Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Really need help filling out the schedules and forms. John and Sandy Ferguson got married eight years ago and have a seven-year-old daughter, Samantha. In

Really need help filling out the schedules and forms.

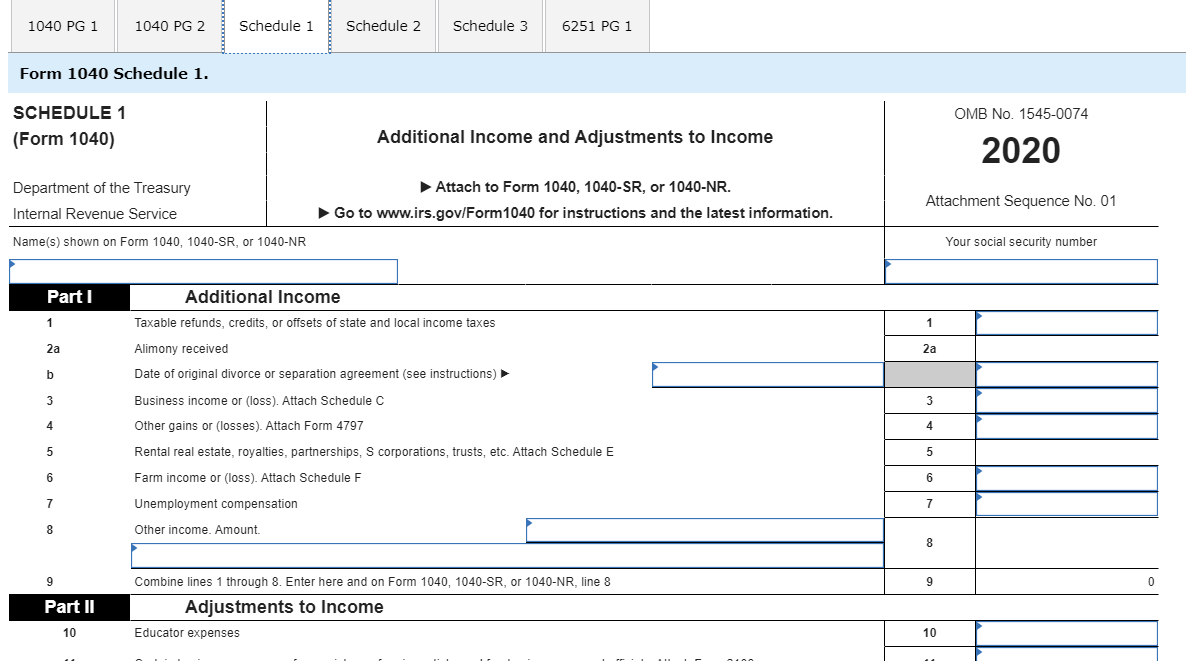

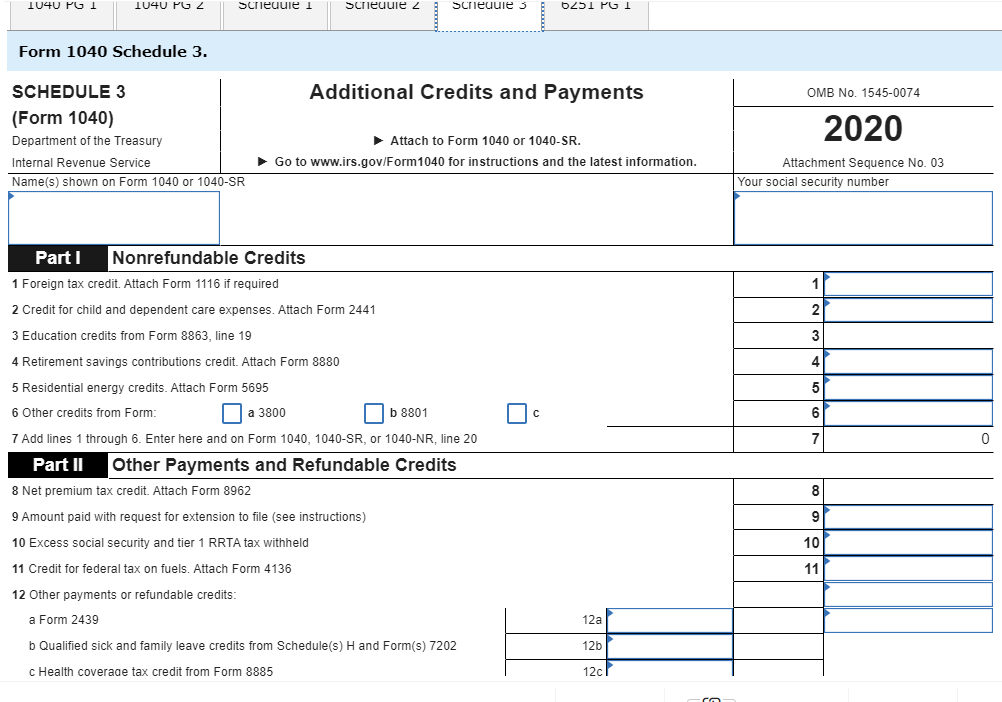

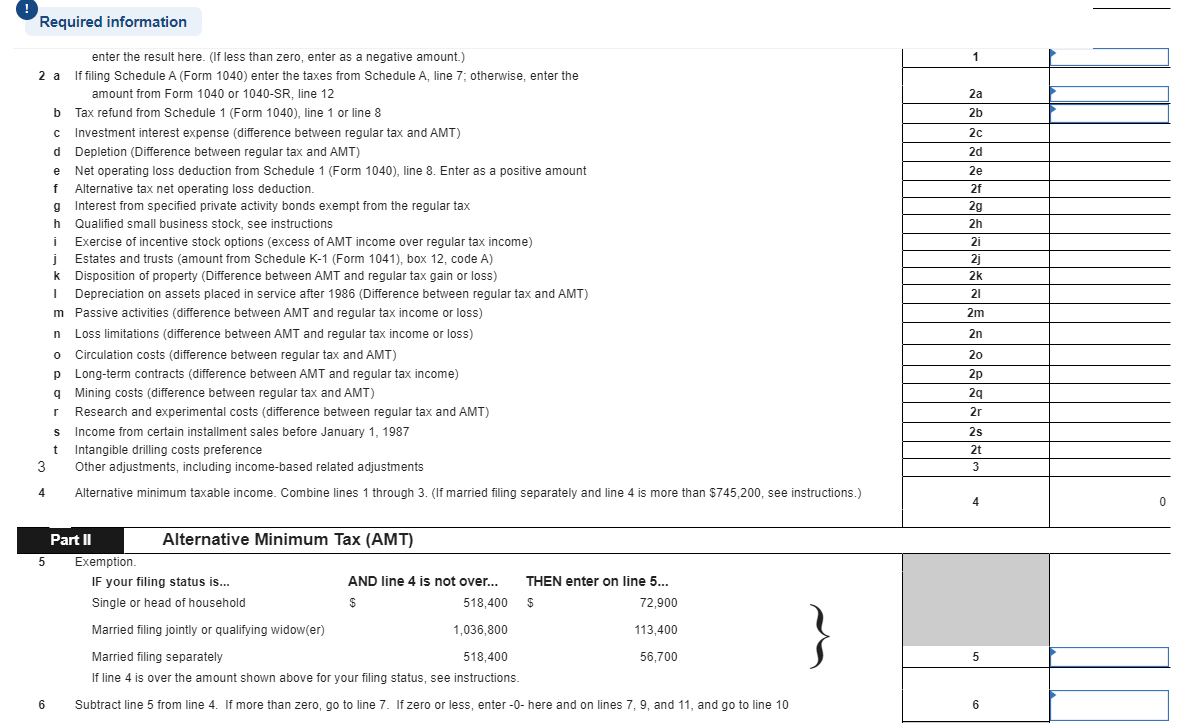

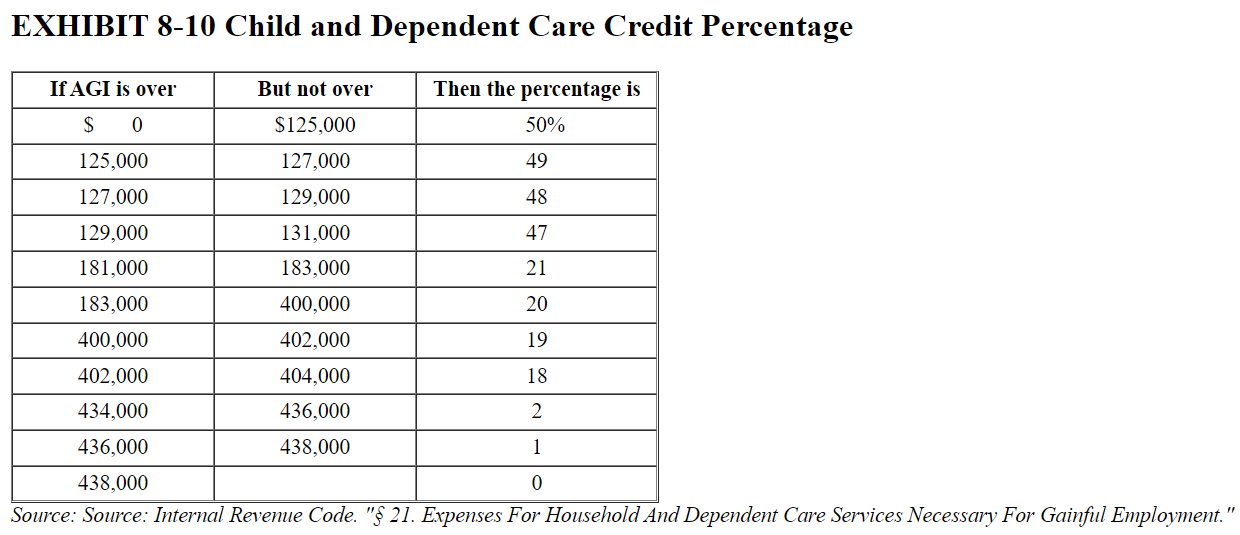

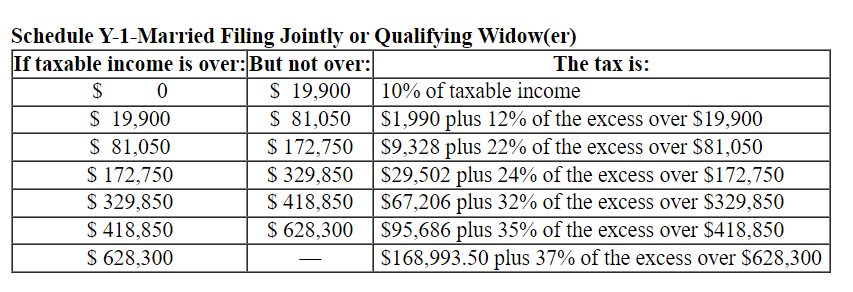

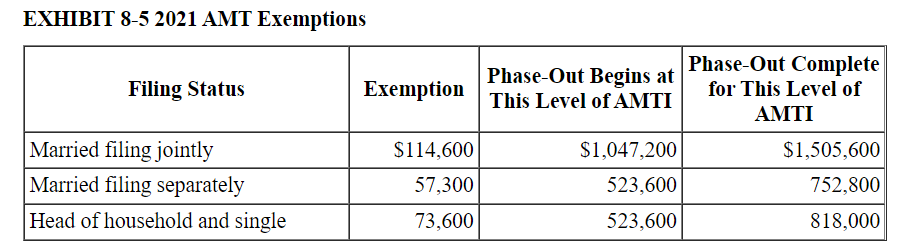

John and Sandy Ferguson got married eight years ago and have a seven-year-old daughter, Samantha. In 2021, John worked as a computer technician at a local university earning a salary of $152,000, and Sandy worked part time as a receptionist for a law firm earning a salary of $29,000. John also does some Web design work on the side and reported revenues of $4,000 and associated expenses of $750. The Fergusons received $800 in qualified dividends and a $200 refund of their state income taxes. The Fergusons always itemize their deductions, and their itemized deductions were well over the standard deduction amount last year. Assume the Fergusons did not receive an advance payment for the 2021 individual recovery credit because they are not eligible for the credit. Use Exhibit 8-10, Tax Rate Schedule, Dividends and Capital Gains Tax Rates, 2021 AMT exemption for reference. The Fergusons reported making the following payments during the year: State income taxes of $4,400. Federal tax withholding of $21,000. Alimony payments to John's former wife of $10,000 (divorced 12/31/2014). Child support payments for John's child with his former wife of $4,100. $12,200 of real property taxes. Sandy was reimbursed $600 for employee business expenses she incurred. She was required to provide documentation for her expenses to her employer. $3,600 to Kid Care day care center for Samantha's care while John and Sandy worked. $14,000 interest on their home mortgage ($400,000 acquisition debt). $3,000 interest on a $40,000 home-equity loan. They used the loan to pay for a family vacation and new car. $15,000 cash charitable contributions to qualified charities. Donation of used furniture to Goodwill. The furniture had a fair market value of $400 and cost $2,000. Complete pages 1 and 2, Schedule 1, Schedule 2, and Schedule 3 of Form 1040 and Form 6251 for John and Sandy. John and Sandy Ferguson's address is 19010 N.W. 135th Street, Miami, FL 33054. Social security numbers: John (DOB 11/07/1970): 111-11-1111 Sandy (DOB 6/24/1972): 222-22-2222 Samantha (DOB 9/30/2016): 333-33-3333 Alimony recipient: 555-55-5555 (Input all the values as positive numbers. Round your intermediate calculations and final answers to the nearest whole dollar. Use 2021 tax rules regardless of year on tax form.) 1040 for a couple Married Filing Jointly with one dependent. 