Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Read below and answer, Why does a business that has profit of $30,000 per year need a bank loan? Jones Electrical Distribution After several years

Read below and answer, Why does a business that has profit of $30,000 per year need a bank loan?

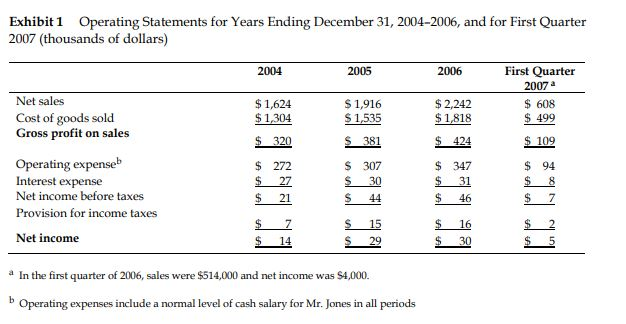

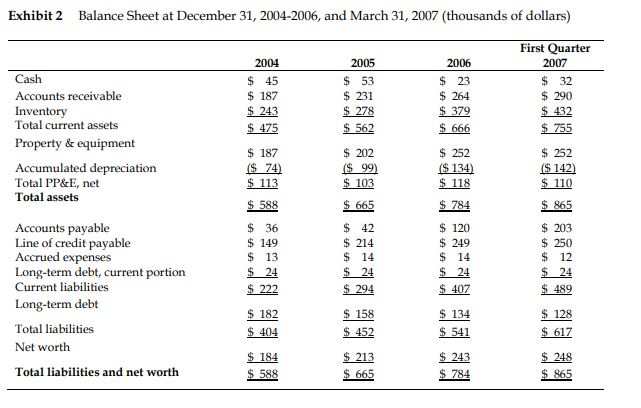

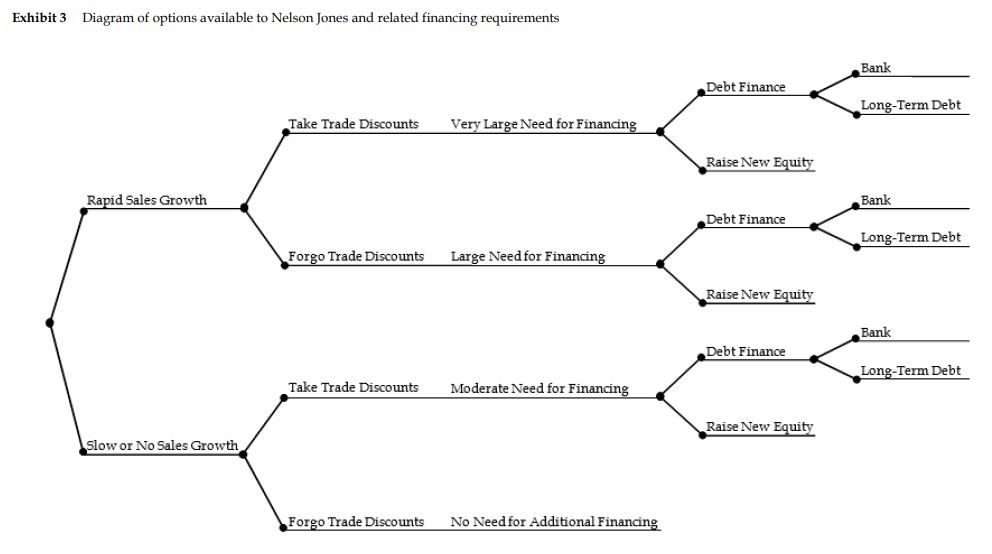

Jones Electrical Distribution After several years of rapid growth, in the spring of 2007 Jones Electrical Distribution anticipated a further substantial increase in sales. Despite good profits, the company had experienced a shortage of cash and had found it necessary to increase its borrowing from Metropolitan Bank-a local one- branch bank-to $250,000 in 2006. The maximum loan that Metropolitan would make to any one borrower was $250,000, and Jones had been able to stay within the limit only by relying very heavily on trade credit from the manufacturers from whom Jones purchased the electrical products it sold to its customers. Nelson Jones, sole owner and president of the company, was therefore looking elsewhere for a new banking relationship that would allow him to negotiate a larger loan. Jim Lyons, a homebuilder who was a friend of Jones, introduced Jones to Rachel Montrose, Lyons's relationship officer at the local branch of Southern Bank & Trust-a large, regional bank. Southern had a 7-year relationship with Lyons, including a current loan balance of over $3 million. Jones and Montrose tentatively discussed the possibility that Southern might extend a line of credit to Jones up to a maximum amount of $350,000. Jones thought that a loan of this size would more than meet his needs for at least the next year, and he was eager for the flexibility that a line of credit of this size would provide. After discussion, Montrose had arranged for the credit department of Southern Bank & Trust to investigate Nelson Jones and his company. Background of Jones Electrical Distribution Jones Electrical Distribution was founded in 1999 as a partnership between Nelson Jones and his college roommate, Dave Verden. In 2003, Jones and Verden had a disagreement on how aggressively they should grow the business, and Jones ultimately bought Verden out for $250,000. They agreed that Jones would pay Verden the $250,000 in installments of $2,000 per month plus interest of 8% per year. The business sold electrical components and tools to general contractors and electricians. The products, which included items such as controllers, breakers, signal devices and fuses, were purchased from nearly 100 different suppliers. Jones's customers used the products in the construction and repair of commercial and residential buildings. To a degree, Jones's sales followed the seasonality of its customers' businesses which had their highest activity during the spring and summer when weather was most conducive for construction work. The market in which Jones competed was large, fragmented, and highly competitive. Jones faced significant competition from national distributors, home centers, and other small supply houses. In spite of the competition, Jones had built up sales volume by successfully competing on price and employing an aggressive direct sales force who often visited customers at their job sites. In order to compete on price, Jones maintained tight control over operating expenses, including paying his salesforce primarily on commission and keeping overhead to a minimum. In addition, as part of his expense management effort, Jones had historically paid his suppliers within 10 days of the invoice date in order to take full advantage of the 2% discounts they offered for quick payments. Jones had also proved adept at demand forecasting and inventory management, allowing him to satisfy his customers' demand with