Answered step by step

Verified Expert Solution

Question

1 Approved Answer

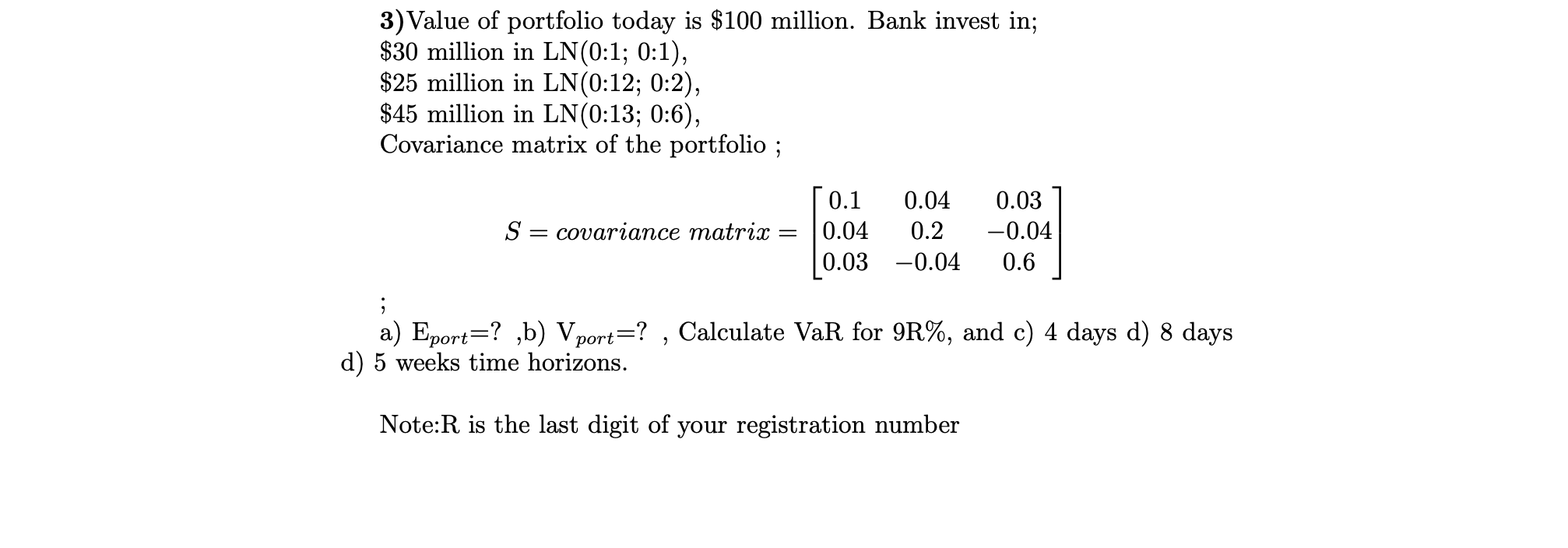

R IS: 3!!! I NEED THIS SOLUTION ASAP!! 3)Value of portfolio today is $100 million. Bank invest in; $30 million in LN(0:1; 0:1), $25 million

R IS: 3!!! I NEED THIS SOLUTION ASAP!!

R IS: 3!!! I NEED THIS SOLUTION ASAP!!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Marketing For Financial Advisors

Authors: Eric Bradlow, Keith Niedermeier, Patti Williams

1st Edition

0071605142, 978-0071605144