1040 PG 1 1040 PG 2 Schedule 1 Schedule 2 Schedule 3 6251 PG 1 Form 1040 Page 1 and 2. Form 1040 Department of the TreasuryInternal Revenue Service (99) U.S. Individual Income Tax Return 2020 OMB No. 1545-0074 IRS Use Only-Do not write or staple in this space. Single | Married filing jointly Married filing separately (MFS) | Head of household (HOH) Qualifying widow(er) (QW) If you checked the MFS box, enter the name of your spouse. If you checked the HOH or QW box, enter the child's name if the qualifying person is a child but not your dependent. Filing Status Check only one box. Your first name and middle initial Last name Your social security number If joint return, spouse's first name and middle initial Spouse's social security number Last name Home address (number and street). If you have a P.O. box, see instructions. Apt. no. Presidential Election Campaign City, town, or post office. If you have foreign address, also complete spaces below. State ZIP code Check here if you, or your spouse if filing jointly, want $3 to go to this fund. Checking a box below will not change your tax or refund. Foreign country name Foreign province/state/county Foreign postal code You Spouse Yes No At any time during 2020, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency? TE 1040 for a couple Married Filing Jointly with one dependent. 1040 PG 1 1040 PG 2 Schedule 1 Schedule 2 Schedule 3 6251 PG 1 Form 1040 Page 1 and 2. Form 1040 (2020) Page 2 16 Tax (see instructions). Amount. 1 8814 4972 16 17 17 Amount from Schedule 2, line 3 18 Add lines 16 and 17 19 Child tax credit or credit for other dependents 18 0 19 20 Amount from Schedule 3, line 7 20 21 Add lines 19 and 20 21 0 22 23 24 0 22 Subtract line 21 from line 18. If zero or less, enter-0- 23 Other taxes, including self-employment tax, from Schedule 2, line 10 24 Add lines 22 and 23. This is your total tax 25 Federal income tax withheld from: : a Form(s) W-2 b Form(s) 1099 b c Other forms (see instructions) d Add lines 25a through 250 25a 25b 25c 25d 0 If you have a qualifying 26 2020 estimated tax payments and amount applied from 2019 return . 26 child, attach Sch. EIC 27 Earned income credit (EIC) 27 28 Additional child tax credit. Attach Schedule 8812 28 If you have . nontaxable combat pay 29 American opportunity credit from Form 8863. line 8 29 1040 PG 1 1040 PG 2 Schedule 1 Schedule 2 Schedule 3 6251 PG 1 Form 1040 Schedule 2. Additional Taxes OMB No. 1545-0074 SCHEDULE 2 (Form 1040) Department of the Treasury Internal Revenue Service Name(s) shown on Form 1040, 1040-SR, or 1040-NR 2020 Attach to Form 1040, 1040-SR, or 1040-NR. Go to www.irs.gov/Form 1040 for instructions and the latest information. Attachment Sequence No. 02 Your social security number Parti Tax 1 Alternative minimum tax. Attach Form 6251 1 2 Excess advance premium tax credit repayment. Attach Form 8962 2 3 Add lines 1 and 2. Enter here and on Form 1040, 1040-SR, or 1040-NR, line 17 3 Part II Other Taxes 4 Self-employment tax. Attach Schedule SE 4 5 Unreported social security and Medicare tax from Form: a 4137 b 8919 5 6 Additional tax on IRAs, other qualified retirement plans, and other tax-favored accounts. Attach Form 5329 if required 6 7a Household employment taxes. Attach Schedule H 7a b Repayment of first-time homebuyer credit from Form 5405. Attach Form 5405 if required 7b 8 Taxes from: a Form 8959 b Form 8960 c Instructions; enter code(s) 9 Section 965 net tax liability installment from Form 965-A 91 10 Add lines 4 through 8. These are your total other taxes. Enter here and on Form 1040 or 1040-SR, line 23, or Form 