Read the attached Term Sheet Negotiations. case study and compare the two term sheets.

Provide detailed answers to the following question:

- Does it make a difference to your answers whether you expect Trendsetter.com to grow fast or grow slowly?

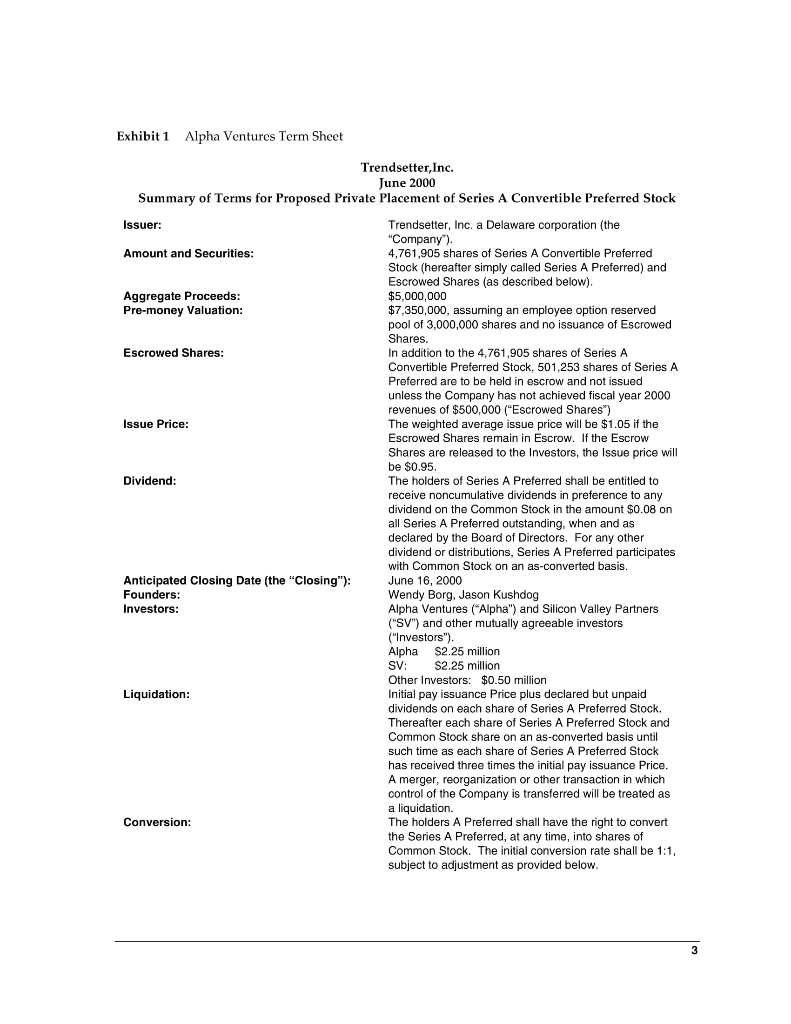

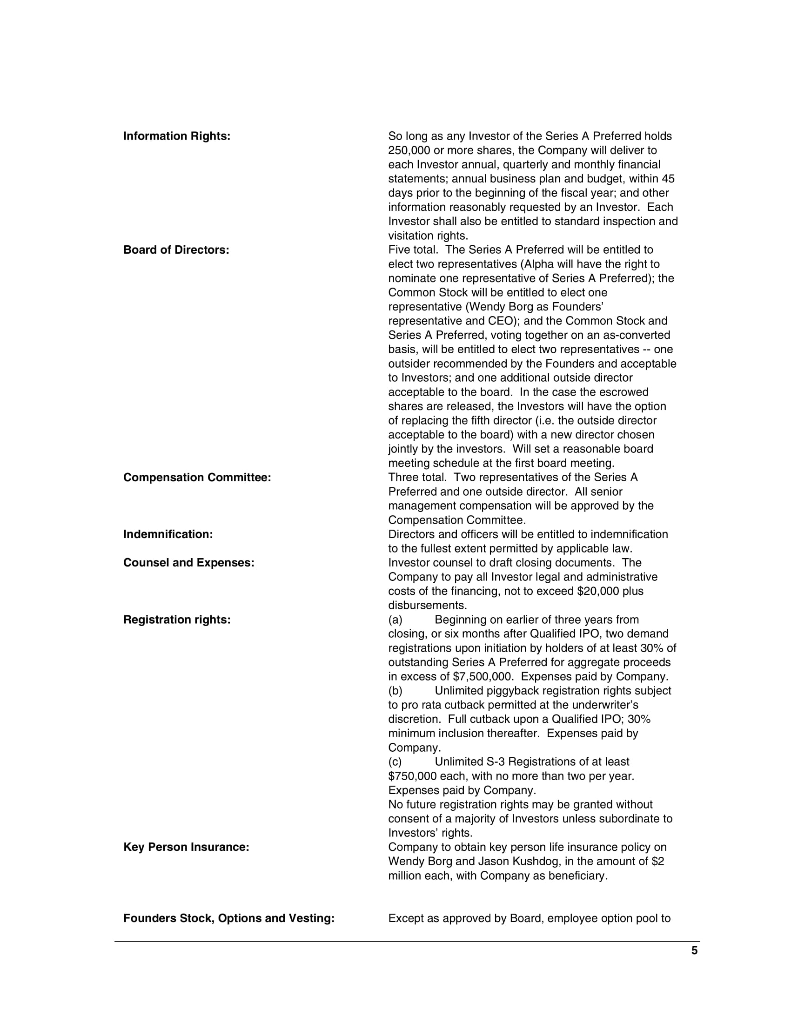

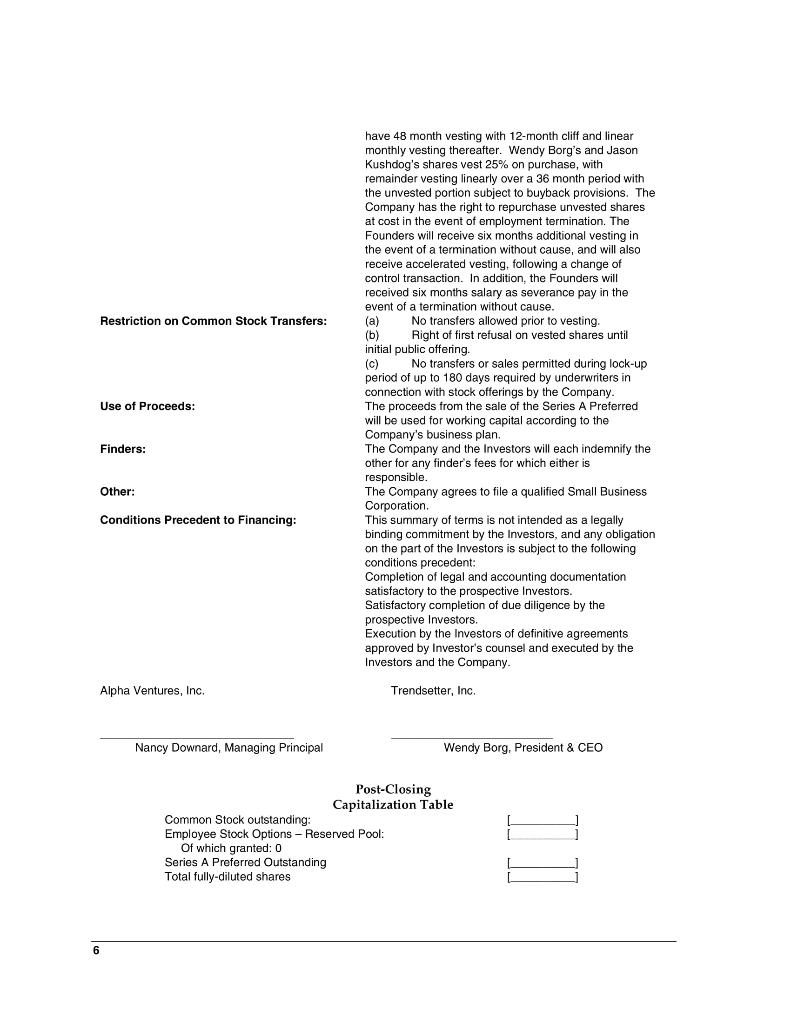

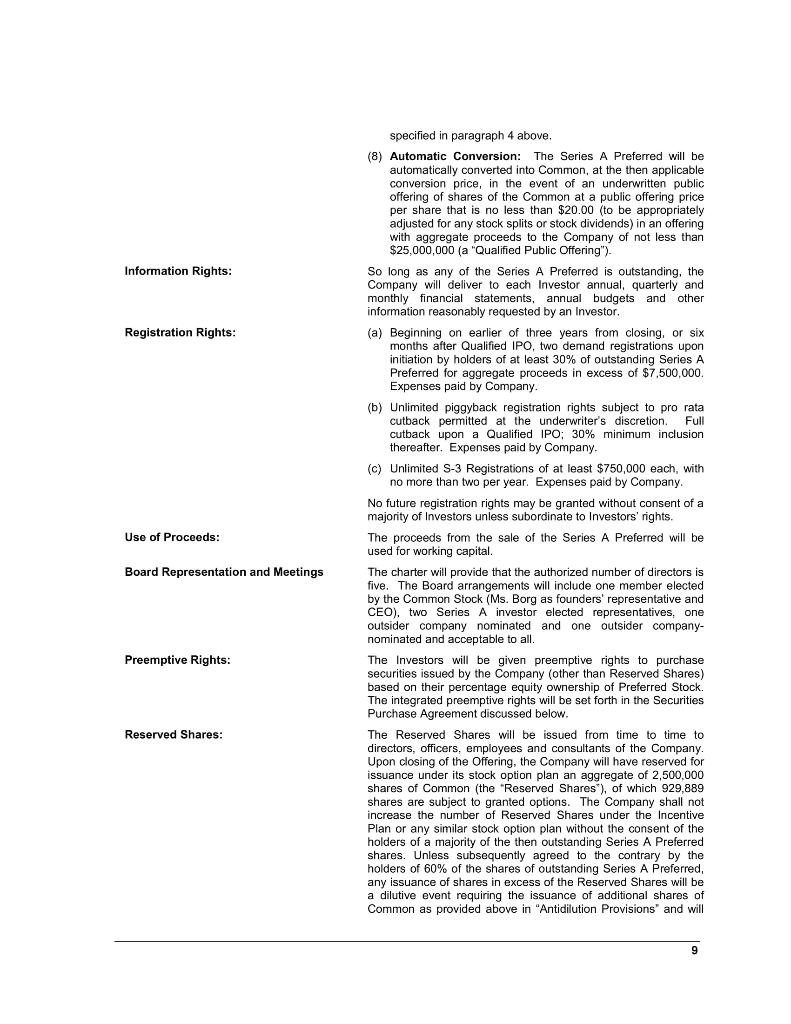

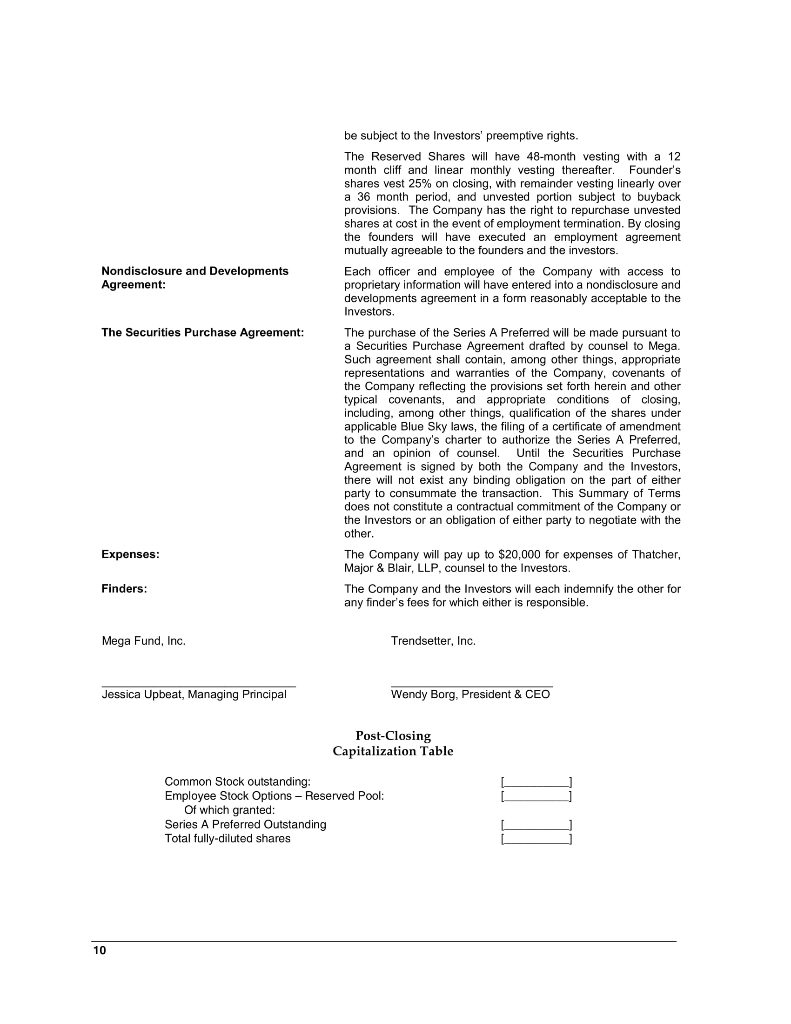

801-358 Term Sheet Negotiations for Trendsetter, Inc. At first, the two operated with their own capital but knowing very well that they would need to raise outside money. Borg explained. This type of software solution will take a lot of money to develop. Also, we needed a partner firm for the development phase. Luckily, I was able to get a former client Waldo, a major fashion retailer, to commit to work with us while we were developing the product. Although we hadn't signed any contracts yet, I had a good relationship with the CEO and I was promised that we would get a signed agreement from them once we got funding. That's why we approached the VCs. Borg and Kushdog were no fools and knew that most top-tier venture capitalists received more than 2,000 unsolicited business plans per year. In most of these venture capital firms all 2000 plans made it straight into the garbage can - without receiving any consideration. Experience had shown VCs that it was not worth their time to look for needles in a haystack. Rather, VCs focused on plans that came with recommendations and endorsements (from other VCs, entrepreneurs whom the VC had previously backed, investors in the VCs' fund and from other "friends.") Fortunately, Borg and Kushdog knew two insiders who were well-connected in the venture capital community. "Our friends got us in the door at several firms," Kushdog recalled, "Once a first meeting had been arranged we knew that the ball had been teed up for us and we needed to hit it. We knew that we were on to something when our first meeting with a VC that was originally scheduled for 30 minutes ended up lasting 2 hours-and the VC did not complain." Borg and Kushdog received a lot of interest from the VC community. They presented to seven VCs. And six of them really liked the plan and the team that was in place. The process of meetings and presentations took almost two months, however. This was longer than the entrepreneurs had expected. So it was a real relief for the two when they finally received term sheets from the VCs they wanted the most: Alpha Ventures and Mega Fund. Both funds were top tier VCs and had a lot of experience in retail and software. Plus the chemistry with both firms seemed good. Borg explained: With Mega everything went smoothly. Alpha I think really liked our idea but was pretty skeptical about our ability to get a five-star client like Waldo on board early. As a result they really liked us but wanted to invest at a lower valuation than other VCs because they did not think we could book $500,000 in revenues in the first year. After a lot of talking they came around and made a fair offer. Since Borg and Kushdog thought that both VC firms, Alpha Ventures and Mega, were an equally good fit it would come down to who gave Trendsetter a better offer. Neither of the entrepreneurs had any experience in analyzing term sheets and although the top-line valuations from both VC firms were not that different the entrepreneurs knew that they had to be very careful when comparing covenants in both term sheets. "I don't like lawyers but I think we need one, now," said Kushdog as they left the restaurant. "I agree," replied Borg, "but wouldn't it be reassuring if we could figure this out on our own first?" Exhibit 1 Alpha Ventures Term Sheet Trendsetter, Inc. June 2000 Summary of Terms for Proposed Private Placement of Series A Convertible Preferred Stock Issuer: Amount and Securities: Aggregate Proceeds: Pre-money Valuation: Escrowed Shares: Issue Price: Dividend: Trendsetter, Inc. a Delaware corporation (the "Company"). 