Answered step by step

Verified Expert Solution

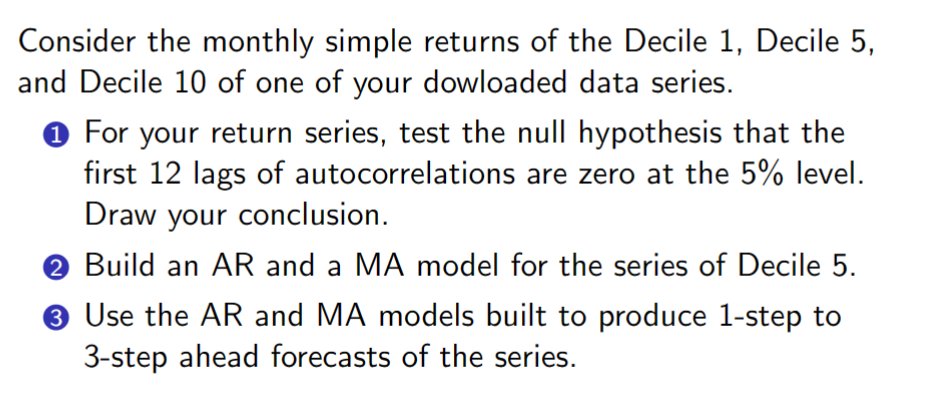

Question

1 Approved Answer

R programming language question. Where it says one of your downloaded data you can downloaded any stock's prices for a period of 5 years for

R programming language question. Where it says "one of your downloaded data" you can downloaded any stock's prices for a period of 5 years for instance.

In my effort to help as much as possible, I can say that for the autocorrelations we use the acf function. For making the deciles, we use the quantile function. But my problem is mostly with part 2 and 3. I would like the answer with explanations of the code please.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started