Questions: D-F, There is another post for A-C.

https://www.chegg.com/homework-help/questions-and-answers/suppose-hired-financial-consultant-defense-electronics-inc-dei--large-publicly-traded-firm-q96673691

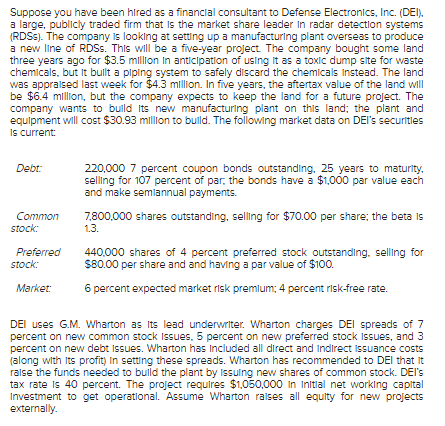

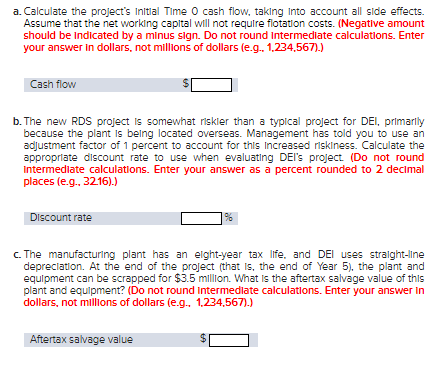

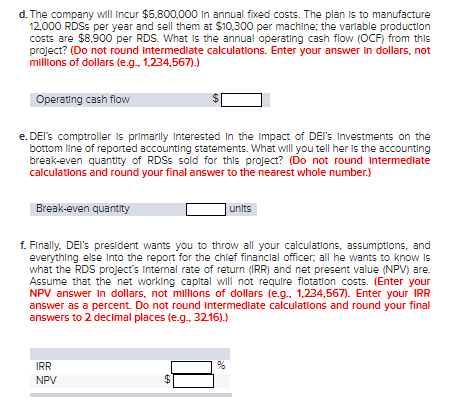

Suppose you have been hired as a financial consultant to Defense Electronics, Inc. (DEI). a large, publicly traded firm that is the market share leader in radar detection systems (RDSS). The company is looking at setting up a manufacturing plant overseas to produce a new line of RDSs. This will be a five-year project. The company bought some land three years ago for $3.5 million in anticipation of using it as a toxic dump site for waste chemicals, but it bullt a piping system to safely discard the chemicals instead. The land was appraised last week for $4.3 million. In five years, the aftertax value of the land will be $6.4 million, but the company expects to keep the land for a future project. The company wants to build its new manufacturing plant on this land; the plant and equipment will cost $30.93 million to build. The following market data on DEI's securities is current: Debt: 220.000 7 percent coupon bonds outstanding, 25 years to maturity. selling for 107 percent of par, the bonds have a $1.000 par value each and make semiannual payments. 7.800.000 shares outstanding, selling for $70.00 per share the beta is Common stock: 13. Preferred stock: 440.000 shares of 4 percent preferred stock outstanding, selling for $80.00 per share and and having a par value of $100. 6 percent expected market risk premium: 4 percent risk-free rate. Market: DEI uses G.M. Wharton as its lead underwriter. Wharton charges DEI spreads of 7 percent on new common stock issues, 5 percent on new preferred stock issues, and 3 percent on new debt issues. Wharton has included all direct and Indirect Issuance costs (along with its profit) In setting these spreads. Wharton has recommended to DEI that it raise the funds needed to build the plant by Issuing new shares of common stock. DEI's tax rate is 40 percent. The project requires $1,050,000 in Initial net working capital Investment to get operational. Assume Wharton raises all equity for new projects externally. a. Calculate the project's Initial Time O cash flow, taking into account all side effects. Assume that the networking capital will not require flotation costs. (Negative amount should be indicated by a minus sign. Do not round Intermediate calculations. Enter your answer in dollars, not millions of dollars (e.g.. 1.234,567).) Cash flow b. The new RDS project is somewhat riskler than a typical project for DEI, primarily because the plant is being located overseas. Management has told you to use an adjustment factor of 1 percent to account for this increased riskiness. Calculate the appropriate discount rate to use when evaluating DEI's project (Do not round Intermediate calculations. Enter your answer as a percent rounded to 2 decimal places (e.g. 32.16).) Discount rate c. The manufacturing plant has an elght-year tax life, and DEI uses straight-line depreciation. At the end of the project (that is, the end of Year 5). the plant and equipment can be scrapped for $3.5 million. What is the aftertax salvage value of this plant and equipment? (Do not round Intermediate calculations. Enter your answer in dollars, not millions of dollars (e.g. 1,234,567).) Aftertax salvage value $ d. The company will incur $5.800,000 in annual fixed costs. The plan is to manufacture 12,000 RDSS per year and sell them at $10.300 per machine; the varlable production costs are $8.900 per RDS. What is the annual operating cash flow (OCF) from this project? (Do not round intermediate calculations. Enter your answer in dollars, not millions of dollars (e.g.. 1,234,567).) Operating cash flow e. DEI's comptroller is primarily Interested in the Impact of DEI's Investments on the bottom line of reported accounting statements. What will you tell her is the accounting break-even quantity of RDSs sold for this project? (Do not round Intermediate calculations and round your final answer to the nearest whole number.) Break-even quantity units f. Finally. DEI's president wants you to throw all your calculations, assumptions, and everything else Into the report for the chief financial officer, all he wants to know is what the RDS project's Internal rate of return (IRR) and net present value (NPV) are. Assume that the net working capital will not require flotation costs. (Enter your NPV answer in dollars, not millions of dollars (e.... 1,234,567). Enter your IRR answer as a percent. Do not round Intermediate calculations and round your final answers to 2 decimal places (e.g.. 3216).) % IRR NPV B C D E 6 000 7 $ 8 $ Land price Current land value Land value in 5 years Plant & Equipment cost 3,500,000 4,300,000 6,400,000 30,930,000 9 $ 10 $ 11 12 . 