2. Reconcile the absorption costing EBIT and the variable costing EBIT figures for each year by computing the deferred/released fixed overhead for each year and

2. Reconcile the absorption costing EBIT and the variable costing EBIT figures for each year by computing the deferred/released fixed overhead for each year and applying the proper adjustments.

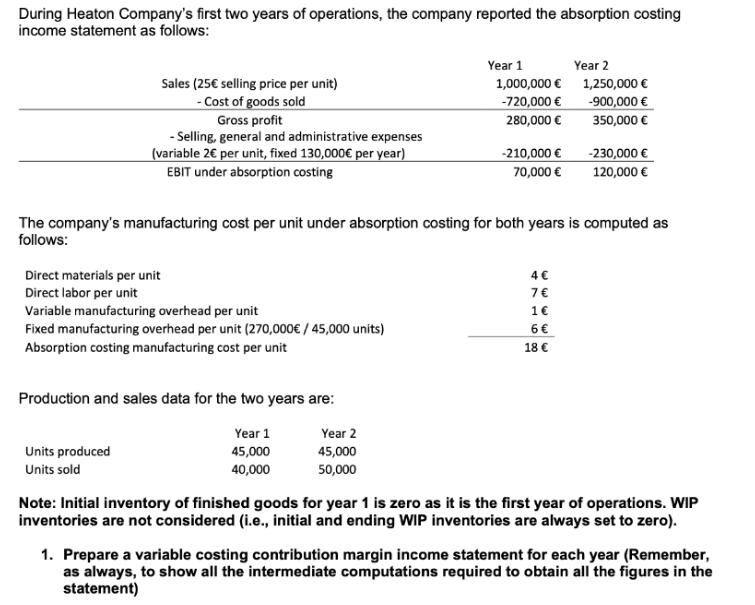

During Heaton Company's first two years of operations, the company reported the absorption costing income statement as follows: Sales (25 selling price per unit) -Cost of goods sold Gross profit -Selling, general and administrative expenses (variable 2 per unit, fixed 130,000 per year) EBIT under absorption costing Direct materials per unit Direct labor per unit Variable manufacturing overhead per unit Fixed manufacturing overhead per unit (270,000 / 45,000 units) Absorption costing manufacturing cost per unit Production and sales data for the two years are: Year 1 45,000 40,000 Units produced Units sold Year 1 Year 2 45,000 50,000 1,000,000 -720,000 280,000 -210,000 70,000 The company's manufacturing cost per unit under absorption costing for both years is computed as follows: 4 7 Year 2 1 6 18 1,250,000 -900,000 350,000 -230,000 120,000 Note: Initial inventory of finished goods for year 1 is zero as it is the first year of operations. WIP inventories are not considered (i.e., initial and ending WIP inventories are always set to zero). 1. Prepare a variable costing contribution margin income statement for each year (Remember, as always, to show all the intermediate computations required to obtain all the figures in the statement)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

1 Income statement using variable costing Contribution margin Income Statement Variable costing Year ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Alvin a. arens, Randal j. elder, Mark s. Beasley

14th Edition

133081605, 132575957, 9780133081602, 978-0132575959