1040-NR, line 23b 10 0 For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 71478U Schedule 2 (Form 1040) 2020 THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS 8 1040 PG 1 1040 PG 2 Schedule 1 Schedule 2 Schedule 3 6251 PG 1 Form 1040 Schedule 1. OMB No. 1545-0074 SCHEDULE 1 (Form 1040) Additional Income and Adjustments to Income 2020 Department of the Treasury Internal Revenue Service Name(s) shown on Form 1040, 1040-SR, or 1040-NR Attach to Form 1040, 1040-SR, or 1040-NR. Go to www.irs.gov/Form 1040 for instructions and the latest information. Attachment Sequence No. 01 Your social security number Parti Additional Income 1 Taxable refunds, credits, or offsets of state and local income taxes 1 2a Alimony received 2a b 3 3 4 4 Date of original divorce or separation agreement (see instructions) Business income or (loss). Attach Schedule C Other gains or losses). Attach Form 4797 Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E Farm income or loss). Attach Schedule F Unemployment compensation 5 5 6 6 7 7 8 Other income. Amount. 8 9 9 0 Part II Combine lines 1 through 8. Enter here and on Form 1040, 1040-SR, or 1040-NR, line 8 Adjustments to Income Educator expenses 10 10 1040 PG 1 1040 PG 2 Scrieuule 1 Scrieuule 2 Screuuie 3 6251 PGI Form 1040 Schedule 3. Additional Credits and Payments OMB No. 1545-0074 SCHEDULE 3 (Form 1040) Department of the Treasury Internal Revenue Service Name(s) shown on Form 1040 or 1040-SR 2020 Attach to Form 1040 or 1040-SR. Go to www.irs.gov/Form 1040 for instructions and the latest information. Attachment Sequence No. 03 Your social security number 1 2 3 4 Parti Nonrefundable Credits 1 Foreign tax credit. Attach Form 1116 if required 2 Credit for child and dependent care expenses. Attach Form 2441 3 Education credits from Form 8863, line 19 4 Retirement savings contributions credit. Attach Form 8880 5 Residential energy credits. Attach Form 5695 6 Other credits from Form: a 3800 b 8801 7 Add lines 1 through 6. Enter here and on Form 1040, 1040-SR, or 1040-NR, line 20 Part II Other Payments and Refundable Credits 8 Net premium tax credit. Attach Form 8962 9 Amount paid with request for extension to file (see instructions) 5 O 6 7 0 8 9 10 Excess social security and tier 1 RRTA tax withheld 10 11 Credit for federal tax on fuels. Attach Form 4136 11 12 Other payments or refundable credits: a Form 2439 b Qualified sick and family leave credits from Schedule(s) H and Form(s) 7202 12a 12b c Health coverage tax credit from Form 8885 12c Required information 1 2a 2b 2c 2d enter the result here. (If less than zero, enter as a negative amount.) 2 a If filing Schedule A (Form 1040) enter the taxes from Schedule A, line 7; otherwise, enter the amount from Form 1040 or 1040-SR, line 12 b Tax refund from Schedule 1 (Form 1040), line 1 or line 8 Investment interest expense (difference between regular tax and AMT) d Depletion (Difference between regular tax and AMT) Net operating loss deduction from Schedule 1 (Form 1040), line 8. Enter as a positive amount f Alternative tax net operating loss deduction. g Interest from specified private activity bonds exempt from the regular tax h Qualified small business stock, see instructions i Exercise of incentive stock