4,761,905 shares of Series A Convertible Preferred Stock (hereafter simply called Series A Preferred) and Escrowed Shares (as described below). $5,000,000 $7,350,000, assuming an employee option reserved pool of 3,000,000 shares and no issuance of Escrowed Shares. In addition to the 4,761,905 shares of Series A Convertible Preferred Stock, 501,253 shares of Series A Preferred are to be held in escrow and not issued unless the Company has not achieved fiscal year 2000 revenues of $500,000 ("Escrowed Shares) The weighted average issue price will be $1.05 if the Escrowed Shares remain in Escrow. If the Escrow Shares are released to the Investors, the Issue price will be $0.95. The holders of Series A Preferred shall be entitled to receive noncumulative dividends in preference to any dividend on the Common Stock in the amount $0.08 on all Series A Preferred outstanding, when and as declared by the Board of Directors. For any other dividend or distributions, Series A Preferred participates with Common Stock on an as-converted basis. June 16, 2000 Wendy Borg, Jason Kushdog Alpha Ventures ("Alpha") and Silicon Valley Partners ("SV") and other mutually agreeable investors ("Investors"). Alpha $2.25 million SV: S2.25 million Other Investors: $0.50 million Initial pay issuance Price plus declared but unpaid dividends on each share of Series A Preferred Stock. Thereafter each share of Series A Preferred Stock and Common Stock share on an as-converted basis until such time as each share of Series A Preferred Stock has received three times the initial pay issuance Price. A merger, reorganization or other transaction in which control of the Company is transferred will be treated as a liquidation. The holders A Preferred shall have the right to convert the Series A Preferred, at any time, into shares of Common Stock. The initial conversion rate shall be 1:1, subject to adjustment as provided below. Anticipated Closing Date (the "Closing"): Founders: Investors: Liquidation: Conversion: Automatic Conversion: Antidilution Provisions: Voting Rights: The Series A Preferred shall be automatically converted into Common Stock, at the then applicable conversion price, (i) in the event that the holders of at least a majority of the outstanding Series A Preferred consent to such conversion or (ii) upon the closing of a firmly underwritten public offering of shares of Common Stock of the Company at a per share price not less than $5.00 per share and for a total offering of not less than $15 million (before deduction of underwriters commissions an expenses) (a "Qualified IPO") The Series A Preferred shall have broad-based weighted average antidilution protection on issuances of shares. No adjustment will be made for the issuance of up to 3,000,000 shares of Common Stock (or any options for Common Stock) to employees, directors or consultants pursuant to board-approved equity incentive plans. Series A Preferred votes on an as-converted basis, but also has class vote as provided by law. Also, approval of at least 60% of Series A Preferred is required for (i) the creation or issuance of any senior or pari passu security; (ii) an increase in the number of authorized shares of Preferred Stock; (iii) any adverse change to the rights, preferences and privileges of the Preferred Stock; (iv) an increase in the size of the Board of Directors; (v) repurchase of Common Stock except upon termination of employment; (vi) repurchase or redemption of any Preferred Stock (except pursuant to redemption provisions of Articles): (vii) any transaction in which control of the Company is transferred; (viii) any amendment to the Bylaws or Articles of Incorporation; (ix) any dividend or distribution on capital stock of the Company; and (x) any sale, pledge, license or transfer of all or substantially all of the Company's assets. Standard representations and warranties from the Company, Each officer, employee and consultant of the Company will have entered into a proprietary information and inventions agreement in a form acceptable to the Investors. The Investors shall have a pro rata right, based on their percentage equity ownership of Preferred Stock, to participate in subsequent equity financings of the Company. If any shareholder of Common stock (or equivalents) wants to sell shares, he must offer them first to the holders of Series A Preferred. If a shareholder of Common or equivalent wants to transfer shares, holders of Series A Preferred have a right to participate on a pro rata basis (based on their percentage ownership of the Series A Preferred ) in the sale. This does not apply to sales in a Qualified IPO or afterward. Representations and Warranties: Nondisclosure and Development Agreements: Right of First Refusal: Co-Sale Rights: Information