a modest amount of inventory relative to his larger competitors. Jones's focus and dedication to his business allowed him to build it into a profitable operation. Jones Electrical Distribution had grown to $2.24 million in sales and $30,000 of net income in 2006. Operating statements for years 2004-2006 and for the three months ending March 31, 2007, are given in Exhibit 1. Financing the Business Through Southern Bank & Trust To solve his financing need, Jones wanted to develop a relationship with a larger bank that would not run into issues with maximum loans to a single borrower as he had experienced with Metropolitan Bank. He wanted to build a relationship with a bank that could grow with him, including to more locations if he decided to add additional sites in the future. As part of its customary due diligence of Jones Electrical Distribution, the Southern Bank & Trust's credit department asked Jones's friend Jim Lyons for a reference on Jones. Lyons's reference included the following comments: "Nelson is a businessman of the highest integrity and sharp acumen who is a very hands-on manager of his operation. He has excellent knowledge of the products he sells and provides customers with excellent service. He also lives a modest lifestyle." The bank also toured Jones Electrical Distribution's warehouse and office and interviewed the area sales managers for three of the manufacturers from whom Jones bought the products he sold. The managers were unanimous in their favorable opinion of Jones. One of them said: "Nelson has been one of our best performing wholesalers. He really knows how to build relationships and close a sale. He has also been great with his expense management. The guy does not spend a dime unless he absolutely has to. We look forward to building a bigger relationship with him in the future." In addition to the electrical distribution business, which was Jones's only source of income, Jones held jointly with his wife an equity in their home. The house had cost $199,000 to build in 1999 and was mortgaged for $117,000. He also held a $250,000 life insurance policy, payable to his wife. Otherwise, they had no sizeable personal investments. Southern Bank & Trust gave particular attention to the debt position and current ratio of the business. It noted the ready market for the company's products at all times and the fact that sales prospects were favorable. The bank's investigator reported: "Sales are expected to reach $2.7 million by the end of 2007." On the other hand, it was recognized that a general economic downturn might slow down the rate of increase in sales. Projections beyond 2007 were difficult to make, but the prospects appeared good for continued growth in the volume of Jones Electrical Distribution's business over the foreseeable future. The bank also noted the rapid increase in Jones Electrical's accounts payable and line of credit in the recent past. Jones Electrical's main suppliers had terms of 30 days net and provided a 2% discount for payments made within 10 days of invoice date. These terms notwithstanding, the manufacturers did not object if payments lagged somewhat behind the due date. During the past six months, Jones had taken very few purchase discounts because of the shortage of funds arising from the additional investments in working capital associated with the company's increased sales volume. Balance sheets at December 31, 2004-2006, and March 31, 2007, are presented in Exhibit 2. The tentative discussions between Rachel Montrose and Nelson Jones had been about a revolving, secured line of credit not to exceed $350,000. The specific details of the loan had not been worked out, but Montrose had explained the agreement would involve the standard covenants applying to such a loan. She cited as illustrative provisions the requirement that restrictions on