options (excess of AMT income over regular tax income) -), , Estates and trusts (amount from Schedule K-1 (Form 1041), box 12, code A) k Disposition of property (Difference between AMT and regular tax gain or loss) 1 Depreciation on assets placed in service after 1986 (Difference between regular tax and AMT) m Passive activities (difference between AMT and regular tax income or loss) n Loss limitations (difference between AMT and regular tax income or loss) Circulation costs (difference between regular tax and AMT) Long-term contracts (difference between AMT and regular tax income) q Mining costs (difference between regular tax and AMT) r Research and experimental costs (difference between regular tax and AMT) S S Income from certain installment sales before January 1, 1987 t Intangible drilling costs preference 3 Other adjustments, including income-based related adjustments 4 Alternative minimum taxable income. Combine lines 1 through 3. (If married filing separately and line 4 is more than $745,200, see instructions.) 2e 2f 2g 2h 2i 2j 2k 21 2m 2n 0 20 2p 29 2r 2s 2t 3 0 Part II Alternative Minimum Tax (AMT) 5 Exemption IF your filing status is... AND line 4 is not over... Single or head of household $ 518,400 THEN enter on line 5... $ 72.900 Married filing jointly or qualifying widow(er) 1,036,800 113,400 56,700 5 Married filing separately 518,400 If line 4 is over the amount shown above for your filing status, see instructions. 6 Subtract line 5 from line 4. If more than zero, go to line 7. If zero or less, enter-O- here and on lines 7, 9, and 11, and go to line 10 6 EXHIBIT 8-10 Child and Dependent Care Credit Percentage If AGI is over But not over Then the percentage is 50% $ 0 $125,000 125,000 127,000 49 127,000 48 129,000 131,000 129,000 47 183,000 21 181,000 183,000 400,000 400,000 20 402,000 19 402,000 18 404,000 436,000 434,000 2 436,000 438,000 1 0 438,000 Source: Source: Internal Revenue Code. "$ 21. Expenses For Household And Dependent Care Services Necessary For Gainful Employment. !! Schedule Y-1-Married Filing Jointly or Qualifying Widow(er) If taxable income is over:But not over: The tax is: $ 0 $ 19,900 10% of taxable income $ 19,900 $ 81,050 $1,990 plus 12% of the excess over $19,900 $ 81,050 $ 172,750 $9,328 plus 22% of the excess over $81,050 S 172,750 $ 329,850 $29,502 plus 24% of the excess over $172,750 S 329,850 $ 418,850 $67,206 plus 32% of the excess over $329,850 $ 418,850 $ 628,300 $95,686 plus 35% of the excess over $418,850 $ 628,300 $168.993.50 plus 37% of the excess over $628,300 Tax Rates for Net Capital Gains and Qualified Dividends Head of Household Trusts and Estates Rate* 0% Married Filing Jointly $0-$80,800 $80,801 - $501,600 $501,601+ Married Filing Separately $0 - $40,400 $40,401 - $250.800 $250,801+ Taxable Income Single $0-$40,400 $40,401 - $445,850 $445,851+ 15% $0 - $54,100 $54,101 - $473,750 $473,751+ $0-$2,700 $2,701 - $13,250 $13,251+ 20% *This rate applies to the net capital gains and qualified dividends that fall within the range of taxable income specified in the table (net capital gains and qualified dividends are included in taxable income EXHIBIT 8-5 2021 AMT Exemptions Filing Status Exemption Phase-Out Begins at This Level of AMTI