Rights: Board of Directors: Compensation Committee: So long as any Investor of the Series A Preferred holds 250,000 or more shares, the Company will deliver to each Investor annual, quarterly and monthly financial statements; annual business plan and budget, within 45 days prior to the beginning of the fiscal year; and other information reasonably requested by an Investor. Each Investor shall also be entitled to standard inspection and visitation rights. Five total. The Series A Preferred will be entitled to elect two representatives (Alpha will have the right to nominate one representative of Series A Preferred); the Common Stock will be entitled to elect one representative (Wendy Borg as Founders' representative and CEO); and the Common Stock and Series A Preferred, voting together on an as-converted basis, will be entitled to elect two representatives one outsider recommended by the Founders and acceptable to Investors; and one additional outside director acceptable to the board. In the case the escrowed shares are released, the Investors will have the option of replacing the fifth director (i.e. the outside director acceptable to the board) with a new director chosen jointly by the investors. Will set a reasonable board meeting schedule at the first board meeting. Three total. Two representatives of the Series A Preferred and one outside director. All senior management compensation will be approved by the Compensation Committee. Directors and officers will be entitled to indemnification to the fullest extent permitted by applicable law. Investor counsel to draft closing documents. The Company to pay all Investor legal and administrative costs of the financing, not to exceed $20,000 plus disbursements. (a) Beginning on earlier of three years from closing, or six months after Qualified IPO, two demand registrations upon initiation by holders of at least 30% of outstanding Series A Preferred for aggregate proceeds in excess of $7,500,000. Expenses paid by Company. (b) Unlimited piggyback registration rights subject to pro rata cutback permitted at the underwriter's discretion. Full cutback upon a Qualified IPO; 30% minimum inclusion thereafter. Expenses paid by Company (c) Unlimited S-3 Registrations of at least $750,000 each, with no more than two per year. Expenses paid by Company No future registration rights may be granted without consent of a majority of Investors unless subordinate to Investors' rights. Company to obtain key person life insurance policy on Wendy Borg and Jason Kushdog, in the amount of $2 million each, with Company as beneficiary. Indemnification: Counsel and Expenses: Registration rights: Key Person Insurance: Founders Stock, Options and Vesting: Except as approved by Board, employee option pool to that are outstanding or are reserved for issuance immediately after the closing of the merger and (b) have the power to elect at least two-thirds of the surviving corporation's directors) or the sale of 50% or more of the Company's assets or the acquisition in a single transaction or series of related transactions by any person or group of 50% or more of the Company's outstanding Common will be deemed to be a liquidation or winding up for purposes of the liquidation preference unless the holders of at least 70% of the then outstanding shares of Series A Preferred, voting together as a single class, elect not to treat any such event as a liquidation, dissolution or winding up. (3) Redemption: The Series A Preferred shall be redeemed at (1) a redemption price that shall equal the sum of (a) the Series A Purchase Price and (b) any declared but unpaid dividends on such shares of Series A Preferred (including the Accruing Dividends) and (l) there shall be no redemption of Series A Preferred upon an acquisition of the Company or upon a Qualified Public Offering (as hereinafter defined). If the Series A Preferred are not redeemed as required then the Investors shall have the right to designate a majority of the directors. (4) Antidilution Provisions: The Series A Preferred shall have weighted average antidilution rights on issuances of shares at a price less than 100% and greater than 50% of the Series A Purchase Price (except for the issuance of the Reserved Shares): provided if new shares are issued at a price less than or equal to 50% of the Series A Purchase Price then the adjustment will be full ratchet; provided, however, that