in any of the subsequent Problems in this exam. Today (5/27/22), the prices on zero-coupon US Treasury STRIPS are as follows: Maturity In years Price (per $100 in face value) Effective Annual YTM 1 98.50 (106/98.5) - 1 .61523 1/2 95.20 (98.5/95.2) -1 -024900 91.75 (95-291-75) 13. .029116 .03501. 87.14 (9175/87.14) - 82.19 (87.14/82-19) 15-1 1.04000. Questi ~ 3 4 5 2 CLAS 3. How do the returns from the two strategies calculated in part 2 compare to just investing directly for one year by investing in the 1-year zero? Explain why these returns are different and ranked the way they are. Hint: how do your expectations compare to those implied by the current yield curve (as shown in the data in Problem 2)? (8 points) 106.09 100 (1.03) = 110.87 5 100 (1.035)3 2 100(1.624900) 105.04 2 100 (1-0 29116)3= 108.99 lower These are different because when you yo the original given in prob 2 YTM you have than if you use walves you believe they could be The values are close to what was predicted in the problem z however the price is higher when going redicted w what you Based on your analysis of future inflation and its effect on future interest rates, you predict that short-term interest rates will rise over the next year. In particular, you think that the 1-year and the 2-year rates will be higher than they are currently (as indicated by the data in Problem 2). More specifically, you think that the 1-year rate next year will be 3% (per annum) and the two-year rate will be 3.5% (per annum). You want to exploit your analysis to generate a return over 1 year (that is, the horizon of your investment strategy is one year). Based on your beliefs, you want to analyze the returns from two investment strategies: (1) investing in 2-year zeros and selling them early (in exactly one year), or (2) investing in 3-year zeros and selling them early (in exactly one year). Given your expectations about the 1-year and 2-year zero rates next year (in exactly one year), what are the returns you expect for each strategy? (8 points - 4 points each) # Return from investing in the 2-year zeros and selling them next year = 100 (37%.+1) = 106.09 106.09 Return from investing in the 3-year zeros and selling them next year = 1 yr rate 3%. 100 (1.035) 2 yv vate 3.5%. Show your work on space on next page: #100 FV 5 116.87 Problem 2. (10 points) Throughout the remainder of this exam, you should use the following information on the current (t = 0) yield curve. That is, unless stated otherwise, use the information below for calculating any values or yields needed in any of the subsequent Problems in this exam. Today (5/27/22), the prices on zero-coupon US Treasury STRIPS are as follows: Maturity In years Price (per $100 in face value) Effective Annual YTM 1 98.50 (106/98.5) - 1 .61523 1/2 95.20 (98.5/95.2) -1 -024900 91.75 (95-291-75) 13. .029116 .03501. 87.14 (9175/87.14) - 82.19 (87.14/82-19) 15-1 1.04000. Questi ~ 3 4 5 2 CLAS 3. How do the returns from the two strategies calculated in part 2 compare to just investing directly for one year by investing in the 1-year zero? Explain why these returns are different and ranked the way they are. Hint: how do your expectations compare to those implied by the current yield curve (as shown in the data in Problem 2)? (8 points) 106.09 100 (1.03) = 110.87 5 100 (1.035)3 2 100(1.624900) 105.04 2 100 (1-0 29116)3= 108.99 lower These are different because when you yo the original given in prob 2 YTM you have than if you use walves you believe they could be The values are close to what was predicted in the problem z however the price is higher when going redicted w what you