Phase-Out Complete for This Level of AMTI Married filing jointly Married filing separately Head of household and single $114,600 57,300 73,600 $1,047,200 523,600 523,600 $1,505,600 752,800 818,000 John and Sandy Ferguson got married eight years ago and have a seven-year-old daughter, Samantha. In 2021, John worked as a computer technician at a local university earning a salary of $152,000, and Sandy worked part time as a receptionist for a law firm earning a salary of $29,000. John also does some Web design work on the side and reported revenues of $4,000 and associated expenses of $750. The Fergusons received $800 in qualified dividends and a $200 refund of their state income taxes. The Fergusons always itemize their deductions, and their itemized deductions were well over the standard deduction amount last year. Assume the Fergusons did not receive an advance payment for the 2021 individual recovery credit because they are not eligible for the credit. Use Exhibit 8-10, Tax Rate Schedule, Dividends and Capital Gains Tax Rates, 2021 AMT exemption for reference. The Fergusons reported making the following payments during the year: State income taxes of $4,400. Federal tax withholding of $21,000. Alimony payments to John's former wife of $10,000 (divorced 12/31/2014). Child support payments for John's child with his former wife of $4,100. $12,200 of real property taxes. Sandy was reimbursed $600 for employee business expenses she incurred. She was required to provide documentation for her expenses to her employer. $3,600 to Kid Care day care center for Samantha's care while John and Sandy worked. $14,000 interest on their home mortgage ($400,000 acquisition debt). $3,000 interest on a $40,000 home-equity loan. They used the loan to pay for a family vacation and new car. $15,000 cash charitable contributions to qualified charities. Donation of used furniture to Goodwill. The furniture had a fair market value of $400 and cost $2,000. Complete pages 1 and 2, Schedule 1, Schedule 2, and Schedule 3 of Form 1040 and Form 6251 for John and Sandy. John and Sandy Ferguson's address is 19010 N.W. 135th Street, Miami, FL 33054. Social security numbers: John (DOB 11/07/1970): 111-11-1111 Sandy (DOB 6/24/1972): 222-22-2222 Samantha (DOB 9/30/2016): 333-33-3333 Alimony recipient: 555-55-5555 (Input all the values as positive numbers. Round your intermediate calculations and final answers to the nearest whole dollar. Use 2021 tax rules regardless of year on tax form.) 1040 for a couple Married Filing Jointly with one dependent. 1040 PG 1 1040 PG 2 Schedule 1 Schedule 2 Schedule 3 6251 PG 1 Form 1040 Page 1 and 2. Form 1040 Department of the TreasuryInternal Revenue Service (99) U.S. Individual Income Tax Return 2020 OMB No. 1545-0074 IRS Use Only-Do not write or staple in this space. Single | Married filing jointly Married filing separately (MFS) | Head of household (HOH) Qualifying widow(er) (QW) If you checked the MFS box, enter the name of your spouse. If you checked the HOH or QW box, enter the child's name if the qualifying person is a child but not your dependent. Filing Status Check only one box. Your first name and middle initial Last name Your social security number If joint return, spouse's first