with respect to a Designated Financing, this ratchet adjustment shall be made only if the holder of Series A Preferred invests its Pro Rata Share. A Designated Financing shall be an equity financing of at least $100,000 made on a pro rata basis (based on ownership of Common) to all Investors that is designated by the Board as a Designated Financing. Each holder's Pro Rata Share equals a portion of the Designated Financing equal to the number of shares of Common owned by such holder divided by the number of shares of Common owned by all Investors. (5) Voting Rights: The Series A Preferred will vote together with the holders of Common on an as-if converted basis on all matters presented to the stockholders. In addition to any other required vote, the Series A Preferred will be entitled to vote as a separate series as described under "Protective Provisions" below. (6) Protective Provisions: Consent of the holders of a super- majority of the Series A Preferred will be required for certain corporate actions, which actions and consent thresholds shall be agreed upon by the parties and shall be more specifically set forth in the closing documents. (7) Conversion: Each share of Series A Preferred may be converted by its holder at any time into a number of shares of Common equal to the Series A Purchase Price divided by the conversion price of the Series A Preferred. The conversion price will initially be equal to the Series A Purchase Price and will be subject to adjustment as Information Rights: Registration Rights: specified in paragraph 4 above. (8) Automatic Conversion: The Series A Preferred will be automatically converted into Common, at the then applicable conversion price, in the event of an underwritten public offering of shares of the Common at a public offering price per share that is no less than $20.00 (to be appropriately adjusted for any stock splits or stock dividends) in an offering with aggregate proceeds to the Company of not less than $25,000,000 (a "Qualified Public Offering"). So long as any of the Series A Preferred is outstanding, the Company will deliver to each Investor annual, quarterly and monthly financial statements, annual budgets and other information reasonably requested by an Investor (a) Beginning on earlier of three years from closing, or six months after Qualified IPO, two demand registrations upon initiation by holders of at least 30% of outstanding Series A Preferred for aggregate proceeds in excess of $7,500,000 Expenses paid by Company. (b) Unlimited piggyback registration rights subject to pro rata cutback permitted at the underwriter's discretion. Full cutback upon a Qualified IPO; 30% minimum inclusion thereafter. Expenses paid by Company. (c) Unlimited S-3 Registrations of at least $750,000 each, with no more than two per year. Expenses paid by Company. No future registration rights may be granted without consent of a majority of Investors unless subordinate to Investors' rights. The proceeds from the sale of the Series A Preferred will be used for working capital. The charter will provide that the authorized number of directors is five. The Board arrangements will include one member elected by the Common Stock (Ms. Borg as founders' representative and CEO). two Series A investor elected representatives, one outsider company nominated and one outsider company- nominated and acceptable to all. Use of Proceeds: Board Representation and Meetings Preemptive Rights: Reserved Shares: The Investors will be given preemptive rights to purchase securities issued by the Company (other than Reserved Shares) based on their percentage equity ownership of Preferred Stock. The integrated preemptive rights will be set forth in the Securities Purchase Agreement discussed below. The Reserved Shares will be issued from time to time to directors, officers, employees and consultants of the Company Upon closing of the Offering, the Company will have reserved for issuance under its stock option plan an aggregate of 2,500,000 shares of Common (the "Reserved Shares), of which 929,889 shares are subject to granted options. The Company shall not increase the number of Reserved Shares under the Incentive Plan or any similar stock option plan without the consent of the holders of a majority of the then outstanding Series A Preferred shares. Unless subsequently agreed to the contrary by the holders of 60% of the