Answered step by step

Verified Expert Solution

Question

1 Approved Answer

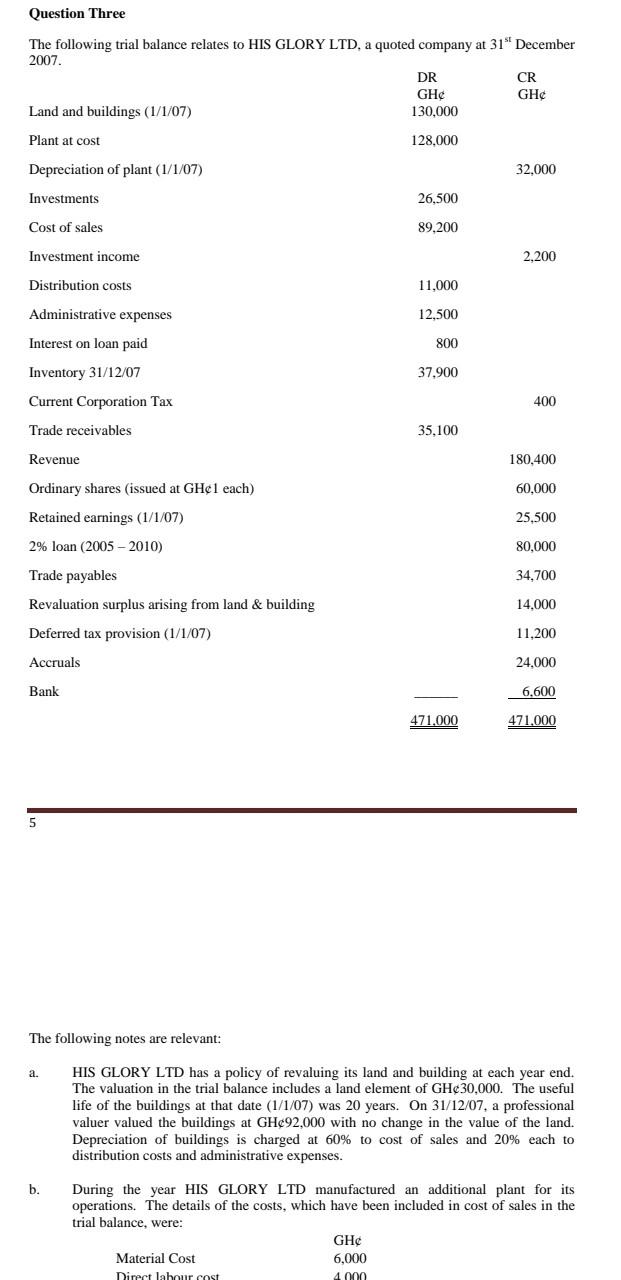

Question Three The following trial balance relates to HIS GLORY LTD, a quoted company at 31 December 2007. DR CR GH GHC Land and buildings