name and middle initial Spouse's social security number Last name Home address (number and street). If you have a P.O. box, see instructions. Apt. no. Presidential Election Campaign City, town, or post office. If you have foreign address, also complete spaces below. State ZIP code Check here if you, or your spouse if filing jointly, want $3 to go to this fund. Checking a box below will not change your tax or refund. Foreign country name Foreign province/state/county Foreign postal code You Spouse Yes No At any time during 2020, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency? TE 1040 for a couple Married Filing Jointly with one dependent. 1040 PG 1 1040 PG 2 Schedule 1 Schedule 2 Schedule 3 6251 PG 1 Form 1040 Page 1 and 2. Form 1040 (2020) Page 2 16 Tax (see instructions). Amount. 1 8814 4972 16 17 17 Amount from Schedule 2, line 3 18 Add lines 16 and 17 19 Child tax credit or credit for other dependents 18 0 19 20 Amount from Schedule 3, line 7 20 21 Add lines 19 and 20 21 0 22 23 24 0 22 Subtract line 21 from line 18. If zero or less, enter-0- 23 Other taxes, including self-employment tax, from Schedule 2, line 10 24 Add lines 22 and 23. This is your total tax 25 Federal income tax withheld from: : a Form(s) W-2 b Form(s) 1099 b c Other forms (see instructions) d Add lines 25a through 250 25a 25b 25c 25d 0 If you have a qualifying 26 2020 estimated tax payments and amount applied from 2019 return . 26 child, attach Sch. EIC 27 Earned income credit (EIC) 27 28 Additional child tax credit. Attach Schedule 8812 28 If you have . nontaxable combat pay 29 American opportunity credit from Form 8863. line 8 29 1040 PG 1 1040 PG 2 Schedule 1 Schedule 2 Schedule 3 6251 PG 1 Form 1040 Schedule 2. Additional Taxes OMB No. 1545-0074 SCHEDULE 2 (Form 1040) Department of the Treasury Internal Revenue Service Name(s) shown on Form 1040, 1040-SR, or 1040-NR 2020 Attach to Form 1040, 1040-SR, or 1040-NR. Go to www.irs.gov/Form 1040 for instructions and the latest information. Attachment Sequence No. 02 Your social security number Parti Tax 1 Alternative minimum tax. Attach Form 6251 1 2 Excess advance premium tax credit repayment. Attach Form 8962 2 3 Add lines 1 and 2. Enter here and on Form 1040, 1040-SR, or 1040-NR, line 17 3 Part II Other Taxes 4 Self-employment tax. Attach Schedule SE 4 5 Unreported social security and Medicare tax from Form: a 4137 b 8919 5 6 Additional tax on IRAs, other qualified retirement plans, and other tax-favored accounts. Attach Form 5329 if required 6 7a Household employment taxes. Attach Schedule H 7a b Repayment of first-time homebuyer credit from Form 5405. Attach Form 5405 if required 7b 8 Taxes from: a Form 8959 b Form 8960 c Instructions; enter code(s) 9 Section 965 net tax liability installment from Form 965-A 91 10 Add lines 4 through 8. These are your total other taxes. Enter here and on Form 1040 or 1040-SR, line 23, or Form 1040-NR, line 23b 10 0 For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 71478U Schedule 2 (Form 1040) 2020 THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS 8 1040 PG 1 1040 PG 2 Schedule 1 Schedule 2 Schedule 3 6251 PG 1 Form 1040 Schedule 1. OMB No. 1545-0074 SCHEDULE 1 (Form 1040) Additional Income and