shares of outstanding Series A Preferred, any issuance of shares in excess of the Reserved Shares will be a dilutive event requiring the issuance of additional shares of Common as provided above in "Antidilution Provisions and will 801-358 Term Sheet Negotiations for Trendsetter, Inc. At first, the two operated with their own capital but knowing very well that they would need to raise outside money. Borg explained. This type of software solution will take a lot of money to develop. Also, we needed a partner firm for the development phase. Luckily, I was able to get a former client Waldo, a major fashion retailer, to commit to work with us while we were developing the product. Although we hadn't signed any contracts yet, I had a good relationship with the CEO and I was promised that we would get a signed agreement from them once we got funding. That's why we approached the VCs. Borg and Kushdog were no fools and knew that most top-tier venture capitalists received more than 2,000 unsolicited business plans per year. In most of these venture capital firms all 2000 plans made it straight into the garbage can - without receiving any consideration. Experience had shown VCs that it was not worth their time to look for needles in a haystack. Rather, VCs focused on plans that came with recommendations and endorsements (from other VCs, entrepreneurs whom the VC had previously backed, investors in the VCs' fund and from other "friends.") Fortunately, Borg and Kushdog knew two insiders who were well-connected in the venture capital community. "Our friends got us in the door at several firms," Kushdog recalled, "Once a first meeting had been arranged we knew that the ball had been teed up for us and we needed to hit it. We knew that we were on to something when our first meeting with a VC that was originally scheduled for 30 minutes ended up lasting 2 hours-and the VC did not complain." Borg and Kushdog received a lot of interest from the VC community. They presented to seven VCs. And six of them really liked the plan and the team that was in place. The process of meetings and presentations took almost two months, however. This was longer than the entrepreneurs had expected. So it was a real relief for the two when they finally received term sheets from the VCs they wanted the most: Alpha Ventures and Mega Fund. Both funds were top tier VCs and had a lot of experience in retail and software. Plus the chemistry with both firms seemed good. Borg explained: With Mega everything went smoothly. Alpha I think really liked our idea but was pretty skeptical about our ability to get a five-star client like Waldo on board early. As a result they really liked us but wanted to invest at a lower valuation than other VCs because they did not think we could book $500,000 in revenues in the first year. After a lot of talking they came around and made a fair offer. Since Borg and Kushdog thought that both VC firms, Alpha Ventures and Mega, were an equally good fit it would come down to who gave Trendsetter a better offer. Neither of the entrepreneurs had any experience in analyzing term sheets and although the top-line valuations from both VC firms were not that different the entrepreneurs knew that they had to be very careful when comparing covenants in both term sheets. "I don't like lawyers but I think we need one, now," said Kushdog as they left the restaurant. "I agree," replied Borg, "but wouldn't it be reassuring if we could figure this out on our own first?" Exhibit 1 Alpha Ventures Term Sheet Trendsetter, Inc. June 2000 Summary of Terms for Proposed Private Placement of Series A Convertible Preferred Stock Issuer: Amount and Securities: Aggregate Proceeds: Pre-money Valuation: Escrowed Shares: Issue Price: Dividend: Trendsetter, Inc. a Delaware corporation (the "Company"). 