13 0 14 15 16 Debt Bonds outstanding Years to Maturity Annual coupon rate Coupons per year Face value (% of par) Bond price (% of par) 220,000 25 7.00% 2 1,000.00 1.07 17 18 19 20 21 Common stock Shares outstanding Beta Share price 7,800,000 22 1.30 N N 23 $ 70.00 2 24 25 26 Preferred stock outstanding Shares outstanding Coupon rate Share price 27 440,000 4.00% 80.00 28 $ 29 30 31 32 Market Market risk premium Risk-free rate 6.00% 4.00% 33 34 mm m 35 36 Equity flotation cost Preferred flotation cost Debt flotation cost Tax rate Net working capital Does the NWC require flotation costs (Yes/No) 7.00% 5.00% 3.00% 40% 1,050,000 37 38 $ 39 40 no 41 42 1% 43 8 44 45 $ b. Adjustment factor c. Life of plant (years) Life of project (years) Plant salvage value d. Annual fixed costs # RDS manufactured Sale price per RDS Variable costs per RDS 46 $ 8 * * * 5 3,500,000 5,800,000 12,000 10,300 8,900 47 48 $ $ 49 50 A B C D E F G I I 34 Market value of debt Market value of equity Market value of preferred Market value of firm DIV ENV PNV Mark: weighted average flotation costs. See section 12. 11 in text book 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 a. flotation costs The cost of the land 3 years ago is a sunk cost and is irrelevant. Land Plant & Equipment Cost Net working capital Total Time o Mark: See section 12. 11. Gross up items, as appropriate, for flotation costs. b. Pretax cost of debt Aftertax cost of debt Cost of equity Cost of preferred WACC Mark: = WACC + Adjustment for Discount rate for project c. Book value in year 5 Aftertax salvage value 79 80 81 82 83 84 85 86 IN DO Mark: Gross salvage value - ((capital gain or loss) times (1 TR) 87 88 89 90 91 d. Sales Variable costs Fixed costs Depreciation EBIT Taxes Net income Depreciation Operating cash flow Mark: (fixed costs + depr) / (Sales price - variable cost) e. Accounting breakeven Year 92 93 94 95 96 97 98 99 0 Nm+ 3 Mark: 100 = OCF + NWC + NSV + after-tax value of lland 101 102 103 104 IRR NPV Suppose you have been hired as a financial consultant to Defense Electronics, Inc. (DEI). a large, publicly traded firm that is the market share leader in radar detection systems (RDSS). The company is looking at setting up a manufacturing plant overseas to produce a new line of RDSs. This will be a five-year project. The company bought some land three years ago for $3.5 million in anticipation of using it as a toxic dump site for waste chemicals, but it bullt a piping system to safely discard the chemicals instead. The land was appraised last week for $4.3 million. In five years, the aftertax value of the land will be $6.4 million, but the company expects to keep the land for a future project. The company wants to build its new manufacturing plant on this land; the plant and equipment will cost $30.93 million to build. The following market data on DEI's securities is current: Debt: 220.000 7 percent coupon bonds outstanding, 25 years to maturity. selling for 107 percent of par, the bonds have a $1.000 par value each and make semiannual payments. 7.800.000 shares outstanding, selling for $70.00 per share the beta is Common stock: 13. Preferred stock: 440.000 shares of 4 percent preferred stock outstanding, selling for $80.00 per share and and having a par value of $100. 6 percent expected market risk premium: 4 percent risk-free rate. Market: DEI uses G.M. Wharton as its lead underwriter. Wharton charges DEI spreads of 7 percent on new common stock issues, 5 percent on new preferred stock issues, and 3 percent on new debt issues. Wharton has included all direct and Indirect Issuance costs (along with its profit) In setting these spreads. Wharton has recommended to DEI that it raise the funds needed to build the plant by Issuing new shares of common stock. DEI's tax rate is 40 percent. The project requires $1,050,000 in Initial net working capital Investment to get operational. Assume Wharton raises all equity for new projects externally. a. Calculate the project's Initial Time O cash flow, taking into account all side effects. Assume that the networking