Adjustments to Income 2020 Department of the Treasury Internal Revenue Service Name(s) shown on Form 1040, 1040-SR, or 1040-NR Attach to Form 1040, 1040-SR, or 1040-NR. Go to www.irs.gov/Form 1040 for instructions and the latest information. Attachment Sequence No. 01 Your social security number Parti Additional Income 1 Taxable refunds, credits, or offsets of state and local income taxes 1 2a Alimony received 2a b 3 3 4 4 Date of original divorce or separation agreement (see instructions) Business income or (loss). Attach Schedule C Other gains or losses). Attach Form 4797 Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E Farm income or loss). Attach Schedule F Unemployment compensation 5 5 6 6 7 7 8 Other income. Amount. 8 9 9 0 Part II Combine lines 1 through 8. Enter here and on Form 1040, 1040-SR, or 1040-NR, line 8 Adjustments to Income Educator expenses 10 10 1040 PG 1 1040 PG 2 Scrieuule 1 Scrieuule 2 Screuuie 3 6251 PGI Form 1040 Schedule 3. Additional Credits and Payments OMB No. 1545-0074 SCHEDULE 3 (Form 1040) Department of the Treasury Internal Revenue Service Name(s) shown on Form 1040 or 1040-SR 2020 Attach to Form 1040 or 1040-SR. Go to www.irs.gov/Form 1040 for instructions and the latest information. Attachment Sequence No. 03 Your social security number 1 2 3 4 Parti Nonrefundable Credits 1 Foreign tax credit. Attach Form 1116 if required 2 Credit for child and dependent care expenses. Attach Form 2441 3 Education credits from Form 8863, line 19 4 Retirement savings contributions credit. Attach Form 8880 5 Residential energy credits. Attach Form 5695 6 Other credits from Form: a 3800 b 8801 7 Add lines 1 through 6. Enter here and on Form 1040, 1040-SR, or 1040-NR, line 20 Part II Other Payments and Refundable Credits 8 Net premium tax credit. Attach Form 8962 9 Amount paid with request for extension to file (see instructions) 5 O 6 7 0 8 9 10 Excess social security and tier 1 RRTA tax withheld 10 11 Credit for federal tax on fuels. Attach Form 4136 11 12 Other payments or refundable credits: a Form 2439 b Qualified sick and family leave credits from Schedule(s) H and Form(s) 7202 12a 12b c Health coverage tax credit from Form 8885 12c Required information 1 2a 2b 2c 2d enter the result here. (If less than zero, enter as a negative amount.) 2 a If filing Schedule A (Form 1040) enter the taxes from Schedule A, line 7; otherwise, enter the amount from Form 1040 or 1040-SR, line 12 b Tax refund from Schedule 1 (Form 1040), line 1 or line 8 Investment interest expense (difference between regular tax and AMT) d Depletion (Difference between regular tax and AMT) Net operating loss deduction from Schedule 1 (Form 1040), line 8. Enter as a positive amount f Alternative tax net operating loss deduction. g Interest from specified private activity bonds exempt from the regular tax h Qualified small business stock, see instructions i Exercise of incentive stock options (excess of AMT income over regular tax income) -), , Estates and trusts (amount from Schedule K-1 (Form 1041), box 12, code A) k Disposition of property (Difference between AMT and regular tax gain or loss) 1 Depreciation on assets placed in service after 1986 (Difference between regular tax and AMT) m Passive