Answered step by step

Verified Expert Solution

Question

1 Approved Answer

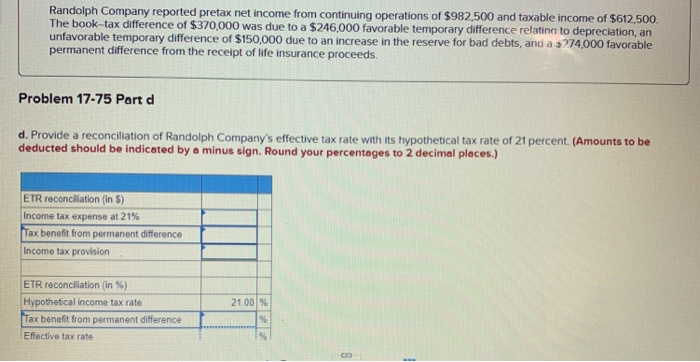

Randolph Company reported pretax net income from continuing operations of $982,500 and taxable income of $612,500. The book-tax difference of $370,000 was due to a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Sustainability Of Public Sector EntitiesThe Relevance Of Accounting Frameworks

Authors: Josette Caruana, Isabel Brusca, Eugenio Caperchione, Sandra Cohen, Francesca Manes Rossi

1st Edition

3030060365, 9783030060367