capital will not require flotation costs. (Negative amount should be indicated by a minus sign. Do not round Intermediate calculations. Enter your answer in dollars, not millions of dollars (e.g.. 1.234,567).) Cash flow b. The new RDS project is somewhat riskler than a typical project for DEI, primarily because the plant is being located overseas. Management has told you to use an adjustment factor of 1 percent to account for this increased riskiness. Calculate the appropriate discount rate to use when evaluating DEI's project (Do not round Intermediate calculations. Enter your answer as a percent rounded to 2 decimal places (e.g. 32.16).) Discount rate c. The manufacturing plant has an elght-year tax life, and DEI uses straight-line depreciation. At the end of the project (that is, the end of Year 5). the plant and equipment can be scrapped for $3.5 million. What is the aftertax salvage value of this plant and equipment? (Do not round Intermediate calculations. Enter your answer in dollars, not millions of dollars (e.g. 1,234,567).) Aftertax salvage value $ d. The company will incur $5.800,000 in annual fixed costs. The plan is to manufacture 12,000 RDSS per year and sell them at $10.300 per machine; the varlable production costs are $8.900 per RDS. What is the annual operating cash flow (OCF) from this project? (Do not round intermediate calculations. Enter your answer in dollars, not millions of dollars (e.g.. 1,234,567).) Operating cash flow e. DEI's comptroller is primarily Interested in the Impact of DEI's Investments on the bottom line of reported accounting statements. What will you tell her is the accounting break-even quantity of RDSs sold for this project? (Do not round Intermediate calculations and round your final answer to the nearest whole number.) Break-even quantity units f. Finally. DEI's president wants you to throw all your calculations, assumptions, and everything else Into the report for the chief financial officer, all he wants to know is what the RDS project's Internal rate of return (IRR) and net present value (NPV) are. Assume that the net working capital will not require flotation costs. (Enter your NPV answer in dollars, not millions of dollars (e.... 1,234,567). Enter your IRR answer as a percent. Do not round Intermediate calculations and round your final answers to 2 decimal places (e.g.. 3216).) % IRR NPV B C D E 6 000 7 $ 8 $ Land price Current land value Land value in 5 years Plant & Equipment cost 3,500,000 4,300,000 6,400,000 30,930,000 9 $ 10 $ 11 12 . 13 0 14 15 16 Debt Bonds outstanding Years to Maturity Annual coupon rate Coupons per year Face value (% of par) Bond price (% of par) 220,000 25 7.00% 2 1,000.00 1.07 17 18 19 20 21 Common stock Shares outstanding Beta Share price 7,800,000 22 1.30 N N 23 $ 70.00 2 24 25 26 Preferred stock outstanding Shares outstanding Coupon rate Share price 27 440,000 4.00% 80.00 28 $ 29 30 31 32 Market Market risk premium Risk-free rate 6.00% 4.00% 33 34 mm m 35 36 Equity flotation cost Preferred flotation cost Debt flotation cost Tax rate Net working capital Does the NWC require flotation costs (Yes/No) 7.00% 5.00% 3.00% 40% 1,050,000 37 38 $ 39 40 no 41 42 1% 43 8 44 45 $ b. Adjustment factor c. Life of plant (years) Life of project (years) Plant salvage value d. Annual fixed costs # RDS manufactured Sale price per RDS Variable costs per RDS 46 $ 8 * * * 5 3,500,000 5,800,000 12,000 10,300 8,900 47 48 $ $ 49 50 A B C D E F G I I 34 Market value of debt Market value of equity Market value of preferred Market value of firm DIV ENV PNV Mark: weighted average flotation costs. See section 12. 11 in text book 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 a. flotation costs The cost of the land 3 years ago is a sunk cost and is irrelevant. Land Plant & Equipment Cost Net working capital Total Time o Mark: See section 12. 11. Gross up items, as appropriate, for flotation costs. b. Pretax cost of debt Aftertax cost of debt Cost of equity Cost of preferred WACC Mark: = WACC + Adjustment for Discount rate for project c. Book value in year 5 Aftertax salvage value 79 80 81 82 83 84 85 86 IN DO Mark: Gross salvage value - ((capital gain or loss) times (1 TR) 87 88 89 90 91 d. Sales Variable costs Fixed costs Depreciation EBIT Taxes Net income Depreciation Operating cash flow Mark: (fixed costs + depr) / (Sales price - variable cost) e. Accounting breakeven Year 92 93 94 95 96 97 98 99 0 Nm+ 3 Mark: 100 = OCF + NWC + NSV + after-tax value of lland 101 102 103 104 IRR NPV