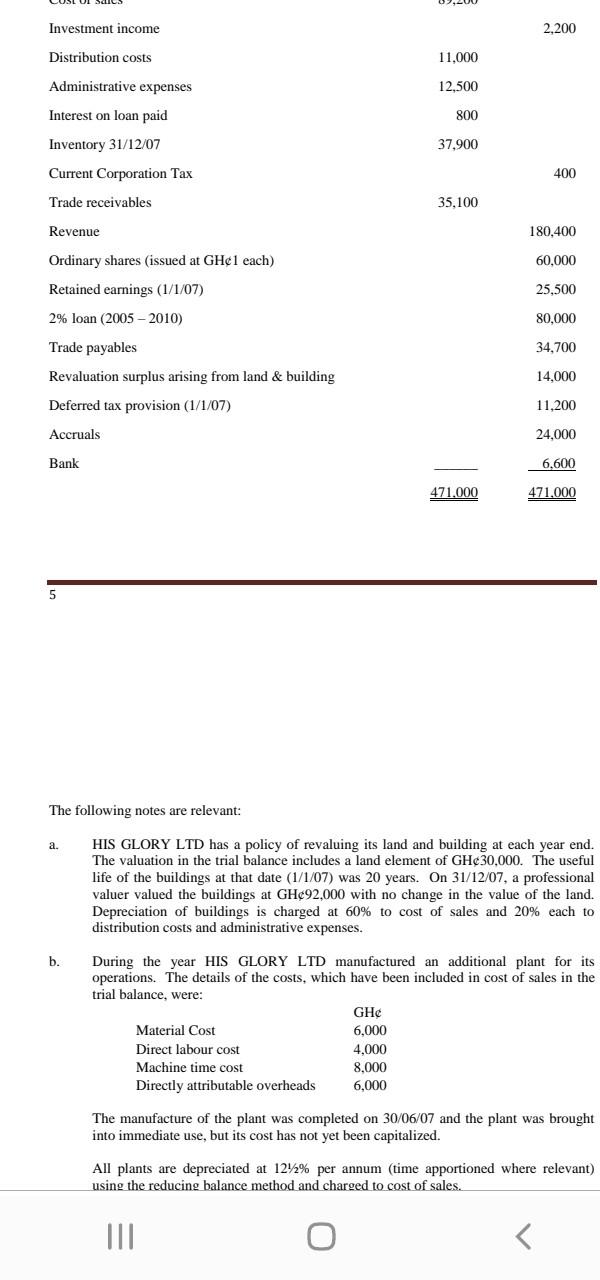

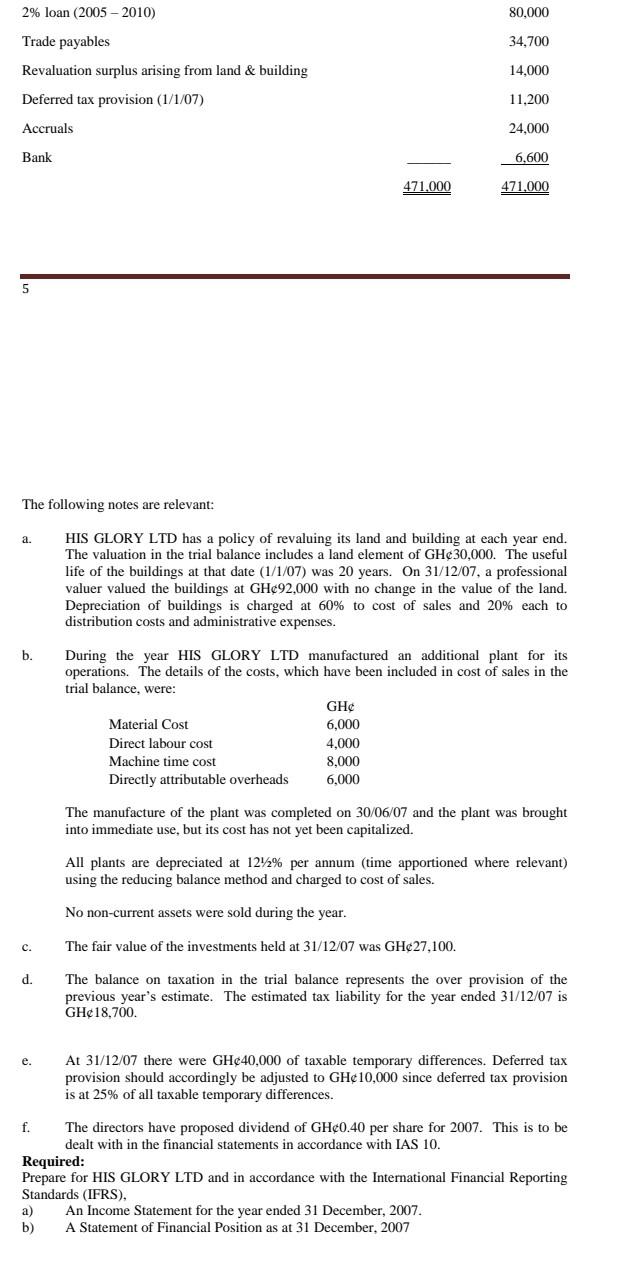

Question Three The following trial balance relates to HIS GLORY LTD, a quoted company at 31" December 2007. DR CR GH GHC Land and buildings (1/1/07) 130,000 Plant at cost 128.000 Depreciation of plant (1/1/07) 32,000 Investments 26,500 Cost of sales 89.200 Investment income 2,200 Distribution costs Administrative expenses Interest on loan paid 11,000 12,500 800 Inventory 31/12/07 37.900 Current Corporation Tax 400 Trade receivables 35.100 Revenue 180,400 Ordinary shares (issued at GH1 each) 60,000 Retained earnings (1/1/07) 2% loan (2005-2010) 25,500 80,000 34,700 Trade payables Revaluation surplus arising from land & building Deferred tax provision (1/1/07) 14.000 11,200 Accruals 24.000 Bank 6,600 471.000 471,000 5 The following notes are relevant: a. HIS GLORY LTD has a policy of revaluing its land and building at each year end. The valuation in the trial balance includes a land element of GH30,000. The useful life of the buildings at that date (1/1/07) was 20 years. On 31/12/07, a professional valuer valued the buildings at GH92,000 with no change in the value of the land. Depreciation of buildings is charged at 60% to cost of sales and 20% each to distribution costs and administrative expenses. b. During the year HIS GLORY LTD manufactured an additional plant for its operations. The details of the costs, which have been included in cost of sales in the trial balance, were: GHC Material Cost 6,000 Direct labour cost 4.000 Investment income 2,200 Distribution costs 11,000 12,500 Administrative expenses Interest on loan paid 800 Inventory 31/12/07 37.900 Current Corporation Tax 400 Trade receivables 35.100 Revenue 180,400 Ordinary shares (issued at GH1 each) 60,000 Retained earnings (1/1/07) 25.500 2% loan (2005-2010) 80,000 Trade payables 34,700 Revaluation surplus arising from land & building 14,000 Deferred tax provision (1/1/07) 11,200 Accruals 24,000 Bank 6,600 471,000 471,000 5 The following notes are relevant: a. HIS GLORY LTD has a policy of revaluing its land and building at each year end. The valuation in the trial balance includes a land element of GH30,000. The useful life of the buildings at that date 1/1/07) was 20 years. On 31/12/07, a professional valuer valued the buildings at GH92,000 with no change in the value of the land. Depreciation of buildings is charged at 60% to cost of sales and 20% each to distribution costs and administrative expenses. b. During the year HIS GLORY LTD manufactured an additional plant for its operations. The details of the costs, which have been included in cost of sales in the trial balance, were: GH Material Cost 6,000 Direct labour cost 4,000 Machine time cost 8,000 Directly attributable overheads 6.000 The manufacture of the plant was completed on 30/06/07 and the plant was brought into immediate use, but its cost has not yet been capitalized. All plants are depreciated at 1242% per annum (time apportioned where relevant) using the reducing balance method and charged to cost of sales. III

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sampling Theory In The Auditing Of Nuclear Materials Accountancy Statistical Modeling Of Accountancy And Audit

Authors: Dictus

1st Edition

3844365427, 978-3844365429