additional borrowing would be imposed, that additional investments in fixed assets could be made only with prior approval of the bank, and that limitations would be placed on withdrawals of funds from the business by Jones. She also indicated that while the line of credit would have a limit of $350,000, Jones's utilization of the line at any point in time would be limited to an amount equal to 75% of Accounts Receivable and 50% of Inventory. Interest would be set on a floating-rate basis at 1.5% percentage points above the prime rate (the rate paid by the bank's most creditworthy customers). Montrose indicated that the initial rate to be paid would be about 7.5% under conditions in effect in early 2007. Jones also understood that he would be required to sever his relationship with Metropolitan Bank if he entered into a loan agreement with Southern Bank & Trust. The Future of Jones Electrical Distribution As he contemplated his next meeting with Montrose, Jones's thoughts were dominated by the immediate need for more bank credit. However, he knew that the increasingly tense relationships with his suppliers and the seemingly unending need for more financing meant that he needed to be more deliberate about his future growth plans. To get started, he grabbed a blank piece of paper from his office printer and sketched out the options before him. He started with the pace of sales growth followed by his taking the 2% discounts-or not-which led into the financing implications of each alternative. See Exhibit 3 for the diagram of the alternatives as Jones saw them. Jones promised himself that he would not only close the new bank deal but he would then determine the right long-term growth path for the company he worked so hard to grow over the past seven years. Exhibit 1 Operating Statements for Years Ending December 31, 2004-2006, and for First Quarter 2007 (thousands of dollars) 2004 2005 2006 First Quarter 2007 a $ 608 $ 499 Net sales Cost of goods sold Gross profit on sales $1,624 $ 1,304 $ 1,916 $ 1,535 $381 $ 109 $ 94 Operating expense Interest expense Net income before taxes Provision for income taxes $ $ $ $ $ $ 320 272 27 21 7 14 $ $ $ $ $ $2,242 $1,818 $ 424 $ 347 $_31 $ 46 $ 16 $ 30 307 30 44 15 29 In hel Net income In the first quarter of 2006, sales were $514,000 and net income was $4,000. Operating expenses include a normal level of cash salary for Mr. Jones in all periods Exhibit 2 Balance Sheet at December 31, 2004-2006, and March 31, 2007 (thousands of dollars) Cash Accounts receivable Inventory Total current assets Property & equipment 2004 $ 45 $ 187 $ 243 $ 475 $ 187 ($ 74) $ 113 2005 $ 53 $ 231 $ 278 $ 562 $ 202 ($ 99) $ 103 $ 665 2006 $ 23 $ 264 $ 379 $ 666 First Quarter 2007 $ 32 $ 290 $ 432 $ 755 Accumulated depreciation Total PP&E, net Total assets $ 252 ($ 134) $ 118 $ 252 ($ 142) $ 110 $ 588 $ 784 $ 865 $ 42 Accounts payable Line of credit payable Accrued expenses Long-term debt, current portion Current liabilities Long-term debt $ 36 $ 149 $ 13 $ 24 $ 222 $ 203 $ 250 $ 12 $24 $ 120 $ 249 $ 14 $ 24 $ 407 $ 134 $ 541 $ 243 $ 784 $ 214 $ 14 $ 24 $ 294 $ 158 $ 452 $ 213 $ 665 $ 489 $ 128 $ 182 Total liabilities Net worth $ 617 $ 404 $ 184 $ 588 Total liabilities and net worth $ 248 $ 865 Exhibit 3 Diagram of options available to Nelson Jones and related financing requirements Bank Debt Finance Long-Term Debt Take Trade Discounts Very Large Need for Financing Raise New Equity Rapid Sales Growth Bank Debt Finance Long-Term Debt Forgo Trade Discounts Large Need for Financing Raise New Equity Bank Debt Finance Long-Term Debt Take Trade Discounts Moderate Need for Financing Raise New Equity Slow or No Sales Growth Forgo Trade Discounts No Need for Additional Financing

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: John Stittle, Robert Wearing

1st Edition

1412935024, 9781412935029