Answered step by step

Verified Expert Solution

Question

1 Approved Answer

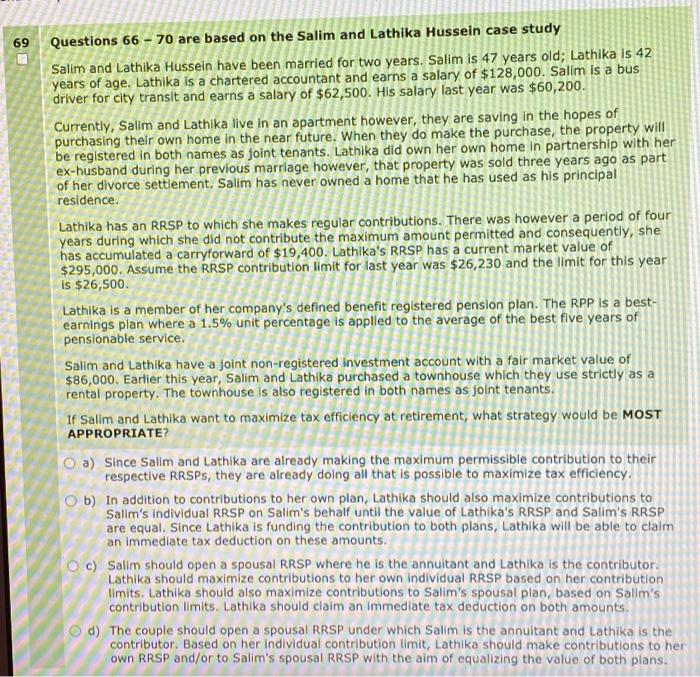

Questions 6670 are based on the Salim and Lathika Hussein case study Salim and Lathika Hussein have been married for two years. Salim is 47

Questions 6670 are based on the Salim and Lathika Hussein case study Salim and Lathika Hussein have been married for two years. Salim is 47 years old; Lathika is 42 years of age. Lathika is a chartered accountant and earns a salary of $128,000. Salim is a bus driver for city transit and earns a salary of $62,500. His salary last year was $60,200. Currently, Salim and Lathika live in an apartment however, they are saving in the hopes of purchasing their own home in the near future. When they do make the purchase, the property will be registered in both names as joint tenants. Lathika did own her own home in partnership with her ex-husband during her previous marriage however, that property was sold three years ago as part of her divorce settlement. Salim has never owned a home that he has used as his principal residence. Lathika has an RRSP to which she makes regular contributions. There was however a period of four years during which she did not contribute the maximum amount permitted and consequently, she has accumulated a carryforward of $19,400. Lathika's RRSP has a current market value of $295,000. Assume the RRSP contribution limit for last year was $26,230 and the limit for this year is $26,500. Lathika is a member of her company's defined benefit registered pension plan. The RPP is a bestearnings plan where a 1.5% unit percentage is applied to the average of the best five years of pensionable service. Salim and Lathika have a joint non-registered investment account with a fair market value of $86,000. Earlier this year, Salim and Lathika purchased a townhouse which they use strictly as a rental property. The townhouse is also registered in both names as joint tenants. If Salim and Lathika want to maximize tax efficiency at retirement, what strategy would be MOST APPROPRIATE? a) Since Salim and Lathika are already making the maximum permissible contribution to their respective RRSPs, they are already doing all that is possible to maximize tax efficiency. b) In addition to contributions to her own plan, Lathika should also maximize contributions to Salim's individual RRSP on Salim's behalf until the value of Lathika's RRSP and Salim's RRSP are equal. Since Lathika is funding the contribution to both plans, Lathika will be able to claim an immediate tax deduction on these amounts. c) Salim should open a spousal RRSP where he is the annuitant and Lathika is the contributor. Lathika should maximize contributions to her own individual RRSP based on her contribution limits. Lathika should also maximize contributions to Salim's spousal plan, based on Salim's contribution limits. Lathika should claim an immediate tax deduction on both amounts. d) The couple should open a spousal RRSP under which Salim is the annuitant and Lathika is the contributor. Based on her individual contribution limit, Lathika should make contributions to her own RRSP and/or to Salim's spousal RRSP with the aim of equalizing the value of both plans

Questions 6670 are based on the Salim and Lathika Hussein case study Salim and Lathika Hussein have been married for two years. Salim is 47 years old; Lathika is 42 years of age. Lathika is a chartered accountant and earns a salary of $128,000. Salim is a bus driver for city transit and earns a salary of $62,500. His salary last year was $60,200. Currently, Salim and Lathika live in an apartment however, they are saving in the hopes of purchasing their own home in the near future. When they do make the purchase, the property will be registered in both names as joint tenants. Lathika did own her own home in partnership with her ex-husband during her previous marriage however, that property was sold three years ago as part of her divorce settlement. Salim has never owned a home that he has used as his principal residence. Lathika has an RRSP to which she makes regular contributions. There was however a period of four years during which she did not contribute the maximum amount permitted and consequently, she has accumulated a carryforward of $19,400. Lathika's RRSP has a current market value of $295,000. Assume the RRSP contribution limit for last year was $26,230 and the limit for this year is $26,500. Lathika is a member of her company's defined benefit registered pension plan. The RPP is a bestearnings plan where a 1.5% unit percentage is applied to the average of the best five years of pensionable service. Salim and Lathika have a joint non-registered investment account with a fair market value of $86,000. Earlier this year, Salim and Lathika purchased a townhouse which they use strictly as a rental property. The townhouse is also registered in both names as joint tenants. If Salim and Lathika want to maximize tax efficiency at retirement, what strategy would be MOST APPROPRIATE? a) Since Salim and Lathika are already making the maximum permissible contribution to their respective RRSPs, they are already doing all that is possible to maximize tax efficiency. b) In addition to contributions to her own plan, Lathika should also maximize contributions to Salim's individual RRSP on Salim's behalf until the value of Lathika's RRSP and Salim's RRSP are equal. Since Lathika is funding the contribution to both plans, Lathika will be able to claim an immediate tax deduction on these amounts. c) Salim should open a spousal RRSP where he is the annuitant and Lathika is the contributor. Lathika should maximize contributions to her own individual RRSP based on her contribution limits. Lathika should also maximize contributions to Salim's spousal plan, based on Salim's contribution limits. Lathika should claim an immediate tax deduction on both amounts. d) The couple should open a spousal RRSP under which Salim is the annuitant and Lathika is the contributor. Based on her individual contribution limit, Lathika should make contributions to her own RRSP and/or to Salim's spousal RRSP with the aim of equalizing the value of both plans Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Agricultural Finance

Authors: Charles Moss

1st Edition

0415599075, 978-0415599078