Answered step by step

Verified Expert Solution

Question

1 Approved Answer

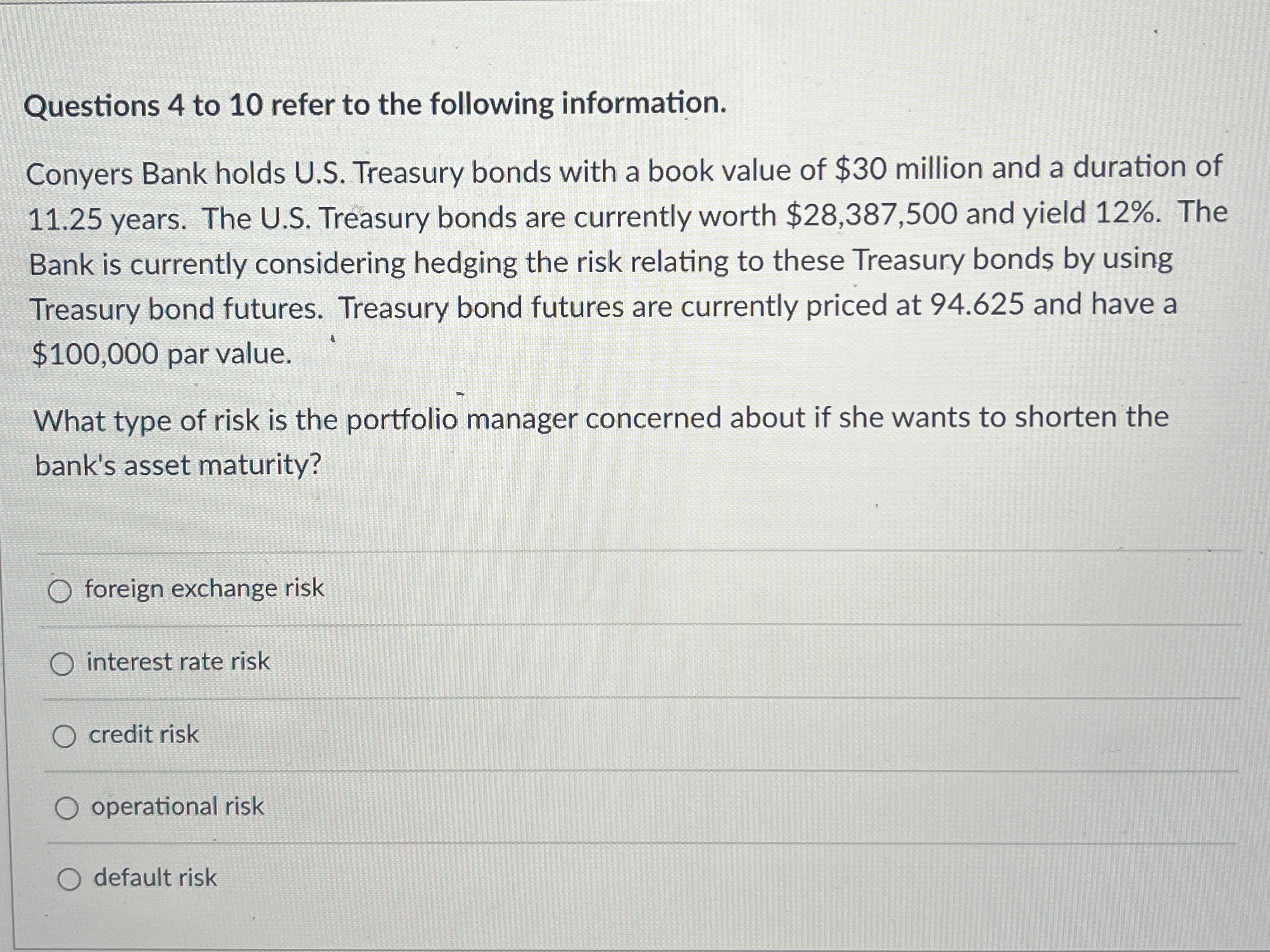

Questions 4 to 1 0 refer to the following information. Conyers Bank holds U . S . Treasury bonds with a book value of $

Questions to refer to the following information.

Conyers Bank holds US Treasury bonds with a book value of $ million and a duration of years. The US Treasury bonds are currently worth $ and yield The Bank is currently considering hedging the risk relating to these Treasury bonds by using Treasury bond futures. Treasury bond futures are currently priced at and have a $ par value.

Which of the following statements is TRUE if the bank's portfolio manager wants to shorten asset maturities?

The portfolio manager is willing to sell the bonds outright since they are more valuable than their book value.

The portfolio manager should do nothing.

The portfolio manager is reluctant to sell the bonds outright since the bank will have to take a loss.

The portfolio manager is reluctant to sell the bonds outright since the bank will have to pay taxes on the gain.

The portfolio manager is willing to sell the bonds outright since they are not as valuable as their book value.

Questions to refer to the following information.

Conyers Bank holds US Treasury bonds with a book value of $ million and a duration of years. The US Treasury bonds are currently worth $ and yield The Bank is currently considering hedging the risk relating to these Treasury bonds by using Treasury bond futures. Treasury bond futures are currently priced at and have a $ par value.

What type of risk is the portfolio manager concerned about if she wants to shorten the bank's asset maturity?

foreign exchange risk

interest rate risk

credit risk

operational risk

default risk

Questions to refer to the following information.

Conyers Bank holds US Treasury bonds with a book value of $ million and a duration of years. The US Treasury bonds are currently worth $ and yield The Bank is currently considering hedging the risk relating to these Treasury bonds by using Treasury bond futures. Treasury bond futures are currently priced at and have a $ par value.

What type of risk is the portfolio manager concerned about if she wants to shorten the bank's asset maturity?

foreign exchange risk

interest rate risk

credit risk

operational risk

default risk

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Stability Website Fraud Confidence And The Wealth Of Nations

Authors: Frederick L. Feldkamp, R. Christopher Whalen

2nd Edition

1118935799, 978-1118935798