Answered step by step

Verified Expert Solution

Question

1 Approved Answer

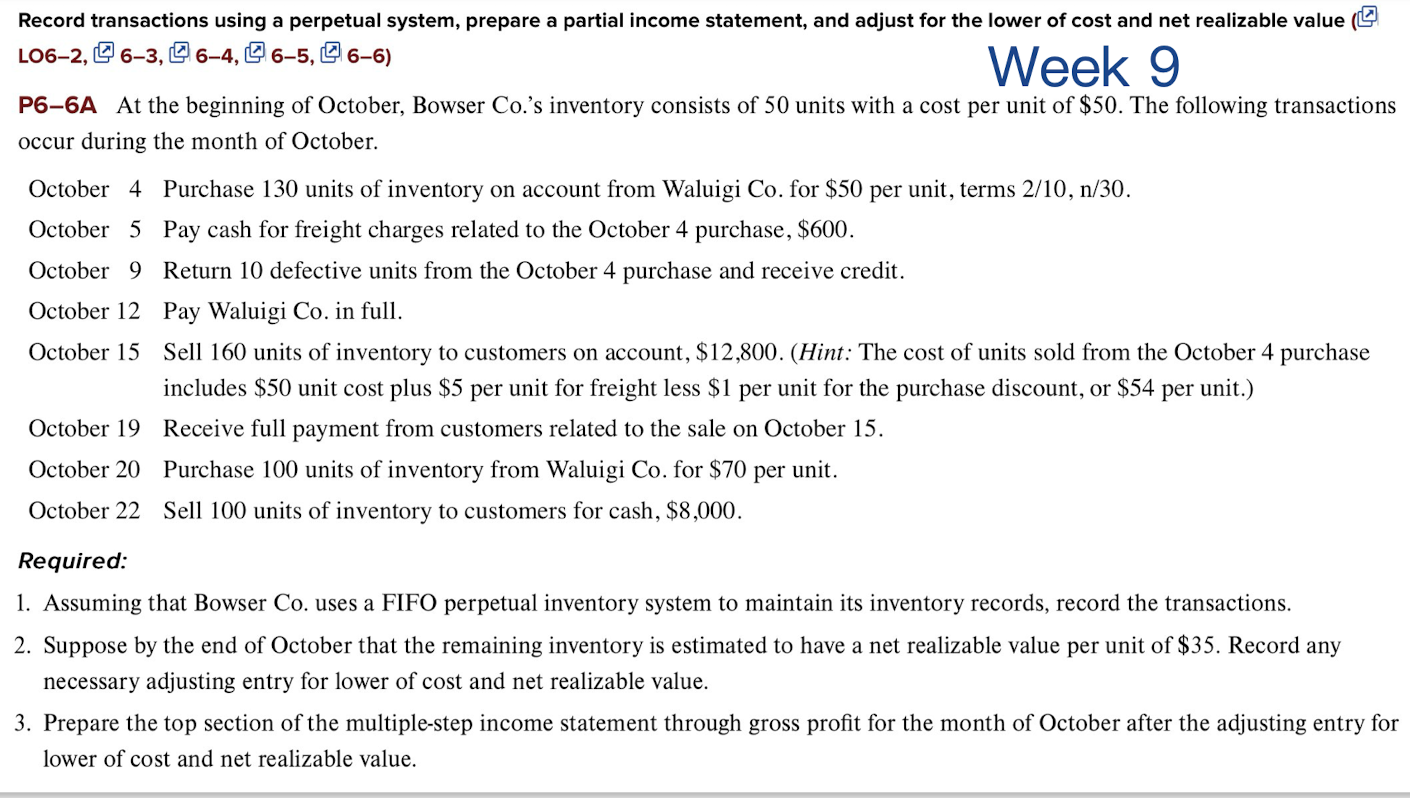

Record transactions using a perpetual system, prepare a partial income statement, and adjust for the lower of cost and net realizable value ( P 6

Record transactions using a perpetual system, prepare a partial income statement, and adjust for the lower of cost and net realizable value

PA At the beginning of October, Bowser Cos inventory consists of units with a cost per unit of $ The following transactions

occur during the month of October.

October Purchase units of inventory on account from Waluigi Co for $ per unit, terms

October Pay cash for freight charges related to the October purchase, $

October Return defective units from the October purchase and receive credit.

October Pay Waluigi Co in full.

October Sell units of inventory to customers on account, $Hint: The cost of units sold from the October purchase

includes $ unit cost plus $ per unit for freight less $ per unit for the purchase discount, or $ per unit.

October Receive full payment from customers related to the sale on October

October Purchase units of inventory from Waluigi Co for $ per unit.

October Sell units of inventory to customers for cash, $

Required:

Assuming that Bowser Co uses a FIFO perpetual inventory system to maintain its inventory records, record the transactions.

Suppose by the end of October that the remaining inventory is estimated to have a net realizable value per unit of $ Record any

necessary adjusting entry for lower of cost and net realizable value.

Prepare the top section of the multiplestep income statement through gross profit for the month of October after the adjusting entry for

lower of cost and net realizable value.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Cost Accounting

Authors: T.R.Sikka

7th Edition

8130918706, 978-8130918709