Answered step by step

Verified Expert Solution

Question

1 Approved Answer

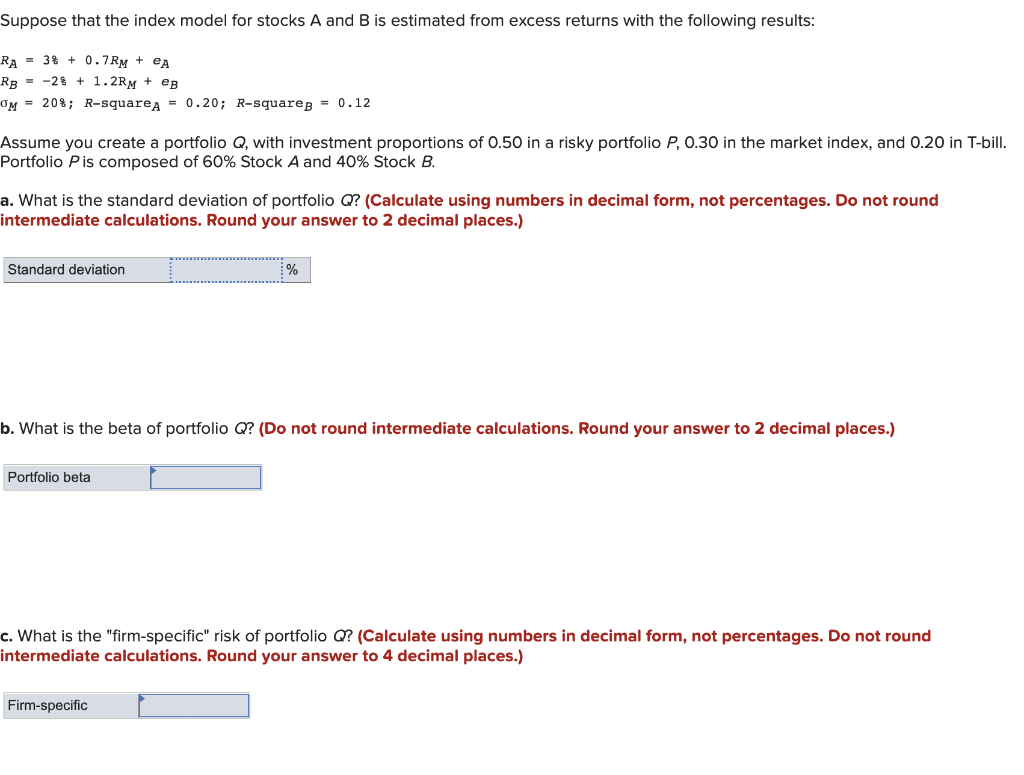

RA=3%+0.7RM+eA RB=2q+1.2RM+eB M=20; ; R-square A=0.20;R-square B=0.12 Assume you create a portfolio Q, with investment proportions of 0.50 in a risky portfolio P,0.30 in the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Making Sense Of School Finance

Authors: Clinton Born

1st Edition

1475856652, 978-1475856651