Answered step by step

Verified Expert Solution

Question

1 Approved Answer

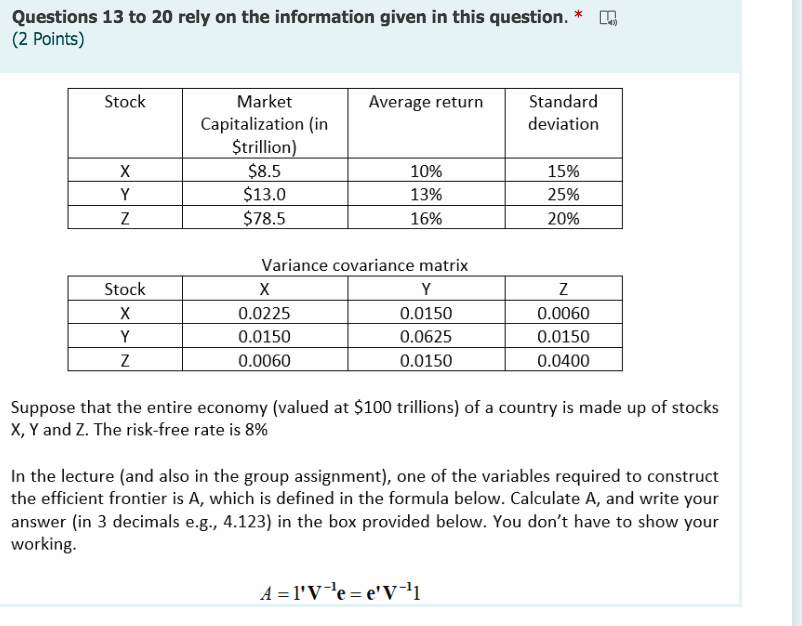

Questions 13 to 20 rely on the information given in this question. (2 Points) * Stock Market Capitalization (in Average return Standard deviation $trillion)

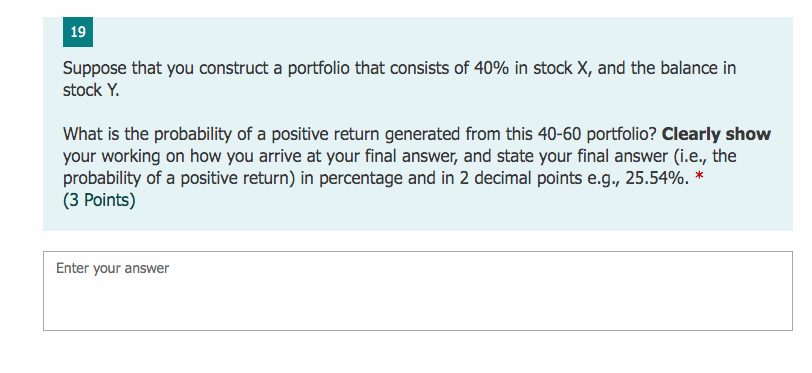

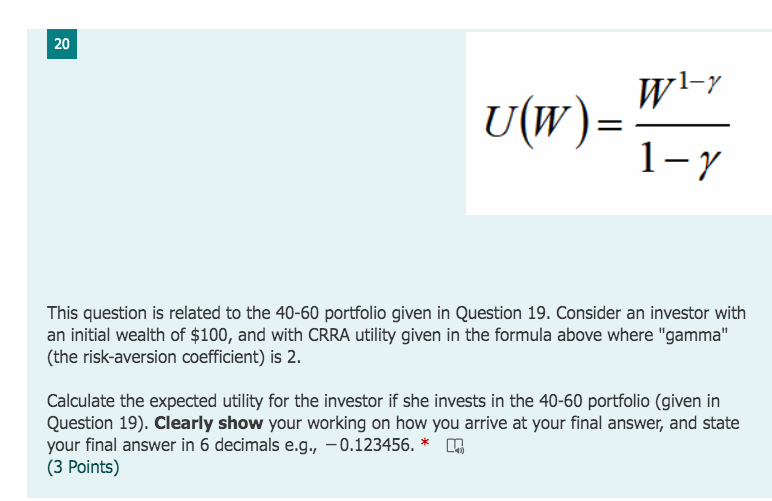

Questions 13 to 20 rely on the information given in this question. (2 Points) * Stock Market Capitalization (in Average return Standard deviation $trillion) X $8.5 10% 15% Y $13.0 13% 25% Z $78.5 16% 20% Variance covariance matrix Stock X 0.0225 Y 0.0150 Z 0.0060 Y Z 0.0150 0.0060 0.0625 0.0150 0.0150 0.0400 Suppose that the entire economy (valued at $100 trillions) of a country is made up of stocks X, Y and Z. The risk-free rate is 8% In the lecture (and also in the group assignment), one of the variables required to construct the efficient frontier is A, which is defined in the formula below. Calculate A, and write your answer (in 3 decimals e.g., 4.123) in the box provided below. You don't have to show your working. A l'Ve e'V-1 19 Suppose that you construct a portfolio that consists of 40% in stock X, and the balance in stock Y. What is the probability of a positive return generated from this 40-60 portfolio? Clearly show your working on how you arrive at your final answer, and state your final answer (i.e., the probability of a positive return) in percentage and in 2 decimal points e.g., 25.54%. * (3 Points) Enter your answer 20 20 U(W)= W1-y 1-Y This question is related to the 40-60 portfolio given in Question 19. Consider an investor with an initial wealth of $100, and with CRRA utility given in the formula above where "gamma" (the risk-aversion coefficient) is 2. Calculate the expected utility for the investor if she invests in the 40-60 portfolio (given in Question 19). Clearly show your working on how you arrive at your final answer, and state your final answer in 6 decimals e.g., -0.123456.* (3 Points)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Derivatives Markets

Authors: Robert McDonald

3rd Edition

978-9332536746, 9789332536746