| RATIO ANALYSIS |

| Item Name | Formula | | | Company Data Used | Answer |

| 2. Audit report: What was the audit opinion? | | | | | (Yes/No) |

| 3. Audit report: Was there a going concern issue? | | | | | (Yes/No) |

| 4. Audit report: Any other serious issues? | If yes, list the other concerns auditors had about the company's financial statements | (Yes/No) |

| | | | | | |

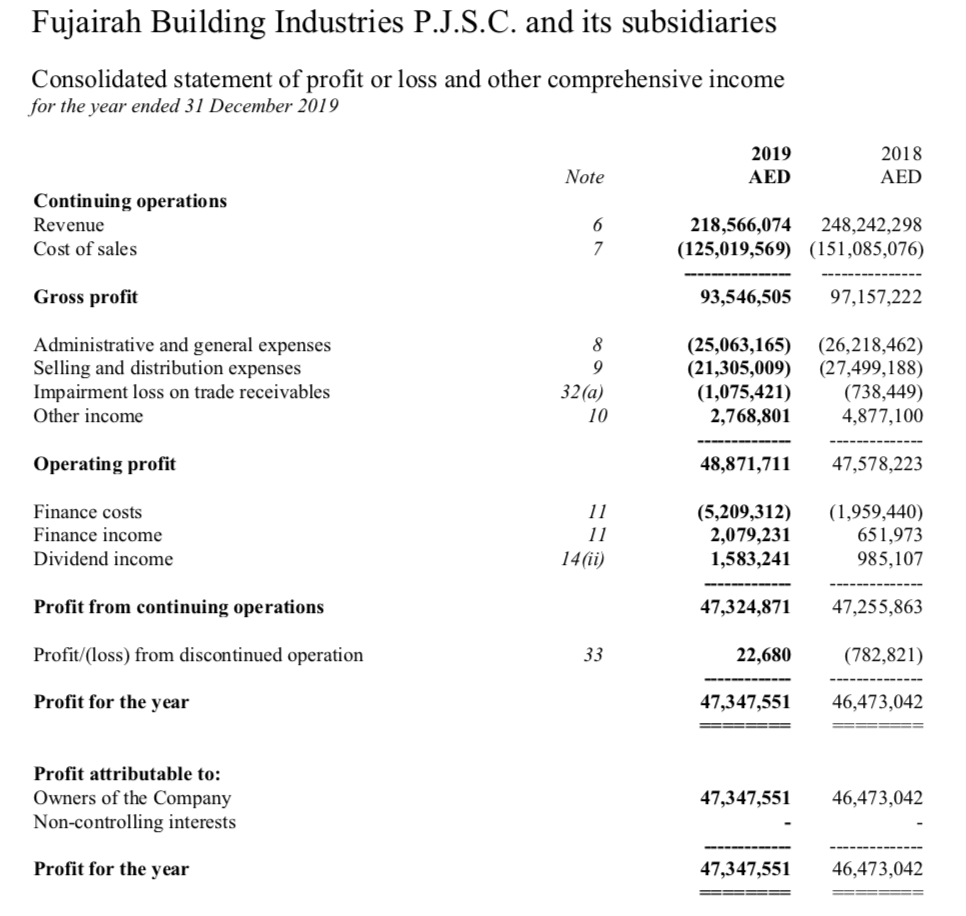

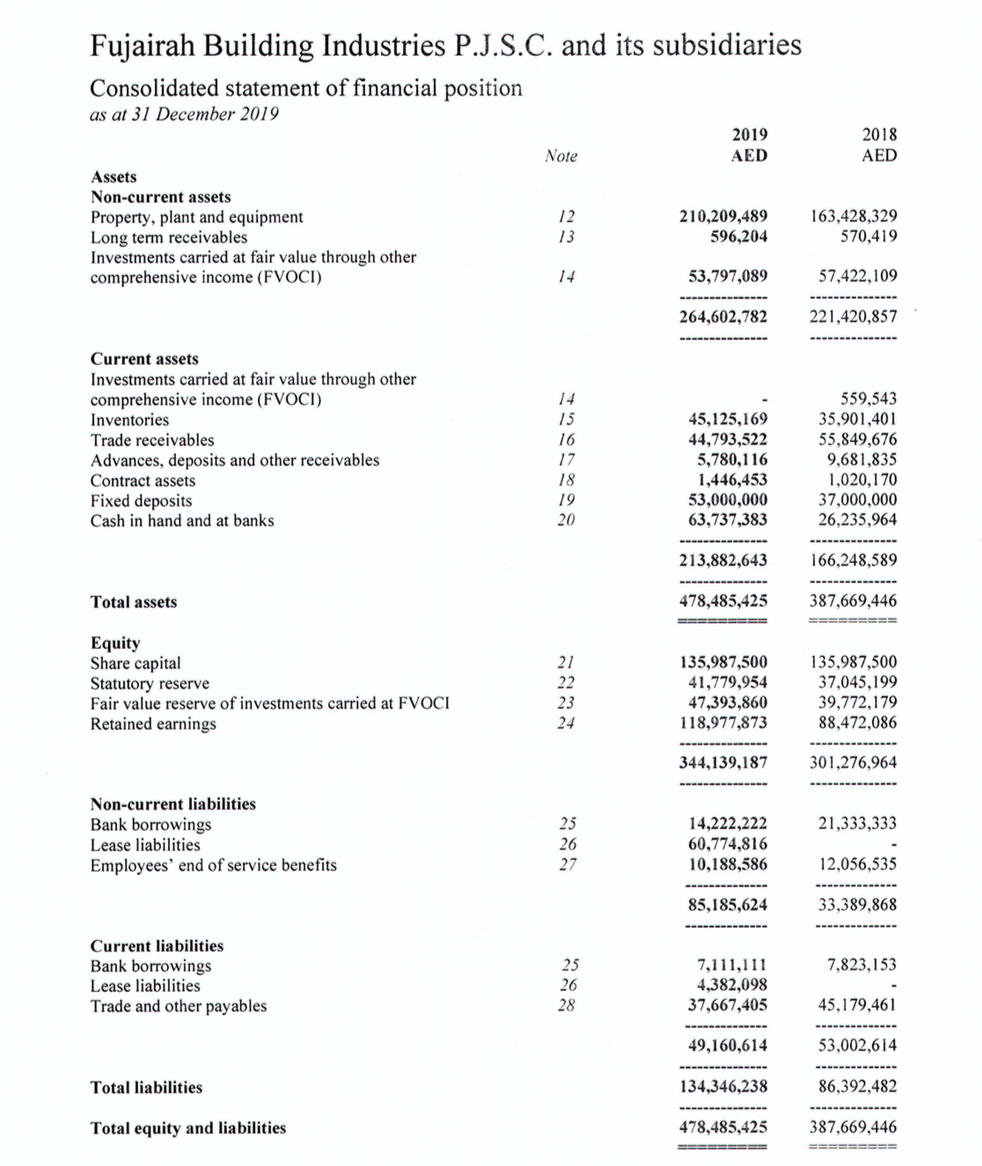

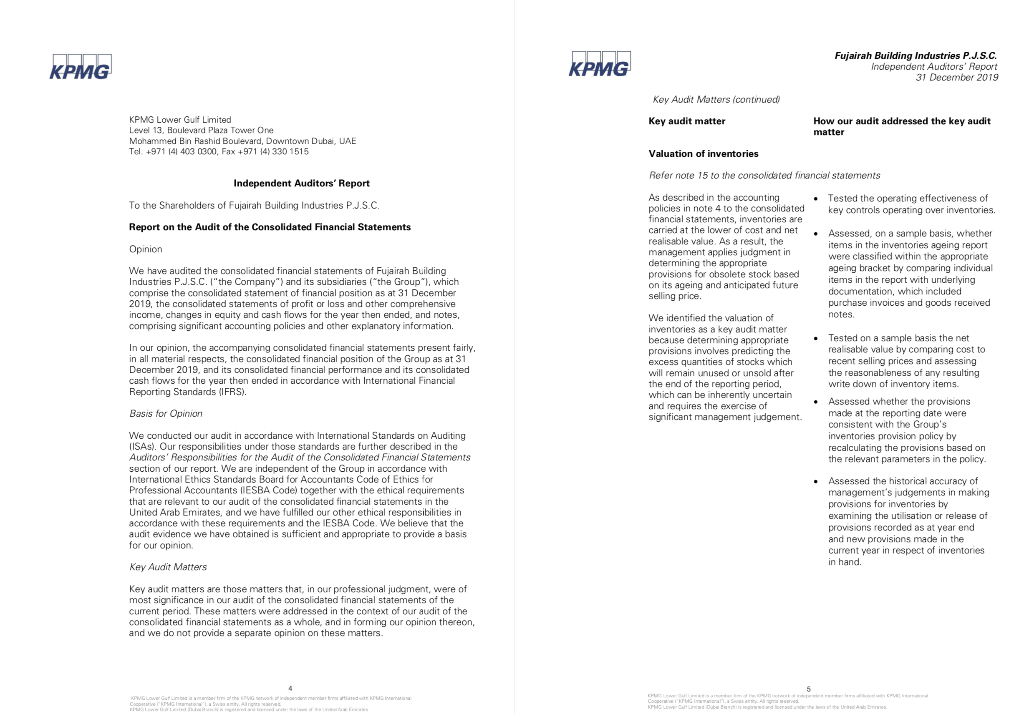

Fujairah Building Industries P.J.S.C. and its subsidiaries Consolidated statement of profit or loss and other comprehensive income for the year ended 31 December 2019 2019 AED 2018 AED Note Continuing operations Revenue Cost of sales 6 7 218,566,074 248,242,298 (125,019,569) (151,085,076) Gross profit 93,546,505 97,157,222 Administrative and general expenses Selling and distribution expenses Impairment loss on trade receivables Other income 8 9 32(a) 10 (25,063,165) (21,305,009) (1,075,421) 2,768,801 (26,218,462) (27,499,188) (738,449) 4,877,100 Operating profit 48,871,711 47,578,223 Finance costs Finance income Dividend income 11 11 14 (ii) (5,209,312) 2,079,231 1,583,241 (1,959,440) 651,973 985,107 Profit from continuing operations 47,324,871 47,255,863 Profit/(loss) from discontinued operation 33 22,680 (782,821) Profit for the year 47,347,551 46,473,042 Profit attributable to: Owners of the Company Non-controlling interests 47,347,551 46,473,042 Profit for the year 47,347,551 46,473,042 Fujairah Building Industries P.J.S.C. and its subsidiaries Consolidated statement of financial position as at 31 December 2019 2019 AED 2018 AED Note Assets Non-current assets Property, plant and equipment Long term receivables Investments carried at fair value through other comprehensive income (FVOCI) 12 13 210,209,489 596,204 163,428,329 570,419 14 53,797,089 57,422,109 264,602,782 221,420,857 Current assets Investments carried at fair value through other comprehensive income (FVOCI) Inventories Trade receivables Advances, deposits and other receivables Contract assets Fixed deposits Cash in hand and at banks 14 15 16 17 18 19 20 45,125,169 44,793,522 5,780,116 1,446,453 53,000,000 63,737,383 559,543 35,901,401 55,849,676 9,681,835 1,020,170 37,000,000 26,235,964 213,882,643 166,248,589 Total assets 478,485,425 387,669,446 Equity Share capital Statutory reserve Fair value reserve of investments carried at FVOCI Retained earnings 21 22 23 24 135,987,500 41,779,954 47,393,860 118,977,873 135,987,500 37,045,199 39,772,179 88,472,086 344,139,187 301,276,964 21,333,333 Non-current liabilities Bank borrowings Lease liabilities Employees' end of service benefits 25 26 27 14,222,222 60,774,816 10,188,586 12,056,535 85,185,624 33,389,868 7,823,153 Current liabilities Bank borrowings Lease liabilities Trade and other payables 25 26 28 7,111,111 4,382,098 37,667,405 45,179,461 49,160,614 53,002,614 Total liabilities 134,346,238 86,392,482 Total equity and liabilities 478,485,425 387,669,446 0 KPMG KPMG Fujairah Building Industries P.J.S.C. Independent Auditors' Report 31 December 2019 Key Audit Matters (continued Key audit matter KPMG Lower Gulf Limited Level 13, Boulevard