Answered step by step

Verified Expert Solution

Question

1 Approved Answer

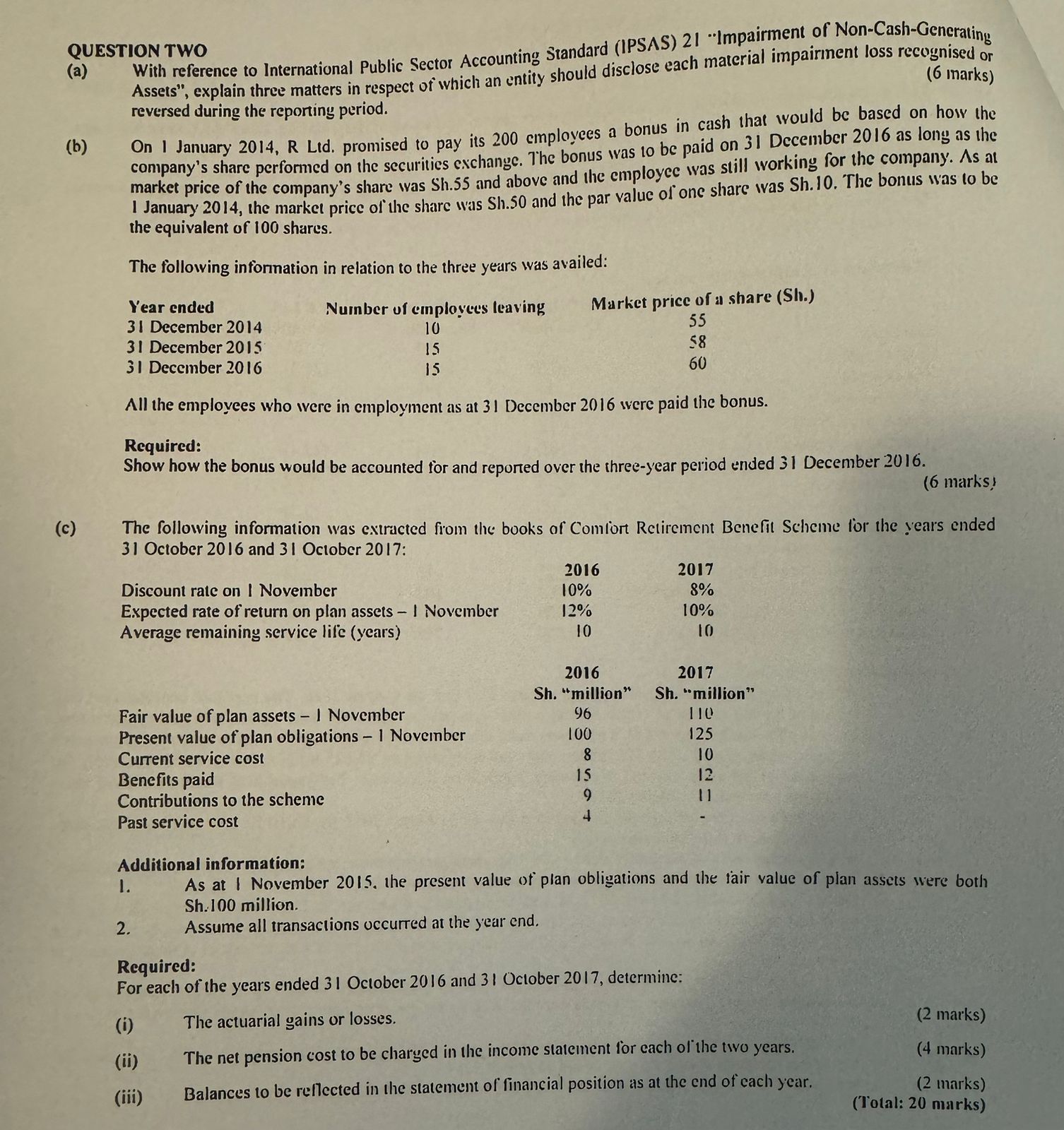

QUESTION TWO ( a ) With reference to International Public Sector Accounting standard ( IPSAS ) 2 1 Impairment of Non - Cash - Generating

QUESTION TWO

a With reference to International Public Sector Accounting standard IPSAS "Impairment of NonCashGenerating

Assets", explain three matters in respect of which an entity should disclose each material impairment loss recognised or

reversed during the reporting period.

marks

On January R Lid. promised to pay its employees a bonus in cash that would be based on how the

company's share performed on the securities exchange. The bonus was to be paid on December as long as the

market price of the company's share was Sh and above and the employee was still working for the company. s at

I January the market price of the share was Sh and the par value of one share was Sh The bonus was to be

the equivalent of shares.

The following information in relation to the three years was availed:

Year ended

December

December

December

Number uf employeess leaving

Market price of a share Sli

All the employees who were in employment as at December were paid the bonus.

Required:

Show how the bonus would be accounted for and reported over the threeyear period ended December

c The following information was extracted from the books of Comlior Retirement Benefit Scheme for the years ended

October and October :

Discount rate on I November

Expected rate of return on plan assets November

Average remaining service life years

Sh "million"

Fair value of plan assets I November

Present value of plan obligations November

Current service cost

Benefits paid

Contributions to the scheme

Past service cost

Sh "million"

Additional information:

As at I November the present value of plan obligations and the tair value of plan assets were both

Sh million.

Assume all transactions occurred at the year end.

Required:

For each of the years ended October and October determine:

i The actuarial gains or losses.

ii The net pension cost to be charged in the income statement for each of the two years.

iii Balances to be reflected in the statement of financial position as at the end of each year.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting A Critical Approach

Authors: John Friedlan

1st Edition

0130193720, 978-0130193728