Answered step by step

Verified Expert Solution

Question

1 Approved Answer

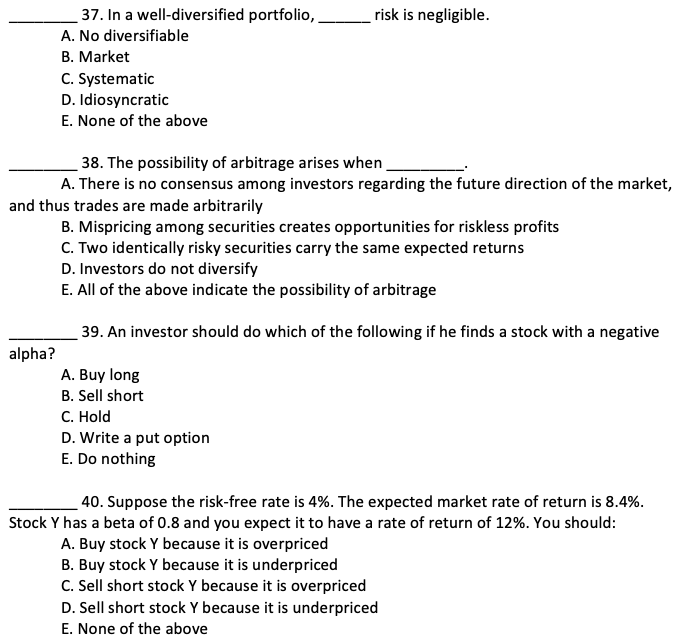

questions 37-40 please risk is negligible. 37. In a well-diversified portfolio, A. No diversifiable B. Market C. Systematic D. Idiosyncratic E. None of the above

questions 37-40 please

risk is negligible. 37. In a well-diversified portfolio, A. No diversifiable B. Market C. Systematic D. Idiosyncratic E. None of the above 38. The possibility of arbitrage arises when A. There is no consensus among investors regarding the future direction of the market, and thus trades are made arbitrarily B. Mispricing among securities creates opportunities for riskless profits C. Two identically risky securities carry the same expected returns D. Investors do not diversify E. All of the above indicate the possibility of arbitrage 39. An investor should do which of the following if he finds a stock with a negative alpha? A. Buy long B. Sell short C. Hold D. Write a put option E. Do nothing 40. Suppose the risk-free rate is 4%. The expected market rate of return is 8.4%. Stock Y has a beta of 0.8 and you expect it to have a rate of return of 12%. You should: A. Buy stock Y because it is overpriced B. Buy stock Y because it is underpriced C. Sell short stock y because it is overpriced D. Sell short stock Y because it is underpriced E. None of the aboveStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Fiscal Impact Handbook

Authors: David Listokin

1st Edition

1138535672, 978-1138535671