Plaza Tower One Mohammed Bin Rashid Boulevard, Downtown Dubai, UAE Tel. +971 14 403 0300, Fax +971 14) 330 1515 How our audit addressed the key audit matter Valuation of inventories Independent Auditors' Report To the Shareholders of Fujairah Building Industries P.J.S.C. Report on the Audit of the Consolidated Financial Statements Opinion We have audited the consolidated financial statements of Fujairah Building Industries P.J.S.C. ("the Company") and its subsidiaries ("the Group"), which comprise the consolidated statement of financial position as at 31 December 2019, the consolidated statements of profit or loss and other comprehensive income, changes in equity and cash flows for the year then ended, and notes, comprising significant accounting policies and other explanatory information. In our opinion, the accompanying consolidated financial statements present fairly in all material respects, the consolidated financial position of the Group as at 31 December 2019, and its consolidated financial performance and its consolidated cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRS). Basis for Opinion We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditors' Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are independent of the Group in accordance with International Ethics Standards Board for Accountants Code of Ethics for Professional Accountants IESBA Code) together with the ethical requirements that are relevant to our audit of the consolidated financial statements in the United Arab Emirates, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the IESBA Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion Key Audit Matters Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. Refer note 15 to the consolidated financial statements As described in the accounting Tested the operating effectiveness of policies in note 4 to the consolidated key controls operating over inventories. financial statements, inventories are carried at the lower of cost and net Assessed, on a sample basis, whether realisable value. As a result, the items in the inventories ageing report management applies judgment in were classified within the appropriate determining the appropriate provisions for obsolete stock based ageing bracket by comparing individual items in the report with underlying on its ageing and anticipated future selling price documentation, which included purchase invoices and goods received We identified the valuation of notes inventories as a key audit matter because determining appropriate Tested on a sample basis the net provisions involves predicting the realisable value by comparing cost to excess quantities of stocks which recent selling prices and assessing will remain unused or unsold after the reasonableness of any resulting the end of the reporting period, write down of inventory items. which can be inherently uncertain and requires the exercise of Assessed whether the provisions significant management judgement. made at the reporting date were consistent with the Group's inventories provision policy by recalculating the provisions based on the relevant parameters in the policy. Assessed the historical accuracy of management's