activities (difference between AMT and regular tax income or loss) n Loss limitations (difference between AMT and regular tax income or loss) Circulation costs (difference between regular tax and AMT) Long-term contracts (difference between AMT and regular tax income) q Mining costs (difference between regular tax and AMT) r Research and experimental costs (difference between regular tax and AMT) S S Income from certain installment sales before January 1, 1987 t Intangible drilling costs preference 3 Other adjustments, including income-based related adjustments 4 Alternative minimum taxable income. Combine lines 1 through 3. (If married filing separately and line 4 is more than $745,200, see instructions.) 2e 2f 2g 2h 2i 2j 2k 21 2m 2n 0 20 2p 29 2r 2s 2t 3 0 Part II Alternative Minimum Tax (AMT) 5 Exemption IF your filing status is... AND line 4 is not over... Single or head of household $ 518,400 THEN enter on line 5... $ 72.900 Married filing jointly or qualifying widow(er) 1,036,800 113,400 56,700 5 Married filing separately 518,400 If line 4 is over the amount shown above for your filing status, see instructions. 6 Subtract line 5 from line 4. If more than zero, go to line 7. If zero or less, enter-O- here and on lines 7, 9, and 11, and go to line 10 6 EXHIBIT 8-10 Child and Dependent Care Credit Percentage If AGI is over But not over Then the percentage is 50% $ 0 $125,000 125,000 127,000 49 127,000 48 129,000 131,000 129,000 47 183,000 21 181,000 183,000 400,000 400,000 20 402,000 19 402,000 18 404,000 436,000 434,000 2 436,000 438,000 1 0 438,000 Source: Source: Internal Revenue Code. "$ 21. Expenses For Household And Dependent Care Services Necessary For Gainful Employment. !! Schedule Y-1-Married Filing Jointly or Qualifying Widow(er) If taxable income is over:But not over: The tax is: $ 0 $ 19,900 10% of taxable income $ 19,900 $ 81,050 $1,990 plus 12% of the excess over $19,900 $ 81,050 $ 172,750 $9,328 plus 22% of the excess over $81,050 S 172,750 $ 329,850 $29,502 plus 24% of the excess over $172,750 S 329,850 $ 418,850 $67,206 plus 32% of the excess over $329,850 $ 418,850 $ 628,300 $95,686 plus 35% of the excess over $418,850 $ 628,300 $168.993.50 plus 37% of the excess over $628,300 Tax Rates for Net Capital Gains and Qualified Dividends Head of Household Trusts and Estates Rate* 0% Married Filing Jointly $0-$80,800 $80,801 - $501,600 $501,601+ Married Filing Separately $0 - $40,400 $40,401 - $250.800 $250,801+ Taxable Income Single $0-$40,400 $40,401 - $445,850 $445,851+ 15% $0 - $54,100 $54,101 - $473,750 $473,751+ $0-$2,700 $2,701 - $13,250 $13,251+ 20% *This rate applies to the net capital gains and qualified dividends that fall within the range of taxable income specified in the table (net capital gains and qualified dividends are included in taxable income EXHIBIT 8-5 2021 AMT Exemptions Filing Status Exemption Phase-Out Begins at This Level of AMTI Phase-Out Complete for This Level of AMTI Married filing jointly Married filing separately Head of household and single $114,600 57,300 73,600 $1,047,200 523,600 523,600 $1,505,600 752,800 818,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Theory

Authors: Ahmed Raihi-Belkaoui

5th Edition

1844800296, 978-1844800292