Answered step by step

Verified Expert Solution

Question

1 Approved Answer

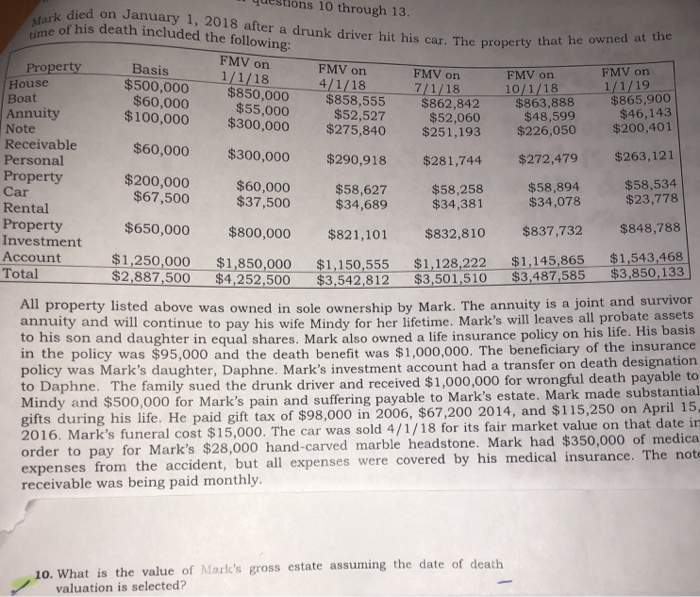

questions 10 through 13 died on January 1, 2018 after a drunk driver hit his car. The propertyt his death included the following: that he

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Connect For Computer Accounting With Quickbooks 2021

Authors: Author

20th Edition

1264069200, 9781264069200