judgements in making provisions for inventories by examining the utilisation or release of provisions recorded as at year end and new provisions made in the Current year in respect of inventories in hand MGLOW Godle rethe Videoer fra andra Coco Now. All rights COM SA TULEWO KPMG Fujairah Building Industries P.J.S.C. Independent Auditors' Report 31 December 2019 KPMG Fujairah Building Industries P.J.S.C. Independent Auditors' Report 31 December 2019 Other matter Key Audit Matters (continued) Key audit matter How our audit addressed the key audit matter The consolidated financial statements of the Group as at and for the year ended 31 December 2018, were audited by another auditor who expressed an unmodified opinion on those consolidated financial statements on 13 February 2019. Expected credit loss on trade receivables Other Information Management is responsible for the other information. The other information comprises the information included in the Director's report. Our opinion on the consolidated financial statements does not cover the other information and we do not express any form of assurance conclusion thereon Refer note 32 to the consolidated financial statements: As described in the accounting Obtained an understanding of the policies in note 4 to the Group's methodology for estimating consolidated financial statements, ECL and assessed the appropriateness impairment of trade receivables is of the ECL methodology against the determined through expected requirements of IFRS 9 credit loss (ECL) model. Assessed management's expected Trade receivables comprise 9% of credit losses model by reviewing the Group's total assets at 31 management's analysis of historical December 2019 and involves credit losses of its receivables, testing significant estimates and the completeness and accuracy of data judgements for the determination inputs in the model and evaluating the of expected credit loss on trade forward looking overlay applied receivables. Tested key inputs of the model, such as those used to calculate the likelihood of default and the subsequent loss on default, by comparing to historical data. We also assessed the reasonableness of forward looking factors used by the Group In connection with our audit of the consolidated financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the consolidated financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard. Responsibilities of Management and Those Charged with Governance for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with IFRS and their preparation in compliance with the applicable provisions of the UAE Federal Law No. (2) of 2015, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error, In preparing the consolidated financial statements, management is responsible for assessing the Group's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so. Those charged with governance are responsible for overseeing the Group's financial reporting process Reviewed arrangements and/or correspondences with external parties to assess the recoverability of significant overdue outstanding receivables 7 KPW Lour Guild a method model GVG Lw Guitamente permend KPMG KPMG Fujairah Building