4,761,905 shares of Series A Convertible Preferred Stock (hereafter simply called Series A Preferred) and Escrowed Shares (as described below). $5,000,000 $7,350,000, assuming an employee option reserved pool of 3,000,000 shares and no issuance of Escrowed Shares. In addition to the 4,761,905 shares of Series A Convertible Preferred Stock, 501,253 shares of Series A Preferred are to be held in escrow and not issued unless the Company has not achieved fiscal year 2000 revenues of $500,000 ("Escrowed Shares) The weighted average issue price will be $1.05 if the Escrowed Shares remain in Escrow. If the Escrow Shares are released to the Investors, the Issue price will be $0.95. The holders of Series A Preferred shall be entitled to receive noncumulative dividends in preference to any dividend on the Common Stock in the amount $0.08 on all Series A Preferred outstanding, when and as declared by the Board of Directors. For any other dividend or distributions, Series A Preferred participates with Common Stock on an as-converted basis. June 16, 2000 Wendy Borg, Jason Kushdog Alpha Ventures ("Alpha") and Silicon Valley Partners ("SV") and other mutually agreeable investors ("Investors"). Alpha $2.25 million SV: S2.25 million Other Investors: $0.50 million Initial pay issuance Price plus declared but unpaid dividends on each share of Series A Preferred Stock. Thereafter each share of Series A Preferred Stock and Common Stock share on an as-converted basis until such time as each share of Series A Preferred Stock has received three times the initial pay issuance Price. A merger, reorganization or other transaction in which control of the Company is transferred will be treated as a liquidation. The holders A Preferred shall have the right to convert the Series A Preferred, at any time, into shares of Common Stock. The initial conversion rate shall be 1:1, subject to adjustment as provided below. Anticipated Closing Date (the "Closing"): Founders: Investors: Liquidation: Conversion: Automatic Conversion: Antidilution Provisions: Voting Rights: The Series A Preferred shall be automatically converted into Common Stock, at the then applicable conversion price, (i) in the event that the holders of at least a majority of the outstanding Series A Preferred consent to such conversion or (ii) upon the closing of a firmly underwritten public offering of shares of Common Stock of the Company at a per share price not less than $5.00 per share and for a total offering of not less than $15 million (before deduction of underwriters commissions an expenses) (a "Qualified IPO") The Series A Preferred shall have broad-based weighted average antidilution protection on issuances of shares. No adjustment will be made for the issuance of up to 3,000,000 shares of Common Stock (or any options for Common Stock) to employees, directors or consultants pursuant to board-approved equity incentive plans. Series A Preferred votes on an as-converted basis, but also has class vote as provided by law. Also, approval of at least 60% of Series A Preferred is required for (i) the creation or issuance of any senior or pari passu security; (ii) an increase in the number of authorized shares of Preferred Stock; (iii) any adverse change to the rights, preferences and privileges of the Preferred Stock; (iv) an increase in the size of the Board of Directors; (v) repurchase of Common Stock except upon termination of employment; (vi) repurchase or redemption of any Preferred Stock (except pursuant to redemption provisions of Articles): (vii) any transaction in which control of the Company is transferred; (viii) any amendment to the Bylaws or Articles of Incorporation; (ix) any dividend or distribution on capital stock of the Company; and (x) any sale, pledge, license or transfer of all or substantially all of the Company's assets. Standard representations and warranties from the Company, Each officer, employee and consultant of the Company will have entered into a proprietary information and inventions agreement in a form acceptable to the Investors. The Investors shall have a pro rata right, based on their percentage equity ownership of Preferred Stock, to participate in subsequent equity financings of the Company. If any shareholder of Common stock (or equivalents) wants to sell shares, he must offer them first to the holders of Series A Preferred. If a shareholder of Common or equivalent wants to transfer shares, holders of Series A Preferred have a right to participate on a pro rata basis (based on their percentage ownership of the Series A Preferred ) in the sale. This does not apply to sales in a Qualified IPO or afterward. Representations and Warranties: Nondisclosure and Development Agreements: Right of First Refusal: Co-Sale Rights: Information Rights: Board of Directors: Compensation Committee: So long as any Investor of the Series A Preferred holds 250,000 or more shares, the Company will deliver to each Investor annual, quarterly and monthly financial statements; annual