Answered step by step

Verified Expert Solution

Question

1 Approved Answer

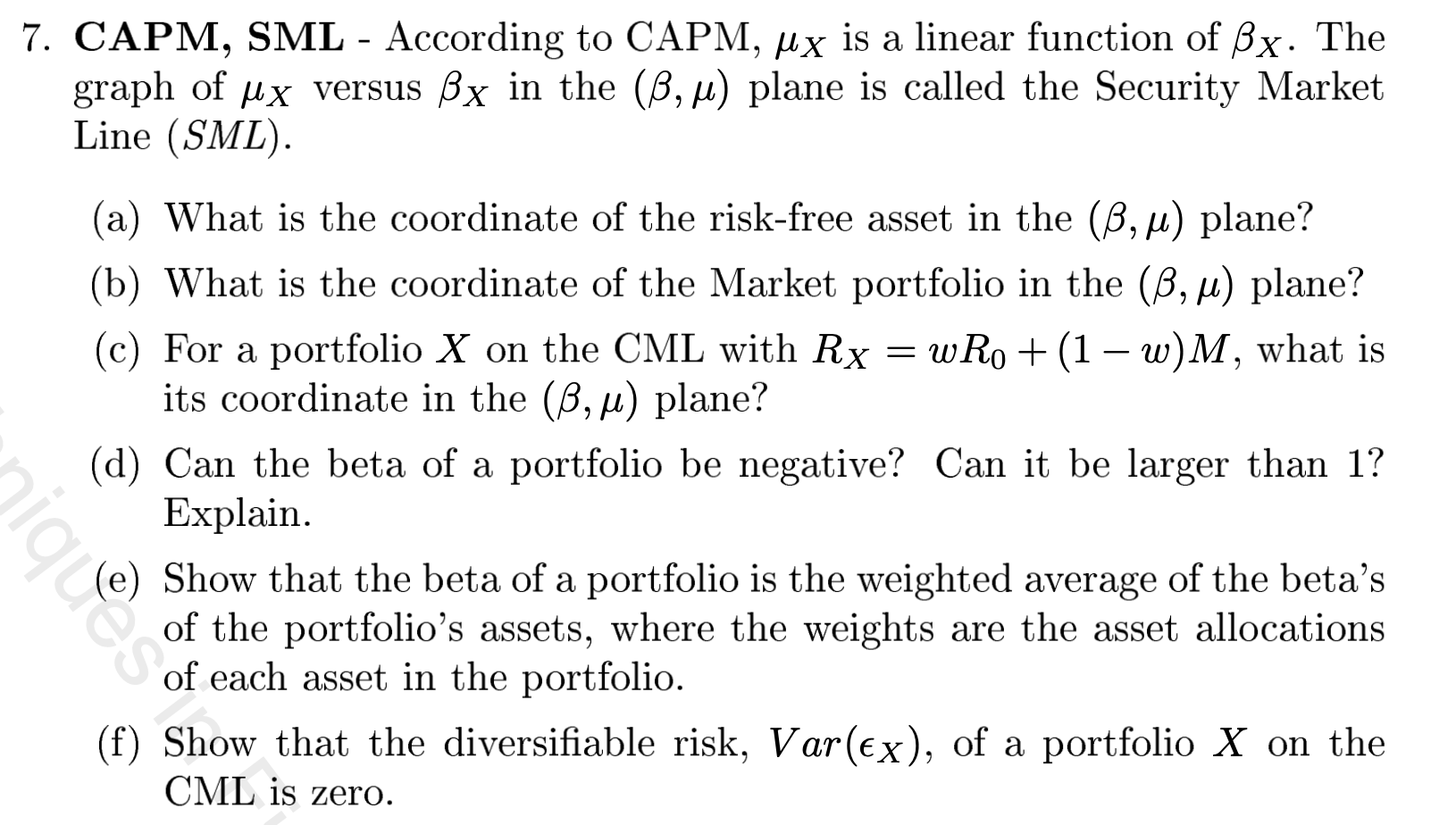

Question on part C, E, F 7. CAPM, SML - According to CAPM, ux is a linear function of Bx. The graph of ux versus

Question on part C, E, F

7. CAPM, SML - According to CAPM, ux is a linear function of Bx. The graph of ux versus Bx in the (B,M) plane is called the Security Market Line (SML). (a) What is the coordinate of the risk-free asset in the (B, u) plane? (b) What is the coordinate of the Market portfolio in the (B, u plane? (c) For a portfolio X on the CML with Rx wR0 + (1 w)M, what is its coordinate in the (B,u) plane? (d) Can the beta of a portfolio be negative? Can it be larger than 1? Explain. Show that the beta of a portfolio is the weighted average of the beta's of the portfolio's assets, where the weights are the asset allocations of each asset in the portfolio. (f) Show that the diversifiable risk, Var(ex), of a portfolio X on the CML is zero. an bi 7. CAPM, SML - According to CAPM, ux is a linear function of Bx. The graph of ux versus Bx in the (B,M) plane is called the Security Market Line (SML). (a) What is the coordinate of the risk-free asset in the (B, u) plane? (b) What is the coordinate of the Market portfolio in the (B, u plane? (c) For a portfolio X on the CML with Rx wR0 + (1 w)M, what is its coordinate in the (B,u) plane? (d) Can the beta of a portfolio be negative? Can it be larger than 1? Explain. Show that the beta of a portfolio is the weighted average of the beta's of the portfolio's assets, where the weights are the asset allocations of each asset in the portfolio. (f) Show that the diversifiable risk, Var(ex), of a portfolio X on the CML is zero. an biStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance A Quantitative Introduction

Authors: Nico Van Der Wijst

1st Edition

1107029228, 978-1107029224