Industries P.J.S.C. Independent Auditors' Report 31 December 2019 KPMG Fujairah Building Industries P.J.S.C. Independent Auctors' Report 31 December 2019 Auditor's Responsibilities for the Audit of the Consolidated Financial Statements (continued) We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings including any significant deficiencies in internal control that we identify during our audit We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards. From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the consolidated financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditors' report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication. Auditor's Responsibilities for the Audit of the Consolidated Financial Statements Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements. As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also: Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group's internal control. Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group's ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors' report. However, future events or conditions may cause the Group to cease to continue as a going concern Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion. Report on Other Legal and Regulatory Requirements Further, as required by the UAE Federal Law No. (2) of 2015, we report that: : i) we have obtained all the information and explanations we considered necessary for the purposes of our audit; ii) the consolidated financial statements have been prepared and comply, in all material respects, with the applicable provisions of the UAE Federal Law No. (2) of 2015 ii) the Group has maintained proper books of account: iv) the financial information included in the Directors' report, in so far as it relates to these consolidated financial statements, is consistent with the books of account of the Group: v) as disclosed in note 37 to the consolidated financial statements, the Group has not purchased any shares during the year ended 31 December 2019: 8 CVG Lower Gmber the CVG Sport medias 9 VG LWG that percent amb KPMG Fujairah Building Industries P.J.S.C. Independent Auditors' Report 31 December 2019 Report on Other Legal and Regulatory Requirements (continued) vi) note 30 to the consolidated financial statements discloses material related party transactions and the terms under which they were conducted; vii) based on the information that has been made available to us, nothing has come to our attention which causes us to believe that the Group has contravened during the financial year ended 31 December 2019 any of the applicable provisions of the UAE Federal Law No. (2) of 2015 or in respect of the Company, its Articles of Association, which would materially affect its activities or its consolidated financial position as at 31 December 2019, and viii) note 8 to the consolidated financial statements discloses the social contributions made during the year. KPMG Lower Gulf Limited Fawzi Abu Rass Registration No. 968 Dubai, United Arab Emirates Date: 0 MAR 2970 10 KPMG Lower Curta member of the work of members with KPNG ter Cooperative Final Sitty Allights KPMG Low Galege ce rows of the United Arab Emrates