business plan and budget, within 45 days prior to the beginning of the fiscal year; and other information reasonably requested by an Investor. Each Investor shall also be entitled to standard inspection and visitation rights. Five total. The Series A Preferred will be entitled to elect two representatives (Alpha will have the right to nominate one representative of Series A Preferred); the Common Stock will be entitled to elect one representative (Wendy Borg as Founders' representative and CEO); and the Common Stock and Series A Preferred, voting together on an as-converted basis, will be entitled to elect two representatives one outsider recommended by the Founders and acceptable to Investors; and one additional outside director acceptable to the board. In the case the escrowed shares are released, the Investors will have the option of replacing the fifth director (i.e. the outside director acceptable to the board) with a new director chosen jointly by the investors. Will set a reasonable board meeting schedule at the first board meeting. Three total. Two representatives of the Series A Preferred and one outside director. All senior management compensation will be approved by the Compensation Committee. Directors and officers will be entitled to indemnification to the fullest extent permitted by applicable law. Investor counsel to draft closing documents. The Company to pay all Investor legal and administrative costs of the financing, not to exceed $20,000 plus disbursements. (a) Beginning on earlier of three years from closing, or six months after Qualified IPO, two demand registrations upon initiation by holders of at least 30% of outstanding Series A Preferred for aggregate proceeds in excess of $7,500,000. Expenses paid by Company. (b) Unlimited piggyback registration rights subject to pro rata cutback permitted at the underwriter's discretion. Full cutback upon a Qualified IPO; 30% minimum inclusion thereafter. Expenses paid by Company (c) Unlimited S-3 Registrations of at least $750,000 each, with no more than two per year. Expenses paid by Company No future registration rights may be granted without consent of a majority of Investors unless subordinate to Investors' rights. Company to obtain key person life insurance policy on Wendy Borg and Jason Kushdog, in the amount of $2 million each, with Company as beneficiary. Indemnification: Counsel and Expenses: Registration rights: Key Person Insurance: Founders Stock, Options and Vesting: Except as approved by Board, employee option pool to that are outstanding or are reserved for issuance immediately after the closing of the merger and (b) have the power to elect at least two-thirds of the surviving corporation's directors) or the sale of 50% or more of the Company's assets or the acquisition in a single transaction or series of related transactions by any person or group of 50% or more of the Company's outstanding Common will be deemed to be a liquidation or winding up for purposes of the liquidation preference unless the holders of at least 70% of the then outstanding shares of Series A Preferred, voting together as a single class, elect not to treat any such event as a liquidation, dissolution or winding up. (3) Redemption: The Series A Preferred shall be redeemed at (1) a redemption price that shall equal the sum of (a) the Series A Purchase Price and (b) any declared but unpaid dividends on such shares of Series A Preferred (including the Accruing Dividends) and (l) there shall be no redemption of Series A Preferred upon an acquisition of the Company or upon a Qualified Public Offering (as hereinafter defined). If the Series A Preferred are not redeemed as required then the Investors shall have the right to designate a majority of the directors. (4) Antidilution Provisions: The Series A Preferred shall have weighted average antidilution rights on issuances of shares at a price less than 100% and greater than 50% of the Series A Purchase Price (except for the issuance of the Reserved Shares): provided if new shares are issued at a price less than or equal to 50% of the Series A Purchase Price then the adjustment will be full ratchet; provided, however, that with respect to a Designated Financing, this ratchet adjustment shall be made only if the holder of Series A Preferred invests its Pro Rata Share. A Designated Financing shall be an equity financing of at least $100,000 made on a pro rata basis (based on ownership of Common) to all Investors that is designated by the Board as a Designated Financing. Each holder's Pro Rata Share equals a portion of the Designated Financing equal to the number of shares of Common owned by such holder divided by the number of shares of Common owned by all Investors. (5) Voting Rights: The Series A Preferred will vote together with the holders of Common on an as-if converted basis on all matters presented to the stockholders. In addition to any other required vote, the Series A Preferred will be entitled to vote as a separate series as described under "Protective Provisions" below. (6) Protective Provisions: Consent of the holders of a super- majority of the Series A Preferred will be required for certain corporate actions, which actions and consent thresholds shall be agreed upon by the parties and shall be more specifically set forth in the closing documents. (7) Conversion: Each share of Series A Preferred may be converted by its holder at any time into a number of shares of Common equal to the Series A Purchase Price divided by the conversion price of the Series A Preferred. The conversion price will initially be equal to the Series A Purchase Price and will be subject to adjustment as Information Rights: Registration Rights: specified in paragraph 4 above. (8) Automatic Conversion: The Series A Preferred will be automatically converted into Common, at the then applicable conversion price, in the event of an underwritten public offering of shares of the Common at a public offering price per share that is no less than $20.00 (to be appropriately adjusted for any stock splits or stock dividends) in an offering with aggregate proceeds to the Company of not less than $25,000,000 (a "Qualified Public Offering"). So long as any of the Series A Preferred is outstanding, the Company will deliver to each Investor annual, quarterly and monthly financial statements, annual budgets and other information reasonably requested by an Investor (a) Beginning on earlier of three years from closing, or six months after Qualified IPO, two demand registrations upon initiation by holders of at least 30% of outstanding Series A Preferred for aggregate proceeds in excess of $7,500,000 Expenses paid by Company. (b) Unlimited piggyback registration rights subject to pro rata cutback permitted at the underwriter's discretion. Full cutback upon a Qualified IPO; 30% minimum inclusion thereafter. Expenses paid by Company. (c) Unlimited S-3 Registrations of at least $750,000 each, with no more than two per year. Expenses paid by Company. No future registration rights may be granted without consent of a majority of Investors unless subordinate to Investors' rights. The proceeds from the sale of the Series A Preferred will be used for working capital. The charter will provide that the authorized number of directors is five. The Board arrangements will include one member elected by the Common Stock (Ms. Borg as founders' representative and CEO). two Series A investor elected representatives, one outsider company nominated and one outsider company- nominated and acceptable to all. Use of Proceeds: Board Representation and Meetings Preemptive Rights: Reserved Shares: The Investors will be given preemptive rights to purchase securities issued by the Company (other than Reserved Shares) based on their percentage equity ownership of Preferred Stock. The integrated preemptive rights will be set forth in the Securities Purchase Agreement discussed below. The Reserved Shares will be issued from time to time to directors, officers, employees and consultants of the Company Upon closing of the Offering, the Company will have reserved for issuance under its stock option plan an aggregate of 2,500,000 shares of Common (the "Reserved Shares), of which 929,889 shares are subject to granted options. The Company shall not increase the number of Reserved Shares under the Incentive Plan or any similar stock option plan without the consent of the holders of a majority of the then outstanding Series A Preferred shares. Unless subsequently agreed to the contrary by the holders of 60% of the shares of outstanding Series A Preferred, any issuance of shares in excess of the Reserved Shares will be a dilutive event requiring the issuance of additional shares of Common as provided above in "Antidilution Provisions and will